Those are 2017-18 nos. FY 19 ROCE projected at 21%. Not entire business is WC -ve but just the affordable housing fitout space. The traditional plywood business requires working capital.

Consider this, at the start of FY 18 in April of 2017, they had zero orders in affordable housing space, the closed the year with order book of 600 odd cr. Currently at high level of closing a deal of two large IT parks in HYD and expects to close year with total revenue of 1200 cr. With 10% margin company will have 120 cr profits and is available at 800 cr market cap today. I have not yet mentioned about the management pedigree and have very high regards for the new promoter. If not already seen, suggest to see three 10 mins videos or promoter on HYBIZ TV on YouTube.

Ok so those the projected nos.

Do they have any investor presentation showing business segments their nos. and margins??How much from government works , private works and how much from plywood ???

If we see and check the nos. of Uniply decor the receivables are very less compare to Uniply industries receivables and also check the payable nos.?? All are in Uniply industries Balance sheet only.

Also do consider the risk of payments/receivables from State Governments. Also the next year State Elections In Telangana, who knows once Government changes the whole business goes for a toss we know how the subcontracting works are awarded.

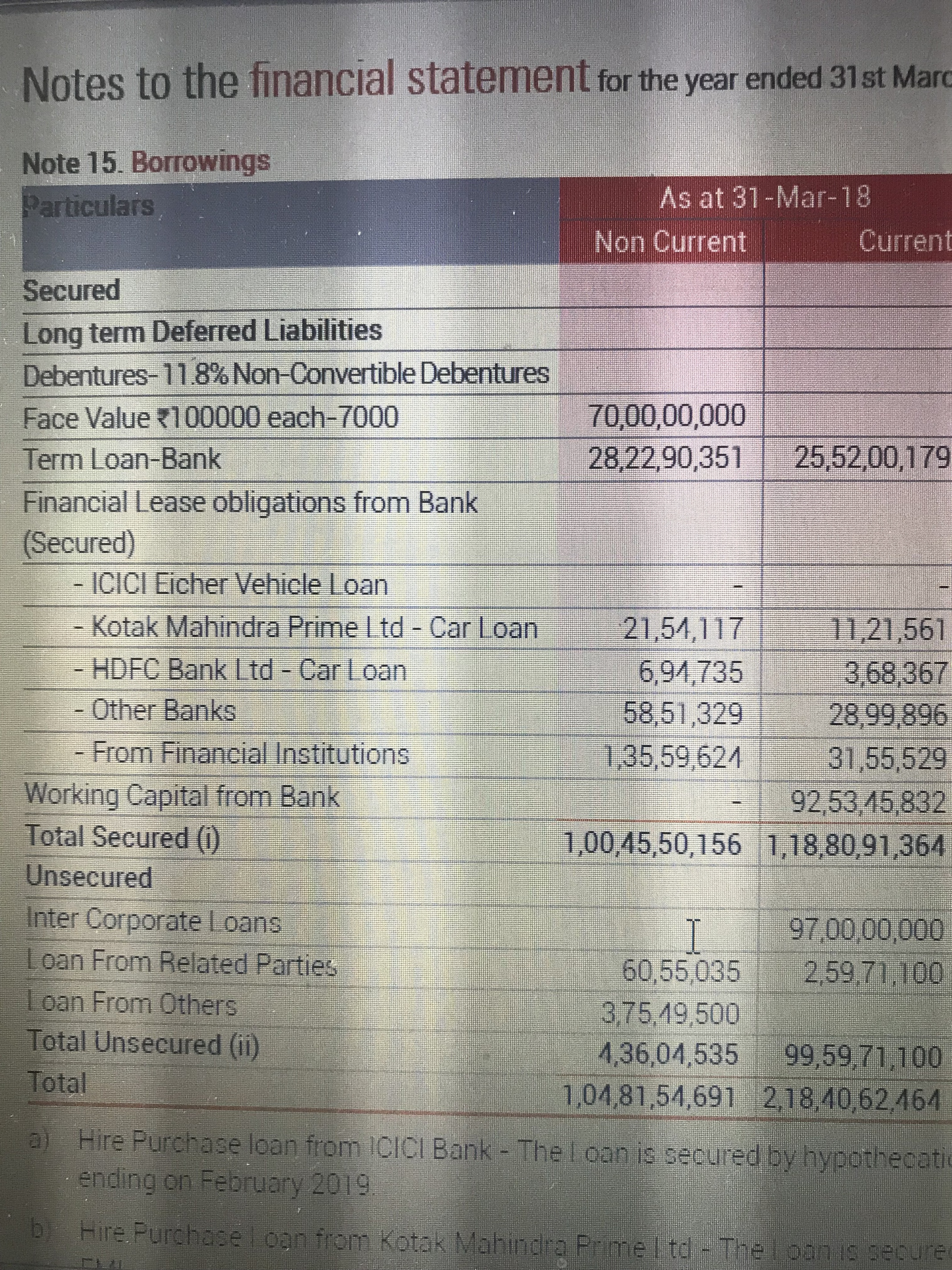

At standalone level company’s D/E is under 0.3 and at consolidated level it’s around 0.77 that’s a huge improvement from 2017 D/e of 1.5.

Sure debt has increased over 2017 but majority of that is in current form towards working capital and will be paid in 12 months time. The long term debt is borrowed for buying properties / offices and a deail break up and explaination of loan is given from page 180 onwards of AR.

Most of the debt shown is capital raised by issuing non convertible debentures which matures in 2020.

