He is younger brother of Satpal Khattar.

1 Like

I thought there would be some linkage since he too is based out of Singapore. Thanks for clarifying.

http://backoffice.phillipcapital.in/Backoffice/Researchfiles/PC_-Uniply_Industries_Initiating-_May_2018_20180504163215.pdf

Following is a brief summary from latest annual report:

Topline grew by almost 100% yoy. 2018 revenue 403 cr vs 230 cr in fy 2017.

As of June 2018, Company has order book or 600+ cr from affordable housing segment.

In long run, company expects to have 75% revenue from affordable housing

By 2022 company expects to clock 2000 cr in topline.

All segment except the subsidiary plywood did well in fy 2018. Plywood expected to do will in 2019 as operational efficiency kicks in.

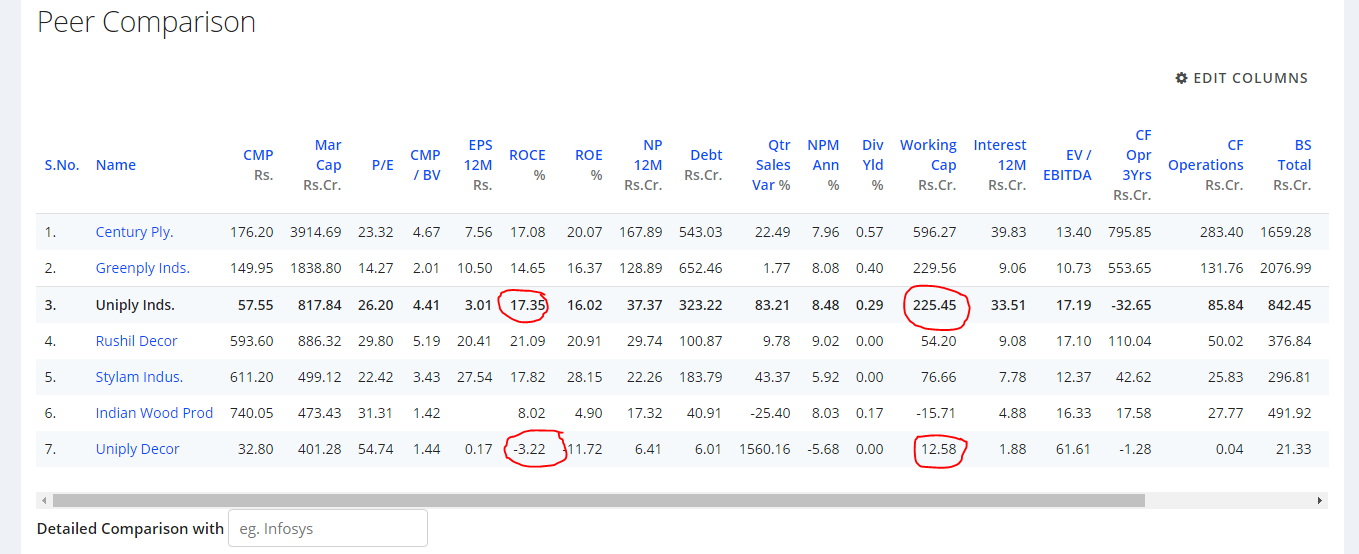

Disc - I am invested heavily and is part of my long term core portfolio. IMHO Company is available at attractive valuations with current Mcap of 930 cr and 2019 topline alone will be in tune of 900 cr. So it’s available at one time sales.

Keshav purchased 0.86% stake from the open market and knowing how prudent he is went on record when the valuations were high, it again confirms the fact that valuations are very very attractive at CMP and it’s a bargain.

Disc- I am adding on every dip and is currently 12% of my sizable portfolio.

Malabar and Promoter entity both purchased additional stake from open market yesterday in Uniply.

1 Like

its available on BSE https://beta.bseindia.com/corporates/ann.html?scrip=532646&dur=A&expandable=3https://beta.bseindia.com/corporates/ann.html?scrip=532646&dur=A&expandable=3

To be clear, the information was shared with exchanges yesterday but the purchase was made almost a month ago.

Malabar India fund buys on 25th and 26th sep.

Can anyone share a link or site which gives an overview of addressable market size for affordable housing?

Affordable housing definition

https://m.economictimes.com/definition/affordable-housing

With Govt of India focus on above as per Housing for All initiative it’s quite huge

Glancing at Annual Report tells me that they are tying with Developers currently on Modular Kitchen space during New Home Construction and it’s contracted first as it’s mentioned as WC-ve and can scale easily with tie ups with more Developers

1 Like

Yeah, precisely the reason I wanted to know the addressable market size. More than developers they would want to tie up with state governments and be approved vendor for respective state body. Gov is their only customer in this space ( so far ) but you are right, this segment is easily scalable and doesn’t require any capex of WC. Margins are high too. So if Company indeed is able to achieve 1200 cr of sales this year and 2500 by 2022, then current valuations are very very attractive.

