Starting to exit today. Great ride from 40 to 123. I cannot justify my investment just because Damani is in the stock.

Cheers to all who pumped in at 40-45 area!

Neil

Starting to exit today. Great ride from 40 to 123. I cannot justify my investment just because Damani is in the stock.

Cheers to all who pumped in at 40-45 area!

Neil

“Words have a magical power. They can bring either the greatest happiness or deepest despair . Words are capable of arousing the strongest emotions and prompting all men’s actions.”

Sigmund Freud

WOW…A Untested young man -a few well articulated words - A multibagger .

Kudos to Neil and rajpanda for spotting it, riding it and exiting with a clear head.

Hi just read the Uniply Annual Report,

little disappointed that new management lost the chance to communicate its strategy to Shareholders

there are lot of people who are putting faith and money with the new promoters.

Was expecting some thoughts and vision for the future of company

Manoj

just ready the Annual Report and was disappointed that new management did not communicate its strategy , vision to new shareholders who have put out huge faith and money behind them.

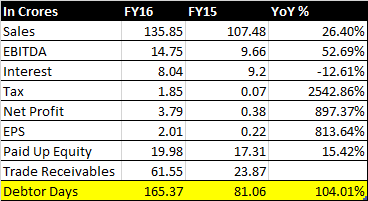

Results Announced:

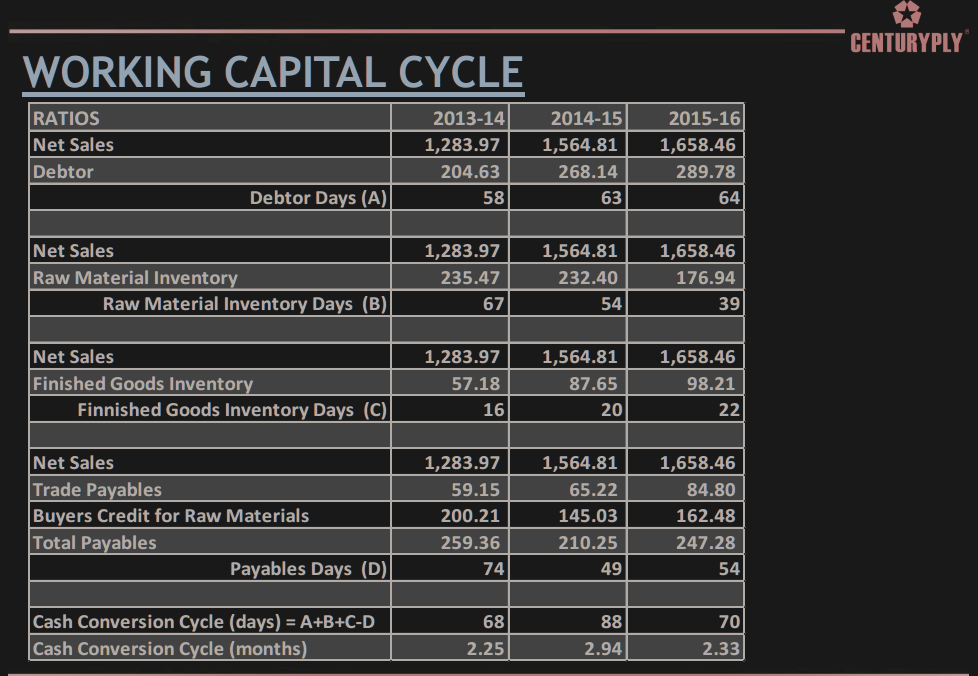

Would like a second confirmation on the Debtor days figure.

It is a big concern on an otherwise good set of results considering it is a turnaround company.

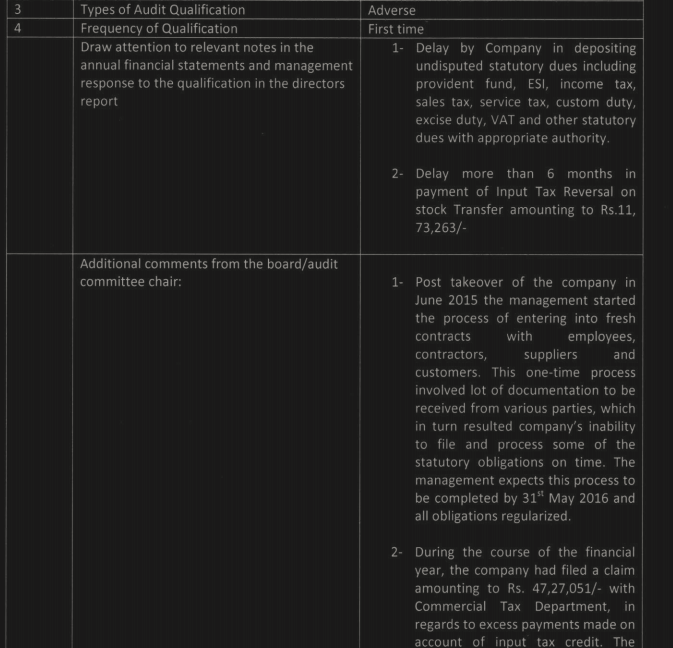

Whilst the Company has made profits for the year ended 31.03.2016, the Board is unable to recommend a dividend until the prior accumulated losses on the book turn positive. The accumulated loss at the start of the year was Rs.9,41,01,925/- and currently stands at Rs.5,61,81,474/-, post adjustment of current year profit transferred to revenue reserves of Rs.3,79,20,451/-.

