Notes From AR 2019 Va tech wabag

AR 2019

Our strengths not only lie in being capable and competitive, but our order wins during the year, is a testimony to our collaborative and co-operative mind-set across clusters and cultures.

Water scarcity is the one issue that is plaguing not

just homes, but offices, hotels and even schools. The groundwater reserve in several of the districts are getting depleted, triggering anxiety. As many as 22 districts, including Chennai, where the water is getting depleted at an alarming rate have been put in the red category. The water shortage has started affecting the hotels in the city. Several of the small and medium hotels were planning to down

the shutters and some of the companies have requested their employees to work from home until the water situation improved.

Water scarcity is being driven by two converging phenomenon: fast growing freshwater use and even faster depletion of usable freshwater resources.

Rising awareness

Future-ready

Closing thoughts

The Company’s business is gradually scaling upwards. Going forward, focusing on emerging markets besides implementing key projects, achieving group synergies, increasing business profitability and effective and economically viable application of technologies would

form the key strategic areas of our business. Our aim is to provide solutions that help extend the life span and usage

of water.

Projects under Namami Gange is our first attempt under the scheme HAM. It reflects our commitment to clean our nation’s longest and sacred river Ganga.

Our Company has always believed and held on to the philosophy of remaining asset light. With liquidity being the key challenge, the Government has chosen the HAM (Hybrid-Annuity Model) route to invite financing through public private partnership framework. Projects under Namami Gange is our first attempt under HAM. It also reflects our commitment to clean our nation’s longest and sacred river Ganga.

