VGUARD management has no history of governance issues so we should not worry. The entire hotel sector will also recover in H2 2021. Vguard has FII holdings and management knows what happens if their is an issue with diversion. Anyway VGUARD is not that cash rich given its growth ambitions for them to move money .

Best test is that Vguard is debt free so moving funds is like moving their own money and we need not worry

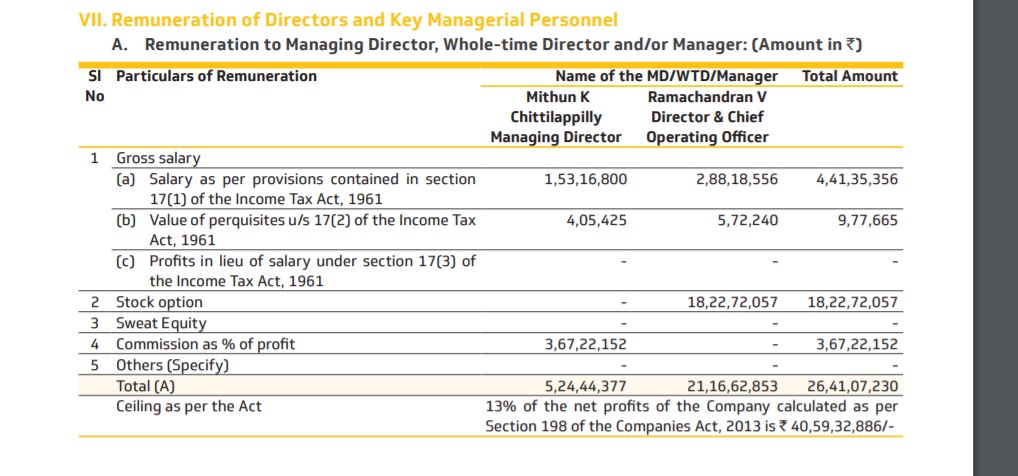

The management salary seems comfortable except for Mr. Ramachandran V. His total salary roughly at 21 crores majority of which is stock option seems exceptionally high for company of this size and it has been the case with this person for last few years.

During his tenure of ~9 years, Sales have nearly doubled or ~8% CAGR. Profits have gone 3.15x, but EPS only tripled due to the dilution; still that is a ~13% CAGR, all the while maintaining RoCE above ~25% on average and healthy Cashflows.

I think we should consider this and cut the company some slack. More so, the overall Remuneration of the Management is ~35% lesser than the Statutory Limit.

The only vice of the company seems to the high Working Capital requirement at around ~15% of Sales on average over the years. Although since Mr. V. Ramachandran joining the company, the Cash Conversion Cycle has come into control a bit (Falling from the 110-120s to the 70-80s).

Also, I was pleasently surprised to note that the company provides a transcript for the AGM as well. More companies should follow this, as the majority of the Shareholders will likely not attend the AGM in person.

Plus, if you generally browse the company’s website, there are all sorts of disclosures and the Annual Report itself is quite good and transparent (Including details of the dilution due to ESOP issue, details of ESOP issue and the valuation).

Thank you @dineshssairam for your views. Whats your take on current valuation as the stock corrected to 180 levels now. Historically vguard used to command higher vsluation, however it didn’t participate in the bull run past 2 years.

I haven’t valued it yet. Just got back to going through the Annual Reports.

The ESOPs started in 2013 and have since scaled a lot. But as I mentioned, this is compensated by improved business metrics on all sides.

Trying to understand why their Margins are lower than Havell’s. Between the two firms, that seems to be the major difference. Even Growth, Returns and Working Capital needs are similar.

Some interesting investments like Gegadyne Energy which I need to go through.

The impression I’ve gotten so far is that the Management does want to move up the Value Chain, but stay within their Competence of Electric / Electronic related “FMEG”, as they call it.

V-Guard follows an asset light hybrid manufacturing model, 50% manufacturing is outsourced. Once a product gains significant scale, they start manufacturing in-house. Havell’s owns the backward integrated value chain, manufactures 95% in-house. However, V-Guard is moving in the same direction, in-house manufacturing increased from 40% to 50% in last 5 years.

Hi Just wanted to check if V Guard is using Blue Yonder ( the old i2) for supply chain management and SalesForce for Customer Relations ? Was going thru the ARs but couldn’t find any references. These two softwares can be a game changer for V Guard I suppose !

One christian priest who was first donor to a stranger roped in the founder to donate to another, thus created a big chain of kidney donations in kerala, i think by now the largest in the world.

Consumer durables grew nicely. Have achieved descent scale. To contribute more to bottomline going fwd

High cost inventory levels going down. As it runs down, EBITDA margins likely to go back to pre Covid levels of 10-11 pc vs 6-7 pc currently

Completed acquisition of Sunflame electricals in Jan. Integration process to start soon. New management to be in place by March or so

Some areas where Sunflame can show immediate improvements - South Mkts where they r under-represented, Online and Organised channels, Direct go to mkt (as they were only going through distributors)

Sunflame business largely flat for 9M FY 23

Sunflame acquisition cost at 640 cr

Sunflame has large incremental (unutilized) capacities, doesn’t requrire capex. V Guard to continue with yearly capex rate of 50-70 cr

Own:Outscourced manufacturing for combined entity to be in the range of 70:30. To inch higher towards own mfg with every passing year

Cash balance + current investments of about 400cr to be used towards funding the a/m acquisition. Plus a debt of about 250 cr to be raised. Sunflame’s revenues to be added to V-Guard’s from Jan onwards

Sunflame’s margins are higher than V Guard standalone