The Board was appraised on the progress of the planned asset acquisition of M/s. Euro Decor Private Limited’s Plywood & Block board unit at Bachau, Gujarat. Post completion of legal and statutory formalities, the Company is expected to enter into definitive sale agreements by 31/05/2016. Further, the Company estimates production from the said plant to commence from 1/07/2016.

Negative Audit qualifications - IMHO i would have been worried if there were dues. But here it was a delay with a reasonable explanation. Will wait for further management commentary before classifying it as an ignorable risk.

Disc: Invested. Not traded in last 3 months.

Hi Vishnu,

I think debtor days calculation is correct.

Based on the feedback I have got from few people, mgmt. has been very aggressive, trying to add new distributor/dealer in new geographies in the last year. I think that could have added a bit to the receivables due to the credit granted to such new dealers etc. for the initial stock.

However, if we look at the decreased inventory (44.96 cr. Vs 66.61 cr), it does a bit to counter balance the working capital requirement vs the increase in debtor days.

Overall, will it be good to track the Working Capital to Sale Ratio instead of just the debtor days? Working Capital to Sales ratio has decreased from 1.8 (FY15) to 1.49 (FY16) ? Though not strictly comparable on YoY basis, given Uniply’s story of promoter trying to do multiple things over the last year.

Maybe, need to check & compare, what’s this ratio for top players like Century/GreenPly.

Hello Raj,

Very reasonable explanation.

I made a mistake of taking debtors in isolation, while as u rightly pointed out it should have been a holistic calculation considering Working capital and each of its individual components.

Greenply has not yet announced its results. Attaching the below slide from Century presentation for Q4FY16. It tallies with ur point about working capital improvements not being specific to Uniply alone.

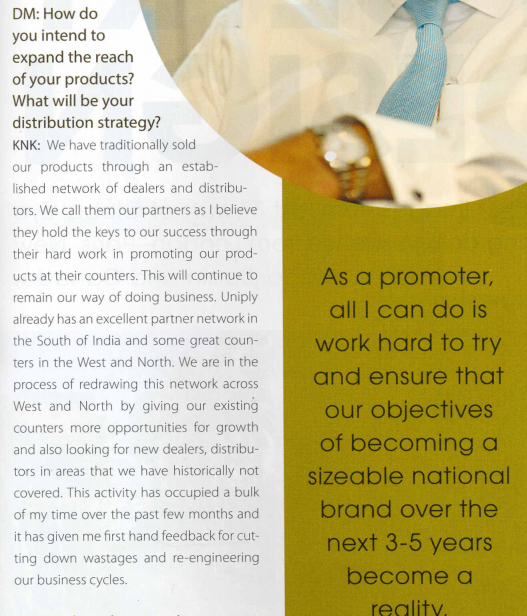

Coming to the dealer additions, i found the below interview dated Nov 2015 where Keshav said most of his time this year was ramping up the dealer network in North and West India.

From the same interview, he gave an excellent and very prudent response when asked to comment on the meteoric rise in share value from Rs 6 to Rs 150 in last 15 months.

Another point which i want to highlight is the revamped website.

Based on historical snapshots, it seems to have happened between Oct 25, 2015 and Jan 11, 2016.

Have to say it is good to see tangible progress at least.

Regards

ET Now: Your costs have increased significantly. It has clearly caused a huge margin compression as well as a PAT de-growth. What is the reason for this? Is it going to continue?

Keshav Kantamneni: No, our EBITDA margins have actually gone up. The main reasons are we perked up our employee cost as well as the overall infrastructure for a much larger sales number in the years ahead. Because, the manufacturing business takes time to build up. After that the business service has to be taken to the larger dealer network across India. So, the costs have stabilised for the future growth potential of the business.

It is actually a gain. The margins have gone up from about 10.5% to about 13%. I expect that will continue to improve and touch 17-18%.

ET Now: Doesn’t the margin stands at 10% versus about 29.5% last year?

Keshav Kantamneni: The EBITDA margins I am looking at are about 13.5% versus 10.7% last year. The ply wood business margin lies around 17-18%. This was an acquisition we made last year and the business required a certain focus on cleaning out the existing team and revamping the whole system for a long term growth model. So, we have not really looked at costs this year. Costs will be a focus going forward.

ET Now: What is the current capacity you are operating? With EURO Decor acquisition, what will be your capacity?