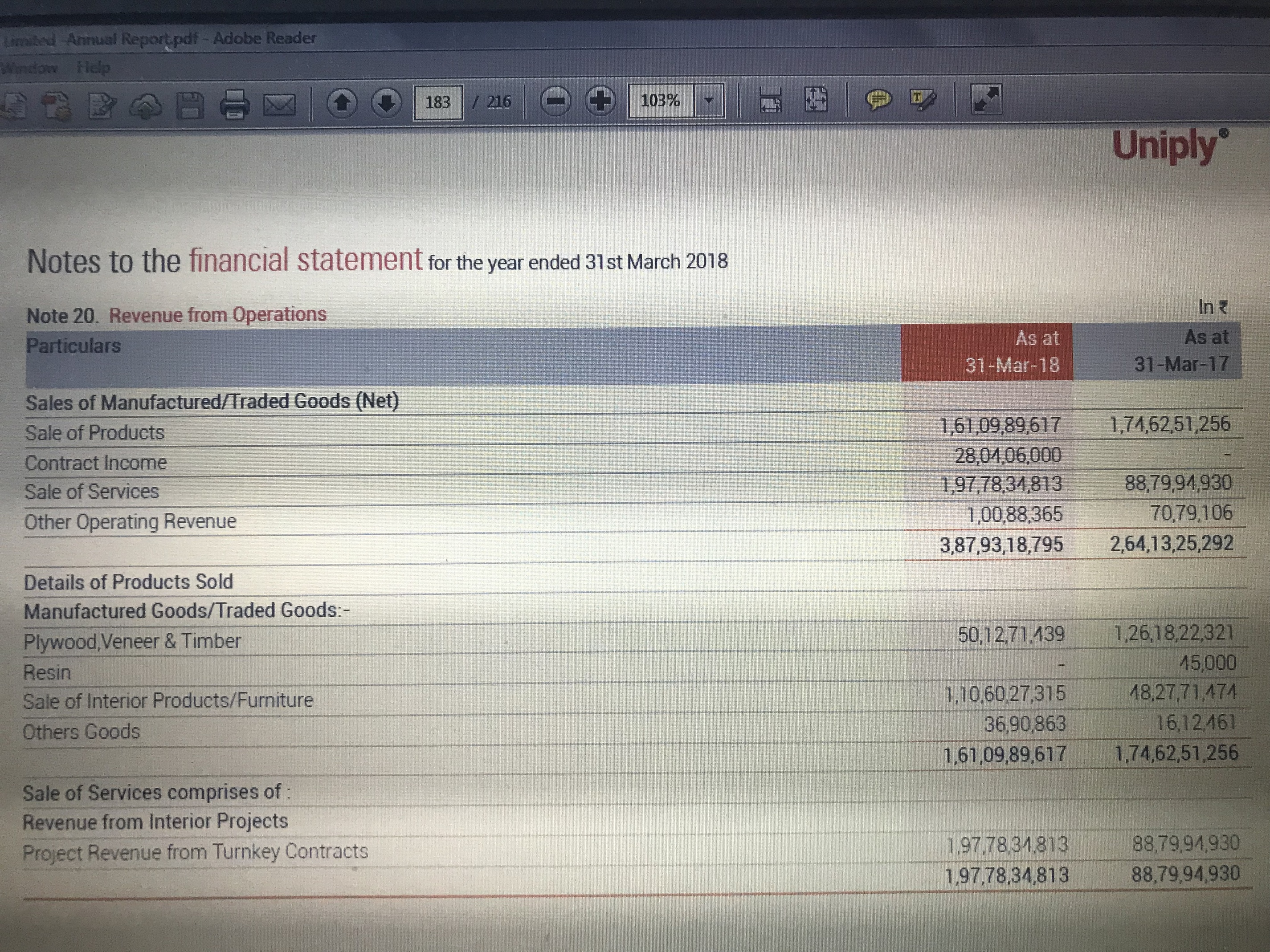

On sales from Diff division, this info is available on page 183 of AR

Promoter and group company has been buying shares from open market. They purchased additional 3 lacs shares through ‘ Madras Electronic pvt Ltd ‘ which is a holding company promoted by Keshav K and Srinivasan Sethuraman who is the CEO of Uniply.

2.27 cr (FV of Rs.2 ) of warrants have been converted to equity @ Rs.82 per share.

does such a conversion work in our interest ?

i mean, while conversion at a price significantly higher than the cmp gives a strong boost and +ve signal, the fresh equity dilutes our stake also? isnt it ?

I have been following this stock for last two years and was quite impressed with the way new management turned around the company from a low margin commodity business to a product and solutions company through getting into interior fit-outs and furniture. It looked like a master-stroke from the company as interior designing is highly un-organized and and a first mover advantage could pay rich dividend in long term. Moreover, it looks like a natural extension of core business with high margin.

But the way management has been trying to get into new area like construction of affordable housing, a complete non-core activity with completely different skill-set and high dependence on govt tenders, it looks like company is in a hurry and spreading itself too thin. We have enough examples before us where even the smartest of promoters have gone wrong if tries to do too many things in too short a period.

Just my personal thoughts. Having tracked the company for two years, it now looks like a long shot.

Hi, when they say construction of affordable housing, they aren’t getting in to actual core construction activity. They are just doing the fit outs of doors, panels and kitchen cabinets IMO which again requires plywood and other substitute as raw material.

Besides when you say company is stretching out too thin, can you please explain how ? They haven’t raised any sizeable debt, nor have any capex plans. D/E is very healthy at 0.77 and they wish to bring it further low in coming years. What he is trying is a master stroke of using existing capacities to its full potential, thereby achieving operational efficiency and intercompany synergies resulting in higher margins. New business of solutions require no capex at all and it’s basically just an investment in Human Resources.

Disc - invested and is 15% of my PF so views may be extremely baised.

It is not clear from the latest AR that company is actually looking at only fit-outs in affordable housing segment. If you read it carefully, at one place, it even talks about using particular kind of cenemt etc.

When I am saying spreading too thin, I meant that in last 3 years, company has gone from ply business to interior fit-outs to furniture and now construction. In the latest AR, they are even trying to make construction 75% of the top line in years to come. If so, you know where the mind-share of management would be.

I have also searched the AR and their website, but could not find very clear info about what"Affordable Housing Business" entails. Seems more like project management offering for building operations.