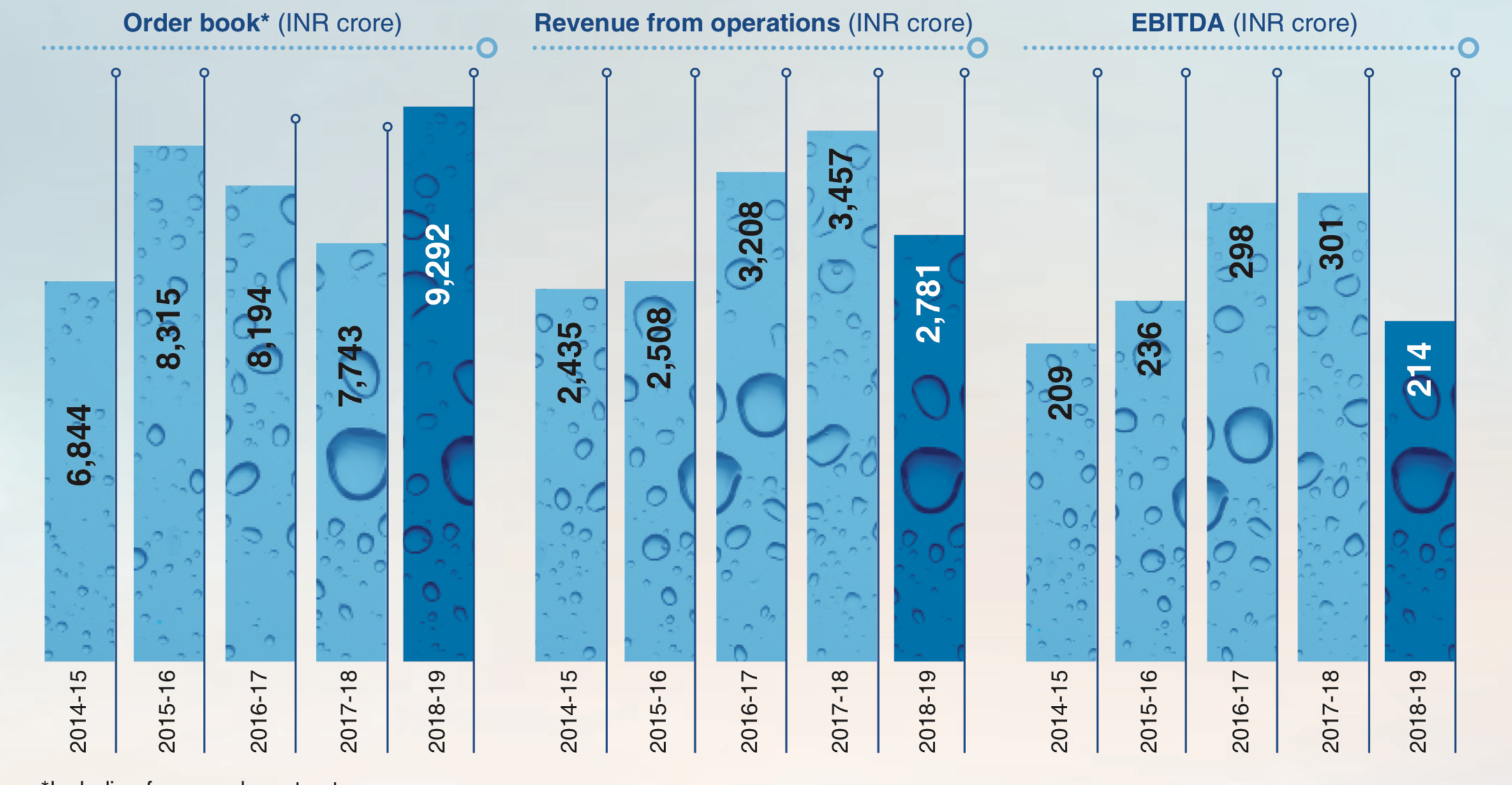

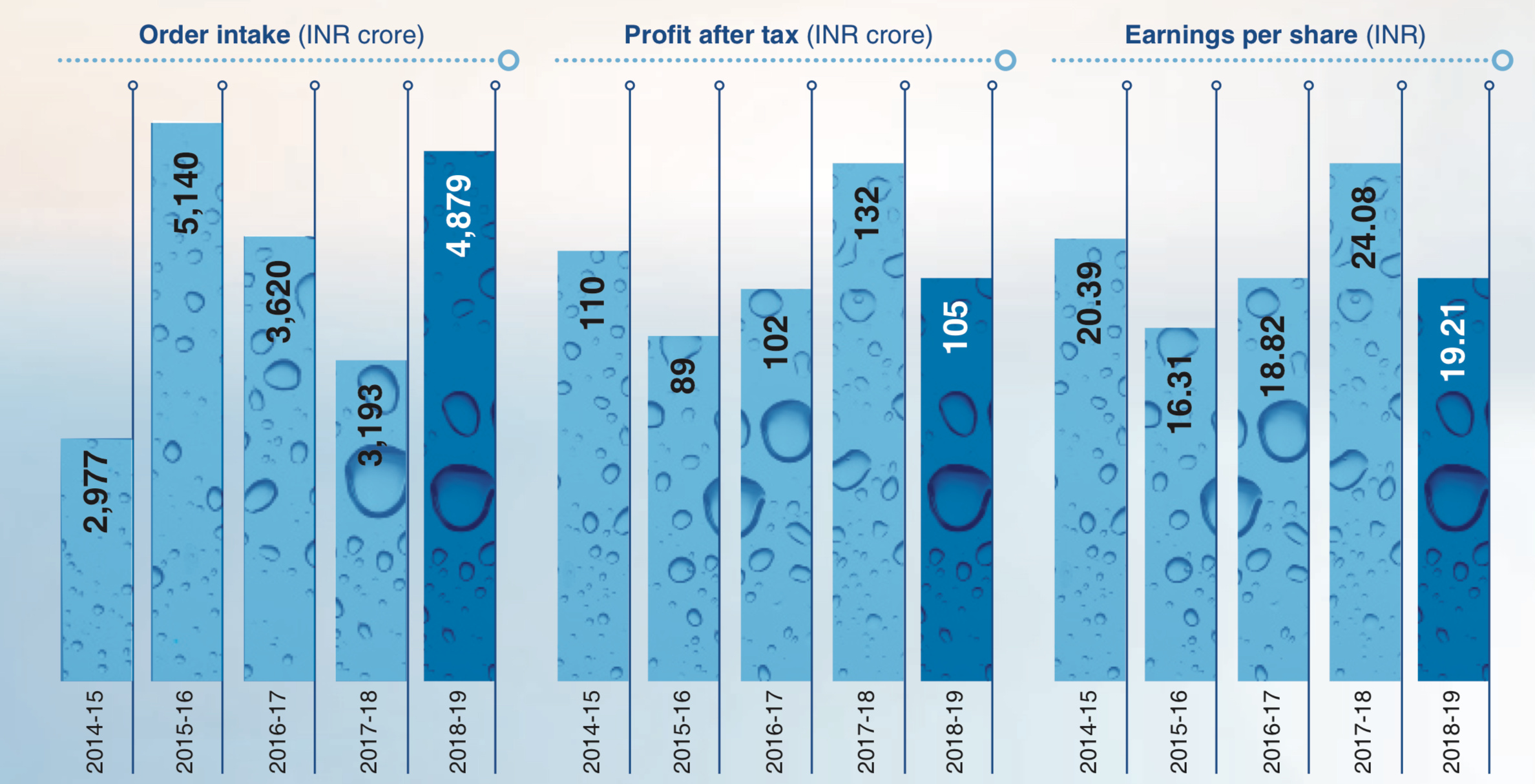

Our order book as on March 31, 2019 stands over 9200 crore, out of which significant Order Intake achieved during FY 19, supported by our MEA region… This reiterates

our strategy to diversify geographically and reduce the dependence on India.