Page 30 of Current Annual Report gives Housing Shortage and numbers which you wanted

Still understanding the story but low interest coverage ratio, high debt to equity and Govt Order Dependency on major growth and margin area( also caution of payments delay this FY in Page 27 of AR) is cautioning to invest on this story

Also, affordable housing segment being WC -ve is hard to believe as contractors are generally paid daily and employees monthly and they are into milestones based payments in this segment

Repco and BLS investments has burned myself on concentration and Govt dependency coupled with abrupt decision risks

Disc : Not invested

I’m unable to understand: Does the company provide fit-out solutions to real estate players or does Uniply itself construct these affordable houses. If it is the former - why does it depend on government land allocation and if latter, then is it sort of a R.E. play?

Please see enclosed images from the latest AR.

Too much debt on book

This was one of my doubts which has popped up while going through the Annual report.

Even in the research report of Phillip Capital, commentary/analysis on affordable housing is missing. Despite this they have mentioned that the T/o will increase 100% YOY for FY19 & 20.

Only thing which I can think of is Phillip Capital research report is date May-18 and AR is Aug-18 and they are not aware of this.

Other comforting factors with respect to UNIPLY is SN has picked up sizeable stake and is still accumulating on drops.

Disc - Not invested, Under watch list

I need to check the debt nos, but going by the AR, management claims the company is under borrowed and don’t see any significant capex in foreseeable future. Besides so long as the ROCE nos are in high 20’s debt shouldn’t be a concern.

Gov being the major customer is in a sense positive, since the economic cycle doesn’t affect orders and execution as would be the case with pvt RE players.

Reason they call it WC-ve I think is, they source RM from subsidiary Uniply Decor, make the fitouts in house and deploy. Once they get payment in phase manner the parent Uniply would payback the decor company thus being WC -ve

Uniply only does Kitchen outfits for the new construction houses under affordable housing. They are currently serving only in the state of Telangana however looking to tie up with other state gov. Gov allots the lands to RE players for construction and believe Kitchen / door panels etc gets outsourced to Uniply.

Interesting point to note here is, this was not even their bread and butter business ( which continue to remain as the plywood and interior design business) however Keshav saw the opportunity and given this a lost cost ( no capex ) high margin business which not only strengthens the balance sheet at bottom line, but also increase the capacity utilization of subsidiary. The size of this opportunity is so big that in first years itself, 60% of Uniply Decors sale came from parent Uniply Industries.

Disc - started with an initial allocation in 2016 but have increased stake substantially in last 30 days and is currently my top holding with more than 15% of my PF.

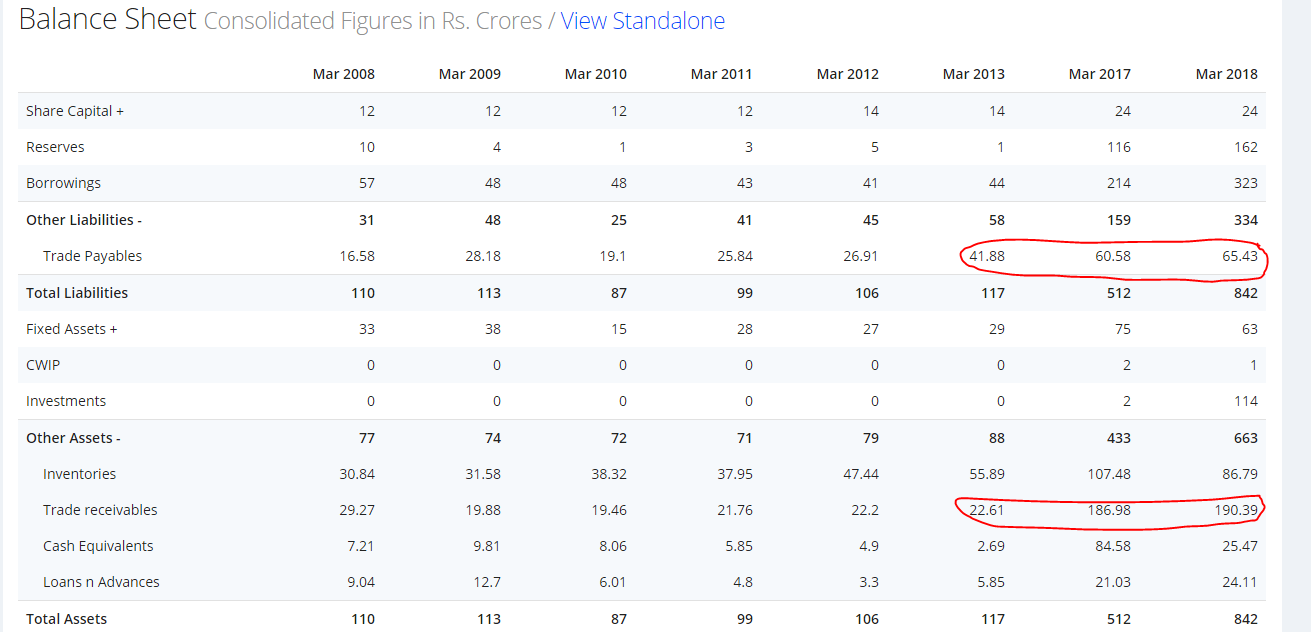

Thanks @rajpanda for starting the thread. One very peculiar thing which i noticed in the annual report was that almost all the money raised through equity and debt went into Advances for Investments (Note 9 - Other Assets).

Can someone help me understand what does that mean and what is this capital being used for ?

The only relevant thing i could come across was this -