@rajpanda I have been following Uniply for about 3-4 months now ever since the management changed. I got the opportunity to talk to Keshav couple of months back and it did look interesting to me as well . I followed up my conversation by doing some on-ground research I did some scuttlebutt in Gurgaon and found that Uniply is an unknown brand. No one keeps it. The ATS no one acknowledges as a product and mostly people just dish it. I also through a friend got some feedback from the Chennai market In Chennai nothing has really changed (This was done very recently). I also spoke to an ex-employee who shared that they are extremely small in TN markets such as Coimbatore, Madurai etc

So at this moment, you are really taking Keshav’s talk on face value without any numbers and also the claim that they are leaders in TN is in question as per my feedback.

Now coming to the industry- my reading after doing scuttlebutt and going through the numbers of all the listed players is that the market is extremely competitive. Most players like Uniply are debt-heavy and they make average returns at best. If you just go out and ask for a ply you will be swamped by options and you can’t really make much difference between a Rs 50 ply and Rs 150 ply. The implication of this is that brand creation is extremely difficult, only Green and Century have been able to create some brand recall- that too after so many years of investing into S&M.

From whatever data one could gather, it would be very difficult for someone to build a ‘brand’ in this market, especially coming from behind. Sure GST will help, and the move towards organized trade will help, but I would wait for the basic financials to improve.

Bulk of the trade still happens in cash-even for branded players, that’s a risk too.

The share was taken up to 37 and then dumped to 20 bucks a while back and it has now started its surge again. Its always a bit uncomfortable if the shares only do a UC or an LC and that too consistently.

Net net, Prudence would be to wait and watch and if the story plays out then you can still make a good return, but right now the risk reward is not very much in your favor.

I guess the negativity is good for the stock!! Thing to consider is that Century and Greenply are running at above 100% capacity at the moment.

Greenply incidently is now focusing on higher margin MDF business and has started outsourcing traded ply for growth as of now.

I was at yesterday’s Greenply Investor meet in Mumbai and they were very clear on the benefits of GST…it is going to DESTROY the unorganized ply players who avoid the tax net by being below 1.5cr turnover while GST will be applicable to anyone with 15lakhs annual turnover.

Coming back to Uniply, they are barely at 55%-60% capacity at the moment and they are in the process of boosting dealer networks and ply capacity over the next 12 months…so by the time GST becomes a reality in 2017, Uniply could be a major beneficiary!

If you sit and contemplate Keshav as an entrepreneur, then you are COMPLETELY MISSING the bigger picture of GST and its implication on the plywood industry!!!

Even Greenply yesterday echoed Keshavs thoughts on explosive growth coming for organized players and they explained how and why it will happen! Its amazing whats coming in this sector thanks to GST.

**GST is going to be a gamechanger for many companies and sectors…its a DISRUPTOR…it will completely change everything.

If you think Uniply isnt your cup of tea…go for Century or Green atleast and do not miss this bus.

Neil - I have no hope on GST making it through the LS+RS route in 2017 and in fact ever seeing the light of the day. The GST bill discussion started in 2000 (yes - I mean 2000). In 15 years, there is not even basic agreement and there are so many push and pulls in this country. By the time 2017 comes, Modi/BJP priority will be 2019. A move like GST will hurt small players and they will make hue and cry that the ‘common man’ / Garibi is hit in the stomach etc and Modi will be blamed for siding with the mega industrialists and corporates. Like land bill, it will be referred to numerous committees and panels and eventually, the next priority will be to somehow catch the seat of power than do good for the nation.

Of course, this is off topic and we can discuss it elsewhere…coming back to Uniply, I wouldn’t like to just bet on the GST being game changer. Anything to do with Government will mean a pile of uncertainty in my books and above all, logic goes out of the window

This sudden spurt of price has left me little confused on what’s going on.

There is no doubt, this story is a kind of “hope story” about a rosy future compared to companies past as it’s not backed by consistent financial performance history. For me, this is a kind of experiment with a low allocation.

Disc: I am still contemplating sell or reduce. Watch out for your own interest.

Board Meeting on July 25, 2015

Uniply Industries Ltd has informed BSE that a meeting of the Board of Directors of the Company will be held on July 25, 2015, inter alia, to consider the matter of issue and allotment of equity shares of the Company on Preferential basis to the Promoter and other investors along with other agendas therein.