Talent acquisition and transformation

An organisation only succeeds when it is able to nurture

its core asset – people. In our endeavour to develop a consolidated and cluster based growth we embarked on hiring talent. This has helped us in strengthening all clusters with right management bandwidth and functional capabilities to work as an independent unit.

In order to leverage the opportunities worldwide, WABAG has chosen a cluster based approach. With this approach it is not only making its presence felt but also creating synergies among cross cultures and a sense of ownership across ONE WABAG.

Screen Shot 2019-07-22 at 11.13.48 AM

Screen Shot 2019-07-22 at 11.13.56 AM

Focus Areas for 2019

Patents

Building process efficiency Information systems

Product innovation and technology

LIFE CYCLE PARTNERSHIP

EPC

DBO – Design-Build-Operate

BOOT – Build-Own-Operate-Transfer

O&M

Remaining Asset-Light

Performance Highlights

FY 2018-19 was a mixed bag in terms of achievements. On one side, our financial performance was impacted due to revenue de-growth driven by completion of

2 major overseas projects during the year and the subsequent delay in finalisation of new orders. These new major overseas orders were expected to be awarded 3 quarters earlier and subsequently started contributing to the revenue during FY 2018-19.

The economic benefit of access to clean drinking water and basic sanitation would amount to more than USD 43 billion a year or an economic gain each year of around 5.2% of GDP with a benefit cost ratio of 3.2 and a payback period of 7 years. In less than a decade, there could be a transformative boost to the Indian economy just by helping its citizens access clean drinking water and sanitation. The Water Ministry in India has also brought some initiative to bring all departments working on water under one roof. Providing access to clean drinking water and sanitation is around six times bigger than the ambition of bringing electricity to every part of India. To fulfil the electricity dream, power had to be taken to a little more than 20 million households, whereas nearly 141 million households lack piped water. But as challenging as it sounds, it is a fundamental pillar to India’s USD 5 trillion dream.

The revenue and profit is lower as compared to previous year on account of our large key overseas projects like AMAS and RAPID have reached completion during the current fiscal year and major new orders secured during the year are in early stage of execution. Revenue from new orders is expected to pick up momentum in FY 2019-20.

Management Discussion

Global water use has increased six-fold over the past 100 years and has been increasing steadily by about 1% every year. Changing consumption patterns, burgeoning population, climatic changes and socio-economic developments have led

Global water Demand by 2040 withdrawal

5000

to a surge in demand for clean and safe water. The global water cycle is intensifying due to climatic changes, the wet regions getting wetter and dry ones becoming drier. The phenomenon impacted over 4 billion lives (nearly 2/3rd of the world population) who experience severe water scarcity for a month every year and 2 billion people facing high water stress.

Surprisingly, 1% increase in water consumption every year is expected to trigger a 20-30% surge in demand by 2050. It would be driven by both industrial and domestic sectors. The crisis would be persistent and escalate further with time. Besides, water pollution in key rivers of Asia, Africa and Latin America has worsened since 1990. The coming decades would see a plummet in water quality only to become a threat to the ecosystem.

On Going initiatives and Goals Ahead

Driving SUSTAINABILITY Delivering VALUE

| Policy |

initiatives |

| Vietnam Government’s Initiatives |

Attract investments to provide 85% of the urban population with access to clean urban water and to treat 45% of the urban wastewater by 2020 |

(Source: Vietnam water summit)

Investment of USD 1.7 billion for construction of new regional water supply system to serve the Mekong Delta|

|National Mission for Clean Ganga and high budget allocation, India|28 River-Front Development projects, 33 Entry level projects for construction, modernisation and renovation of 182 Ghats and 118 Crematoria have been initiated

63 sewerage management projects are under implementation in the states of Uttarakhand, Uttar Pradesh, Bihar, Jharkhand and West Bengal; 12 new sewerage management projects launched in these States and works are in process to create a sewerage capacity of 1,187.33 MLD