Keshav Kantamneni: We took over the business last June, there was a management change and since then there has been a gradual uptick in capacity. It was about 35% when we took over and we are running close to full capacity right now. We had some issues with the Chennai floods and it took some days off in the month of December. Apart from that, the business has been running at high capacity there. The EURO acquisition is about two times of our current capacity so we are looking at significant upside once that business starts. Moving ply wood from south to north is not as attractive in medium range brand. The higher end products do sell but the focus is on the medium and low grades. I think that plant will add more value in terms of volumes as well as margins going forward.

Company notice

Uniply Industries Ltd has informed BSE that the Board has allotted 934269 no’s of new fully paid up Equity shares of Rs. 10/- each on preferential basis to Non-Promoters of the Company at Rs. 156.70/- per share at their meeting held on May 17, 2016.

Pursuant to these allotments, the issued, subscribed & paid up equity capital of the Company has increased from Rs.19,98,17,430/- to Rs. 20,91,60,120/-

The equity shares allotted as above shall, rank pari-passu with the existing equity shares of the Company and shall be entitled to such dividends and corporate benefits, if any, declared by the Company after the allotment.

I suppose, This is for the acquisition which cost 42 cr. and they planned to raise 32 cr. debt and 10 cr. cash, but instead they raised 15 odd cr. cash. So dilution of about 4.6 % equity.

@rajpanda Today Uniply Ind announced an Open Offer to acquire 26% stake in U V Boards at the rate of 13.50 per Share. This Offer is Open for both Promoters and Public shareholders.

One of the promoter entity Dugar Merchandise is selling half of their holding.

Mr. Keshav Kantanneni has acquired 8.78% of UV Board of the fully paid up equity share capital of the Target Company along with complete control and management of the target company through SPA.

Open Offer Price is similar to Uniply Ind as they have acquired in 2015.

What would be the future of the company and what is the impact on minority shareholders. Subject matter Experts please share your experience on the same.

Could not find any thread for UV Boards so posting here as promoter group is same and Uniply is acquiring Company.

Thanks.

Disc: No holding in any company.

There were rumours about this acquisition for sometime in the market. Finally it has materialized.

So going by the announcement, Uniply has invested about 1.34 cr. for acquiring 8.78% and now the open offer is for 25% @13.50 at investment of 5.35 cr., which can take the stake upto 34.78%.

We will have to see market reacts to the open offer.

Going by UV Boards AR, seems like, less than half of their revenue came from manufacturing and the other half from trading. I couldn’t dig the capacity info for UV. Company’s FY16 balance sheet shows good improvement though. Will have to get more details.

Thanks for sharing the interview Vishnu. What should one make of his answer to the sourcing logs question? I thought using his investment bank to source from forests in countries across the world seemed a bit credulous.

I would wait for the Annual Report to find some commentary on the sourcing aspect along with a broad overview of the vision and agenda of the management.

Ideally i would have expected it in the last AR itself, but it is understandable if Keshav had more pressing matters to deal with. Besides he had used alternative channels to express his views.

Coming to your query, I would like to express a tangential view on this subject -

Given the recent wildfire in Uttarkhand and annual recurrence of bush-fires in countries like Australia, US and others, and the not so effective management of them. Some of the salvageable wood could be used for sourcing.

But the more important point is that somewhere down the line in future, maybe one can expect with evolving technologies and predictive analytics, we could eventually have proactive strategies to suppress/restrict the amount of damage caused by the forest fires. Apart from the loss of habitat, there is also impact of climate with the release of CO2.

While, philosophically humans have never been adept at maintaining the natural balance, or sticking to the adage - “Nature knows best”, maybe one can still hope that with the recent thrust into organic farming, biodiversity, climate change, etc… we have turned around the corner.

To reiterate, i think it is too early to comment. As stated in the same interview his immediate priority had been to strengthen the dealership network and operational efficiency.

Probably he might come around to fixing the sourcing aspect this year.

Lets wait and see.

With the acquisitions like vector projects the company is going to grow 25% plus per year because of the additional stream of revenue.

Uniply although quoting at 100+ PE has a tremendous opportunity to grow as it has a market cap of only 631 Cr. Although very richly valued in terms of PE, I think we should focus on the market cap vs size of the opportunity.

Thoughts?

Hi Uniply Board,

I am looking to invest a sum of money in the Plywood sector driven by Shift from Unorganized to Organized, 15%+ growth rate for the sector over the next 5 - 7 years etc.

Looking to invest either in Greenply , Uniply or Sarda Plywoods. Can you please give me some idea about how I should think about this and your recommendation?

Regards

Naishadh

Nudging this up - The initiatives of this company require people to sit up and take notice - Those who have a position here , humble request to share your information and knowledge here.

In uniply seed funding is provided by radhakishan damani and other ace investors.

Uniply has taken 8% stake in UV boards and future plans to raise stake at cheap valuations.

Uniply is focusing on product with higher margin.

Does anyone here have an idea about what’s happening in uv board? The stock has been put in gsm…is this done on purpose so that the shares can get cornered? Any1 have an idea?

Open offer made for 37% of UV Boards @ Rs. 25

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=961c9b3f-0961-44b3-88d9-91798670cd60