Uniply Industries Ltd has informed BSE that the Board of Directors of the Company at its meeting held on July 25, 2015, inter alia, has approved the followings:

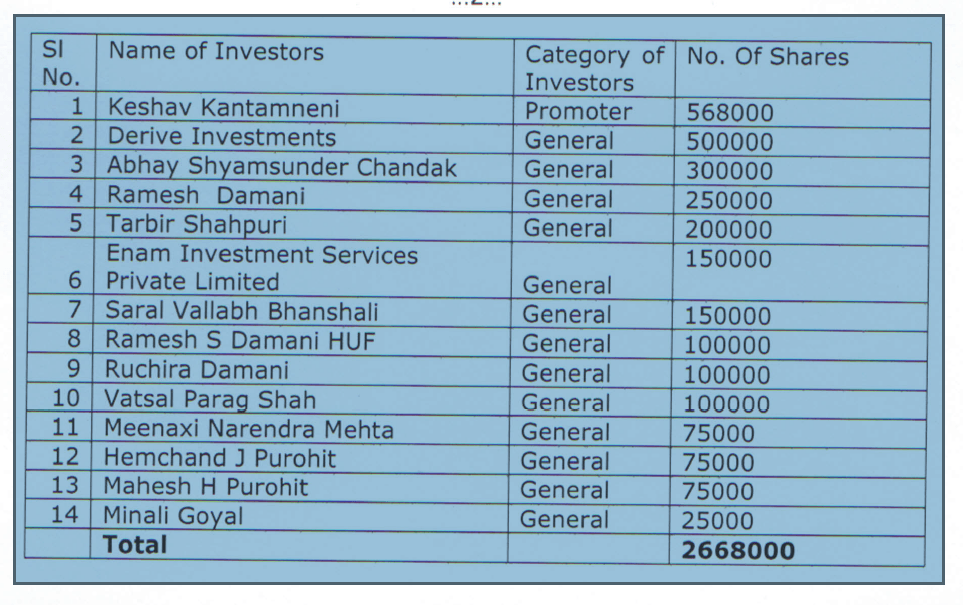

The issue and allotment of up to 26,68,000 equity shares of face value Rs. 10/- each, on a preferential basis to the following promoter and non-promoters for a total subscription amount of up to Rs. 26,68,00,000/- (Rupees Twenty Six Crores Sixty Eighty Lacs), at a price of Rs. 100/- per equity share, in accordance with the applicable provisions of Chapter VII of the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2009 (“SEBI ICDR Regulations”). The Issue and allotment of equity shares of the Company on a preferential basis, shall be subject to and in compliance with all applicable laws including without limitation the provisions of the Companies Act, 2013, read with the rules framed there under, the SEBI ICDR Regulations, the memorandum and articles of association of the Company and the Listing Agreement entered into with the relevant stock exchange and subject to the approval of the shareholders of the Company in the Annual General Meeting of the Company for the financial year 2014-15 and such other requisite approvals as may be required.

Total No. of shares goes up from 173,137,43 to 19981743. A 15% dilution at a good price.

Isn’t the price determined by SEBI’s formula and as such the promoter has no real say in it except delaying/doing the allotment when the price is dirt cheap.

I think you are right. What am not able to understand is, what could be the motive behind this delaying of decision on dilution. The same could have been done at say 50/- giving more equity to the promoter or same equity at lower price ?

Any thought’s ?

That’s ok Rohit. This wasn’t a high conviction bet for me too. So got out seeing the very high returns in very short time.

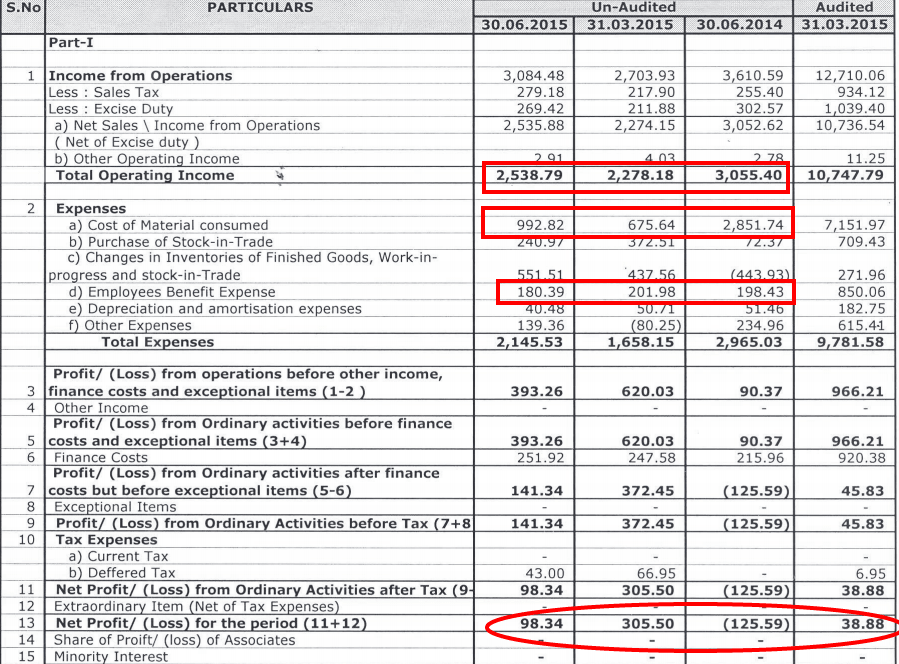

Market in it’s wisdom is currently valuing the company at 230+ cr. mcap + debt of 50 odd cr. (subtracting the equity (cash) raised from debt). This is for a company which will probably just about manage 4-5 cr. NP this year if last Q’s rate is taken as normalized rate.

Hard to understand for me, so i gave up