The Ministry is implementing key projects such as Namami Gange, Pradhan Mantri Krishi Sinchayee Yojana and river inter linking. It also plans to complete 80% of the Ganga cleaning programme by 2019.|

|National Drinking Water Policy|The National Drinking Water Policy provides a framework for addressing the key issues and challenges facing the countries water supply sector in the provision of safe water supply to the people of Sri Lanka. Increasing demands from a growing population, competing uses of water in an expanding economy, mounting evidence of environmental degradation, rising costs of development of new supplies, increased pollution from urbanisation and lack of policies and institutional constraints, are critical issues in meeting targets in the water supply sector.|

|Water Privatisation in Indonesia|The central government of Indonesia has repeatedly announced its intention to universalise access to clean water by 2019. To achieve this, an estimated 27 million new connections are needed, with a major investment gap of USD 20.8 billion.|

india

Key Drivers

Safe and Adequate Drinking water in rural Areas:

Government aims to provide 100% drinking water. Currently, 71.8% of India has access to safe drinking water. Gujarat, Goa, Madhya Pradesh are close to achieving universal coverage, while UP follows with 98% coverage.

installed Sewage Treatment Capacity: The installed sewage treatment capacity of urban India as a percent of sewage generated is 37.6%. The target is to reach 68.8%by 2030. Gujarat, Himachal Pradesh, Punjab and Sikkim, and the UT of Chandigarh have already achieved it.

Annual Ground water withdrawal: Around 62% of the net available groundwater in India is withdrawn. With the upper limit at 70% to control the replenishment rate at normal levels. Haryana, Punjab, Rajasthan and Delhi need to improve this ratio which has far surpassed the maximum limit.

Sewage Treatment Market in india

Increasing municipal and industrial activities triggered a surge in sewage production in the urban parts of the country.

On Going initiatives and Goals Ahead

sewage capacity has increased from 11,787 MLD in 2009 to 26,066 MLD in 2018 (as of July 2018). Currently, around 83% is operational. A number of policy changes have been promulgated by municipal agencies at central and state level to encourage stakeholders to recycle and reuse water.

The Government has launched various policies in the last couple of years, like ‘100 Smart Cities,’ the ‘Atal Mission for Rejuvenation and Urban Transformation of 500 Habitations,’ the ‘Namami Gange Mission’ and the ‘Swachh Bharat Mission.’

Various projects, under different phases in the pipeline, are expected to create 11,550 MLD of additional sewage treatment capacity and expand the network by 18,280km. The investment required for this sector over 2019-2026 is likely to be around INR 167 billion.

| Policy |

initiatives |

| Ministry of Power Notification on Reuse |

The policy mandates thermal power plants located within a 50 km radius of municipal sewage treatment plants to use treated sewage for its process applications. |

| Ministry of Housing and Urban Affairs Faecal Sludge and Septage Management Policy |

The Ministry has come up with a comprehensive manual mandating sewage treatment plants to compost digested sludge which is rich in organic nutrients and promote sale as fertilisers. The Ministry will provide an incentive of INR 1500 per ton of fertiliser sold. |

| Ministry of Science and Technology, DST |

The ministry has come up with the National Mission on Desalination to be of use to utilities across India. The mission has kick started with a compendium of global technologies from proven players highlighting the techno commercial details and benefits. Given the prospects of desalination in Gujarat, Tamil Nadu and Karnataka, this mission will act as a guiding tool to develop new technologies and create more cost optimal and sustainable desalination solutions. |

| National Mission for Clean Ganga’(NMCG) |

Aims at providing comprehensive and sustainable solutions for major pollution hot-spots across 97 towns and 4,465 villages on the Ganga stem. As per the available data, a total of 150 sewage projects have been taken up, of these, 112 are on the main course of Ganga and rest on tributaries. 42 projects have been completed, 61 are in progress and 47 are under tendering process. |

In Kanpur, 20 MLD Common Effluent Plant (CETP) has been sanctioned with an estimated cost of INR 617 crore. This project has an integrated approach of including conveyance system from individual units, large chrome recovery plants and a pilot zero liquid discharge plant.

In Uttarakhand, sewage and ghat works have been sanctioned with investments of INR 1,337 crore to be utilised over next 15 years for O&M.|

Middle East & north Africa (MEnA)

Once the birthplace of ancient civilisations, the Middle East and North Africa region is at crossroads at present. This arid region has always faced unavailability of water. Limited resources, degrading infrastructure compounded by rapid population growth has led to the dwindling of the resource. The water resources per capita are 1/6th of the global average.

| Policy |

initiatives |

| National Water Resources Plan |

Implementation of the National Water Plan 2017 - 2037 in the drinking water space with an investment of USD 50 billion over next 20 years. |

The Government envisions the reuse of effluent from sewage treatment plants and water efficiency.

