Q3 results:

How does the distribution reach of V guard compare with that of Havells ?

About PAT growth 54%, management has clarified in con call that this is one-time growth effect due to lower base effect in 1Q19 real picture is QoQ growth. Otherwise company is growing as normal. Weak demand persist in market

Consumer eletricals & electronics have good growth, check Havells Q1 results, shown good growth in this segment.

May be because of less penetration and replacement demand, even though tough real state situation.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/f30c98e2-2ecb-4f1b-8bc7-dc0568c85bb8.pdf

Annual Report (2018-2019)

valuation of v-guard is on the higher side , eventhough its run by an ethical promoter & good management. I’m expecting a good correction in this bear market to add to my position

Disclosure: trimmed position couple of months ago (profit booking)

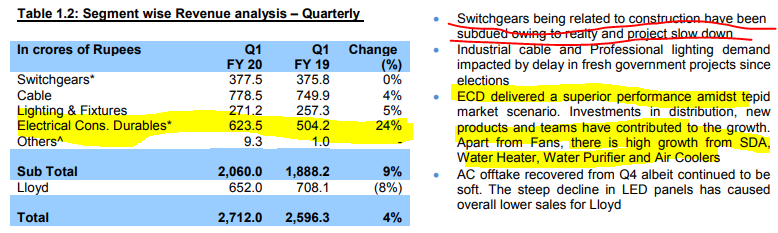

Q2 FY 20 highlights:

• Consolidated Net Revenue from operations for the quarter ended September 30, 2019 was

Rs. 623.27 crores; an increase of 3.1 % over previous year (Rs.604.50 crores).

• Consolidated Profit Before Tax for the quarter ended September 30, 2019 was Rs.78.48

crores; Increase of 62.6% over the previous year (Rs.48.27 crores).

• Consolidated Profit After Tax for the quarter ended September 30, 2019 was Rs.58.75

crores; Increase of 54.4% over the previous year (Rs.38.04 crores).

• During the quarter, Stabilizer and electrical segment registered growth. Overall, subdued

consumer demand impacted top-line growth.

• Non-South markets contributed 37% of turnover for the quarter, up from 35.7% in the

corresponding quarter of the previous year.

• Results for the quarter include a writeback of Rs.10.12 crores of ESOP provisions no

longer required.

impression from the concall

the headlines were

1.weak demand, no comments on improvement possibility

2.11 percent yoy topline growth guidance

3.h2 and q3 will be better

4.in this market environment, focus to maintain margins if required at the cost of revenues

5. consumer durable performance to be better in coming quarters

6.focus on increased distribution through eCommerce, presently 50cr of the topline in this quarter

market overview-

slowdown in demand, increased competition to gain market share by pricing by other players and new entrants, no demand picking up from affordable housing stimulus by the government, unorganised sector continue to have and gain their share of the market, gst had no impact.floods in kerala , bihar and rains in maharashtra impacted this quarter like previous year, dewali season has been as expected nothing exuberant , waterheater forms a major part of cons durable segment and sales have been affected in this quarter due to supply constraints from china, which ha cleared up by now, this segment performance to increase in h2, management approach to navigate this scenario is grow distribution via eCommerce and refresh product line to justify higher price to the customer and inhouse manufacturing to be installed in fans and water heater segment, capex is being done for that regard, distribution channel’s inventory has been building up, receivables can be expected to increase

margins- increased price hike has contributed to 1% of the gross margin, hikes taken in water heater , stabilizer and inverter battery segments, 32% margin sustainable going forward, ad spends to remain same at around 5% of expenses, south vs non south margins have converged, margin lower during ecom sale periods, otherwise margins are equivalent

gross margins look better this year because of 3 factors, 2% dip in margins due to floods last year leading to discounts and incentives given, lower commodity prices and price hike

general info-

fans, stabilizer and inverter battery is the main seller in nonsouth market

5-6 out of 12 product line is sold in non south market

looking out for M&A opportunities

competition in the market since 12-15 months already, continuing on performance till now and to go forwards on similar lines…

expansion into kitchen appliances and water purifier segemnts over next 1 year

most of the analyst seemed to have focused their concerns about the topline growth, demand improvement expectation, better performance of consumer durable going forward , plans to increase distributing channels at a faster pace, margin sustainability and h2 performance improvement…

except, cons. durables segment , h2 performance, management was less optimistic about the concerns …

already trading at high valuation thoughout the volatile broader market , and no visible growth triggers in topline and always persisting threat of revenue growth slow down due to competitive market environment , what the market has more to discount going forward?

a better h2, compared to h1, a debt free balance sheet, free cash flow, focus on maintaining margin with risk to absolute profits ?

will that be enough, i highly doubt it…

I have seen companies in recent times at the face of poor demand their attempt to maintain margin dosent hold up, ends up losing both top and bottom line and also margins in the end along with increase in receivables and expanding working capital cycle…

a change in the general market sentiments might help with higher price to earnings, which is already very high, then again earnings have a threat, in my opinion, we have a poor risk to reward in this scrip…

disclaimer… invested.