@ramanhp @ramdhawad

Uniply Industries is now into ‘active’ construction, and infra engineering of Affordable homes (and not in fit-out in form of doors and kitchens) . . . if you ref. to Annual Report 2018, you will note:

pg 19 says:

". . . the Company achieved attractive status - Grade A, Class 1 contractor (PWD) – within a

short time of entering the affordable construction business."

pg 61 says:

“Uniply reported project wins in affordable housing to the tune of INR 636 crores. Currently, the Company is executing two turnkey projects in Hyderabad (from design to build) of 2,700 and 2,200 homes of 350 sq. ft carpet area. The Company is also in the process of beginning work on a 4,000 affordable home project in Jagtiyal, Telengana.”

pg 91 says:

“The Company is also in the process of commencing work on 12 other affordable housing

projects (three in the Nizamabad district in Telangana and nine projects across Karnataka).”

pg 113 says:

“. . . During the year Company sold its Manufacturing Division on slump sale basis and have entered into Construction Business. However, it continues to trade Plywood. The company is presently in the business of development of infrastructure facilities on Engineering Procurement and Construction basis (EPC) and undertakes contract from various Government and other parties.”

The company now does 3 things:

- via UNIPLY INDUSTRIES (i.e. the main co.) focuses only on Affordable Home constructions and has as AR order book of 636 Crores. in the yr ended on 31 March 2018 it booked revenue from this business of 35 crores (and spent 22 crores). going forward aims to increase share of this segment. pg 29 says, ". . . expect to arrive at a stable balance of 75% revenues from the construction business and the rest from interior infrastructure projects. . " this division now wants to do 1200 crore p.a. turnover in 5 yrs

- via VECTOR PROJECTS, fully owned subsidiary, focuses on interior fit-out and building solutions (read electrical, AC works etc) projects for Offices / Residences. this division wants to do 700 crores p.a. in 5 years

- via UNIPLY DECOR (the associate co. to which it sold the entire Ply manufacturing business, and now owns 37.14% in it) focuses on supply of Ply and Veneer for its projects by way of getting 37.14% of profit + annual royalty (I think 3.75 Cr. per yr) for using the Uniply Brand. This division, as they say, has the potential to do 500 crores p.a. in 5 yrs.

Additionally,

the company has announced that it will merge100% into it Malaysia’s leading design and furniture Artmatrix, with the intention to also have a business of modular furniture for offices and for direct online sales too! https://www.indiaprojectsnews.in/news/uniply-industries-acquires-artmatrix-technology-2662463

CLEARLY THERESE A LOT GOING ON WITHIN THE COMPANY!

Thank for your reply. Have written to the company secretary for providing more details on exact nature of work that they do in this segment. Although Company’s website does provide a clarity and support your findings.

The 30 lac sqft of affordable housing business in Telangana that company talks about in the AR seems to be a interior fitouts business. See below from their website.

I note. . . but its overall a dynamic situation. A lot of info is somewhat getting overlapped. one needs to get clarity

-

it needs to be clear - Is the company is into the construction of affordable housing (i.e. brick, cement etc) ‘OR’ only is into the construction of interiors (say doors, windows, kitchenette. . . anyways in affordable houses these would be of only standard specs ) . . .

-

it needs to be also be known if being into both ‘constructing affordable house’ AND 'constructing premium IT tech park" at the same time are true . . .

In my pov. . .

- To be in ‘affordable’ and to be in ‘premium’ segments at the same time is a proverbial oxymoron! both have very different sensibilities and can’t be run within the same organization at the same time and that too in a nascent stage.

- As well all know the MD is overambitious and has actually delivered in recent past. . . but is all this now a speed overkill??

So, as per the info on company website / AR, and based on my thoughts by interconnecting information, there are 4-5 service areas wherein the Co. operates:

- Architectural & Design + M.E.P. + Interior Fit-outs: i believe all three are Via Vector Projects

- Furniture & Furnishings: again partly via Vector Projects (i.e. modular furniture it fabricates), and also from the announced Aramatrix (Malaysia) merger (that makes international design premium furniture).