Egypt has announced urgent plan for water security. The Government plans to build new water purification plants and expand the network of the desalination plants with the aim to provide potable water to all across the country.|

|Vision 2030, Kingdom of Saudi Arabia|Aims to achieve 100% treated water by 2025. Currently, the market size is USD 4.7 billion

Under the Vision 2030 mission, the National Water Strategy 2030 is created under which the kingdom has stepped up its efforts to rationalise local water consumption, sustain

and maintain water security, and provide high quality water supplies to consumers. The Government aims at adopting cost efficient desalination and distribution mechanisms. Plans to build nine water desalination plants on the Red Sea coast, at a total cost of more than SAR 2 billion and with total production capacity of 240,000 cubic meters of water per day.

The Government has set up an organisation called National Water Company (NWC) which plans USD 23 billion investments in water treatment and reuse related capital expenditure over the next 20 years.

(Source: Gulf State Analytics)|

|UAE Water Security Strategy 2036|Aims to ensure sustainable access to water during both normal and emergency conditions in line with local regulations, standards of the World Health Organisation, and the UAE’s vision to achieve prosperity and sustainability. The overall objectives of the strategy are to reduce total demand for water resources by 21 percent, increase the water productivity index to USD 110 per cubic meter, reduce the water scarcity index by three degrees, increase the reuse of treated water to 95 percent and increase national water storage capacity up to two days.|

|The Recycled Water Policy UAE|The Recycled Water Policy underscores DoE’s recognition of water as a strategic resource and its understanding that water security is an integral part of the sustainable water security. There is an urgent need to develop an integrated policy to manage all water resources in the emirate, including recycled water. The Recycled Water Policy is aligned with the objectives of UAE Water Security Strategy 2036 to ensure sustainable and continued access to water at all times and under any circumstances and to secure an adequate water supply for residential, commercial, governmental, industrial, and agricultural uses.|

latin America

Historically, Latin America is known to have always given high priority to water conservation and health. Despite the region’s income and urbanisation levels, only 60% of the population has access to the sewerage system and 40% of the wastewater gets treated.

On Going initiatives and Goals

| Policy |

initiatives |

| Initiatives by Development Bank of Latin America |

The Development Bank of Latin America (CAF) estimated that over the period 2010-2030, USD 80 billion should be spent on sewerage infrastructure and USD 33 billion on wastewater treatment. |

| (Source: World Bank) |

|

| Abu Dhabi Fund for Development (ADFD) |

Abu Dhabi Fund for Development (ADFD), the leading national entity for international development aid, has approved USD 80 million for the water sector in Argentina. |

r&D programmes at wABAG

1) Ceramopur®

The trials were conducted for treating groundwater with the Ceramic Membrane Filtration process and was concluded in February 2018. The forthcoming Pilot Plant is to be utilised for our Ceramozone® trials where it is foreseen to treat tertiary treated sewage to produce potable water in the final step.

2) Ceramozone®

Ceramozone® trials utilises pre-ozonation / Advanced Oxidation process (AOP), ceramic membrane filtration (with our Ceramopur® technology as discussed above) and granular activated carbon filtration to treat tertiary treated sewage with an aim to get potable water as the last step after chlorine disinfection.

3) research studies with the institute of Chemical Technology (iCT)

4) Damopur

Damopur is WABAG’s technology for Deammonification process (Ammonia removal) in the mainstream

5) Membrane Distillation (MD)

The MD Pilot Plant was identified for further treatment and recovery of water from RO Brine with the Vacuum Membrane Desalination (VMD) technology. The trials will be continued in Nemmeli SWRO for further recovery of water from SWRO Brine.

6) Hard COD

The aim of the Hard COD Pilot Plant is to remove ‘unbiodegradable particulate COD’ which doesn’t get effectively removed in the effluent with the conventional treatment process for ETPs.

7) nereda – Granular activated Sludge

8) ipsach Biel – Multiple Barrier System for lake water Treatment

9) Altenrhein - Micropollutants removal

10) Klosters - Arsenenic removal

11) windhoek - Antimicrobial resistance in water reclamation and reuse

12) frauenkirchen - Micropollutants removal by ozone and activated carbon (KomOzAk)

13) frankfurt – Micro-sieving Pilot Tests at the nidda STP

Disclosure( Holding> 5% of my portfolio in equities)