Interesting !

Q3’2020 results

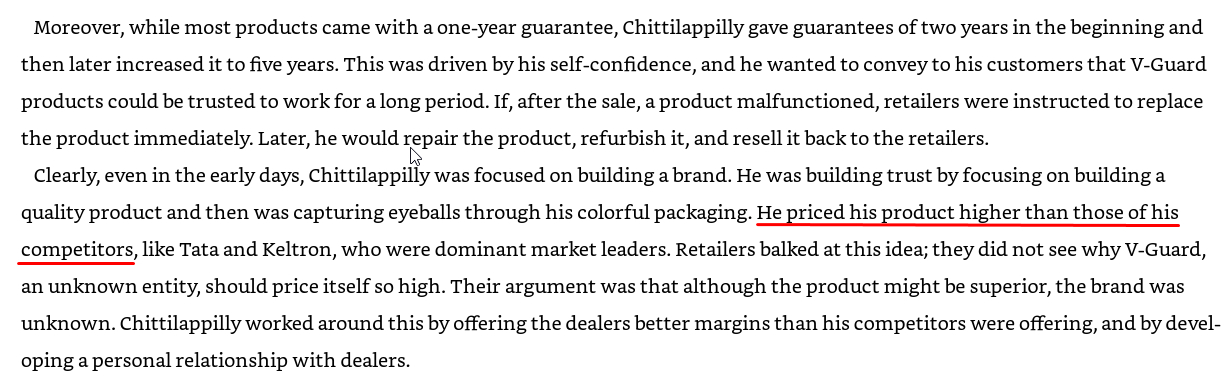

While V-guard has done well in diversifying into other verticals like Fans, geysers, kitchen appliances - a casual search on Flipkart will show you that their prices are pretty high compared to the competiton like Bajaj, Crompton, Orient etc . I do not see any of their products selling in volumes like the other brands for the above segments.

Key moniterable will be the pricing strategy they adopt going forward, as the premium they command in stabilizers & UPS systems wont be so easy to do in other well penetrated segments

They have been always like that.

Source: Rohith Potti, Pooja Bhula _ Intelligent Fanatics of India (2019)

Giving an extended warranty in products like fans , geysers , large kitchen appliances is nothing new and in fact many brands do the same

In any case when was the last time anyone changed their ceiling fan or geyser in less than 5 years. After the initial month, these products just become almost un-noticeable

True, just wanted to point out that keeping their products at a slight premium has always been their strategy. Now whether that is an useful one or not is a different take.

V Guard’s Q1 results.

Disc : invested

Hi All,

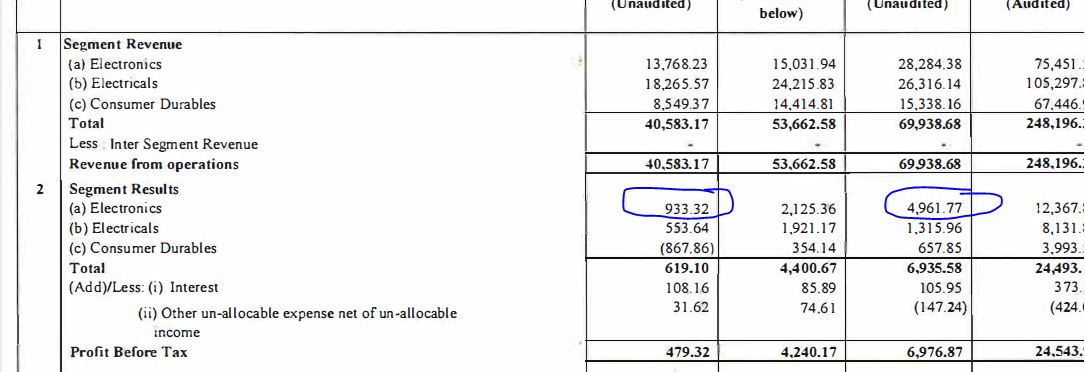

If we check the results and segment wise profits it is quite evident that the consumer durable segment has reported loss,other segments like Electronics and Electricals have reported profit.

But if we have a significant look we can see that profits have somewhat halved in the segments like Consumer durables(657.85 to -(867.86)) and Electricals(1,315.96 decreased to 553.64) but in the Electronics segments(comprising of Stabilizers, Digital UPS, UPS and Solar Inverters) for which they are market leader,their profits have significantly dropped from 4,961.77 to 933.32(decreased by almost 3/4th).Please see the image for more details.

Fellow VPs kindly let us know what you make out of this results.I am pointing this because they are market leaders in the electronics segment and they have performed better in other segments comparing to their core competency interms of the profits.Please note that the comparison is YoY and figures are in lakshs.

Thanks,

Deb