- Civil Development (Affordable Homes and SEZ Office buildings): Via the Main Co.

- We should also add the Royalty + 37.24% profit on a/c of the sold ply business sold to Uniply Decor

Now let’s explore the overll progress of the company. . .

Step 1: the change from old Uniply to new Uniply (focusing on better quality, removing low take off items, adding new plants in other geographical areas) was an understandable transition. . .

Step 2: Likewise, the acquisition of Vector Project to get into interior fit-out space was logical and in fact the smartest of the moves this far (additionally, harnessing of the ply biz alongside). . .

Step 3: Also accepted is the approach to be one-stop-solution to provide Infrastructure / MEP services (Mechanical, Electrical, Plumbing), to the fit-out projects of the clients is great too!

Step 4: the proposal to merge in Malaysian Aramatrix (to include their premium furniture for into their fit out projects and also online sales) though slightly tangential, is a quite good idea indeed. . . .

but … .

Step 5: GETTING INTO HARDCORE CONSTRUCTION OF BUILDINGS (AFFORDABLE HOUSING AND SEZ OFFICE BUILDINGS) seems too far-fetched right away. . . it’s not really a logical progression of all the last 3 yrs of re-organization.

. . so in the end, considering we know (from pg 29 of the Annual Report) that the Co. wants to be in 75% Construction: 25% Interiors Fit-outs. . . We thus, need to evaluate it more like a construction/developer Co. . . . and thus the question is: SHOULD WE BE PAYING 30-40 PE multiple to a company who is new into the construction business.

disclaimer: not invested, but considering

If they are aiming to get 75% of their revenue with construction of “affordable housing” so it should be consider a RE company & same multiples to be given to this company. I was wondering, if they wants to go into construction business then how they will get funding for these projects, as getting funding for RE companies are getting difficult day by day or they are just PWD contractor and getting paid on completion of part projects, its all confusing and they is reflecting on its price movement these days… I didn’t understand the reason for stock split of a ~450 Rs stock which make this company looks a penny stock (~50 Rs)… Surely promoters are trying to do “too many things” including playing in market to get the better valuations which in turn is working against them (at least price movement is showing that).

Disclaimer: invested, but decide whether to remain invested or cash out with “loss”.

on pg 15 in AR they say “The fit-outs business is working capital-consuming, the affordable construction business is working capital-negative and the plywood business is working capital-neutral – an attractive and scale-able mix”

my view:

. . .the housing construction used to be working capital negative (3-4 years ago, when RE was on a high and people flocked to invest in new launches and paid in construction linked plans / subvention schemes, making working capital negative), but not anymore. . . today customers cherry pick from well progressing projects or even once they are ready . . . and to say that govt. funded affordable housing is WC -ve is very difficult to digest; when does govt. pay in advance for next stage of construction???

disclaimer: not invested, but wanting to. not getting confidence though!

As per my understanding, these affordable housing projects have world bank as the partner, uniply is only involved in fit outs and not construction…

Hi. kindly, for our benefit share what’s the basis of your ‘understanding’? . . . as I have posted above the multiple excerpts from the Annual Report whereby the management has clearly stated about it now being in the turnkey construction of affordable homes and sez office buildings

Yes in their AR they clearly mentioned that they awarded PWD contractor agreement, I dont know why ppls here are not reading the AR and SPECULATING that “this might be” or " that might be"… Uniply expecting more revenue from Civil work than fit outs and working with PWD as contractor you know which skills is needed and that the reason this stock is getting hammered each day.

Circular trading cited for Uniply in this article. Seems like a cause of concern in case the referred transactions were undertaken post management change. The article mentions that the charge sheet was filed in Aug,2017.

Is there any way to understand connection of mentioned director Jagmohan Kejriwal with Uniply?

Case of concern here. Can somebody check with the management of Uniply? I have send them an email on the generic id - info@uniply.in