It is. Take it with a pinch of salt. See the efficiency of their Chennai plant. Cash is reality. Any pile up in receivables or orders getting delayed would hit the bottom-line further.

Disc: No holdings

1 Like

hi @saravananb1994 - Can you let me know if it would be idle to do a cumulative of PAT with FCF or do it with cCFO, i do not have much idea on this, can you throw some light here.

@Hocuspocus32 - Hi Vivek can you let me know how did you get the capex and other values (I mean how was that calculated)

The purpose is to see where the funds come from. Higher operating cash flows are good.

These are available from screener.in

@Gaurav_Agarwal @saravananb1994 Hi essentially this is a projects company and in addition a lot of the business is from government bodies, while margin may be higher but payments will be spread out over years. Even profits would be calculated on percentage of completion basis so essentially there is a lot of volatility on cash flow and to a lesser extent in profits. WC cycles will be long and ROCE will be low.

Just as a comparison have pasted same data for L&T consol numbers from screener. They exhibit the same pattern. One cannot judge this as one would a manufacturing company.

Disclosure - Invested

3 Likes

All I am saying is this need looking deep into the company. Just because L&T numbers are like this does not justify Va Tech Wabag numbers.

People who are invested or are interested in investing need to find a just answer as to why for long periods of time Cash from operating activity is diverging from Net Profit.

2 Likes

Proceed with your own risk. I love cash flow generating businesses.

@saravananb1994 @Gaurav_Agarwal - Even I love cash generating companies

But if cash flow from operations is the only criteria we should never look beyond IT/ FMCG cos, no industry will come close to them. Limited point I am making is every industry has different characteristics, in project companies, as size of company (and consequently balance sheet) grows more working capital is utilized hence cash flow from operation is poor. When balance sheet degrows it will actually improve.

Looking at a single ratio in isolation, without taking into account nature of the industry may lead us to wrong conclusions. That’s all from my side…

5 Likes

Groundwater level has seen a depletion of 61% between 2007-2017. As we all know, water cannot be artificially produced hence the only option is to use it reuse and recycle existing resources. VA Tech Wabag is a pioneer in this field.

I would like to add a few points to the above thesis:

-

The management is solid. It uses smart techniques in order to reduce cost.

-

It has a heavy order book which assures revenue growth.

-

The company has undergone an organisational structure change which will help in better efficiency.

-

The only risk to the company is that it outsources the construction of these treatment plants to contractors which runs the potential risk of a delay in executions. But, again I don’t see this as a significant problem as there are no substitutes for the products of this company.

-

Equity Intelligence has a holding in this company.

6 Likes

Holding with a similar thesis. Will wait to see how it plays out.

Management interview link

They are quite bullish on Namami Gange projects and WC reduction (primarily due to APGenco retention money refunds)

2 Likes

Everything that he said in the video is largely on expected lines although I would want to know what he means by ‘hybrid’ projects. Do let me know!

See this link on Hybrid annuity projects.

3 Likes

In recent times promoters are selling its share, do anyone knows the prudence of promoters behind it?

Where do you see this information. I don’t see it on bse insider trading link.

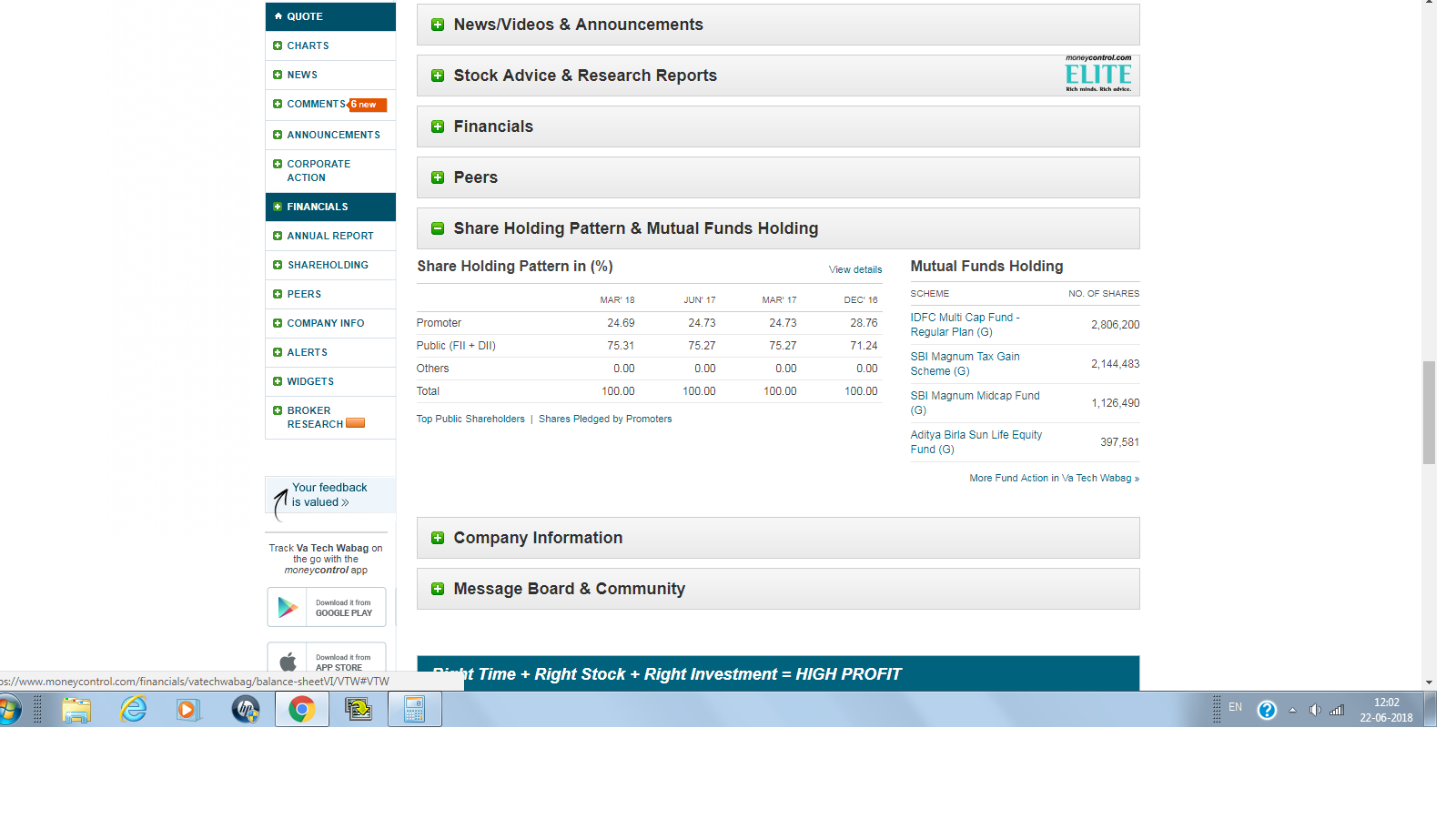

The reduction of 4.02 % in Dec 2016 to Mar 2017 from 28.76 to 24.73 is just because 4.02 % holding of promoter Amit Sengupta is not showing part of promoter group. He has not sold it out. I don’t know why he is moved out of promoter group.

Also when i checked BSE website reduction from 24.73 to 24.69 doesn’t make much sense as number of shares is all same. Some accounting round off it seems.

Amit Sengupta has reduce his stake . Now showing in Public Shareholder.

Latest annual report https://www.bseindia.com/bseplus/AnnualReport/533269/5332690318.pdf