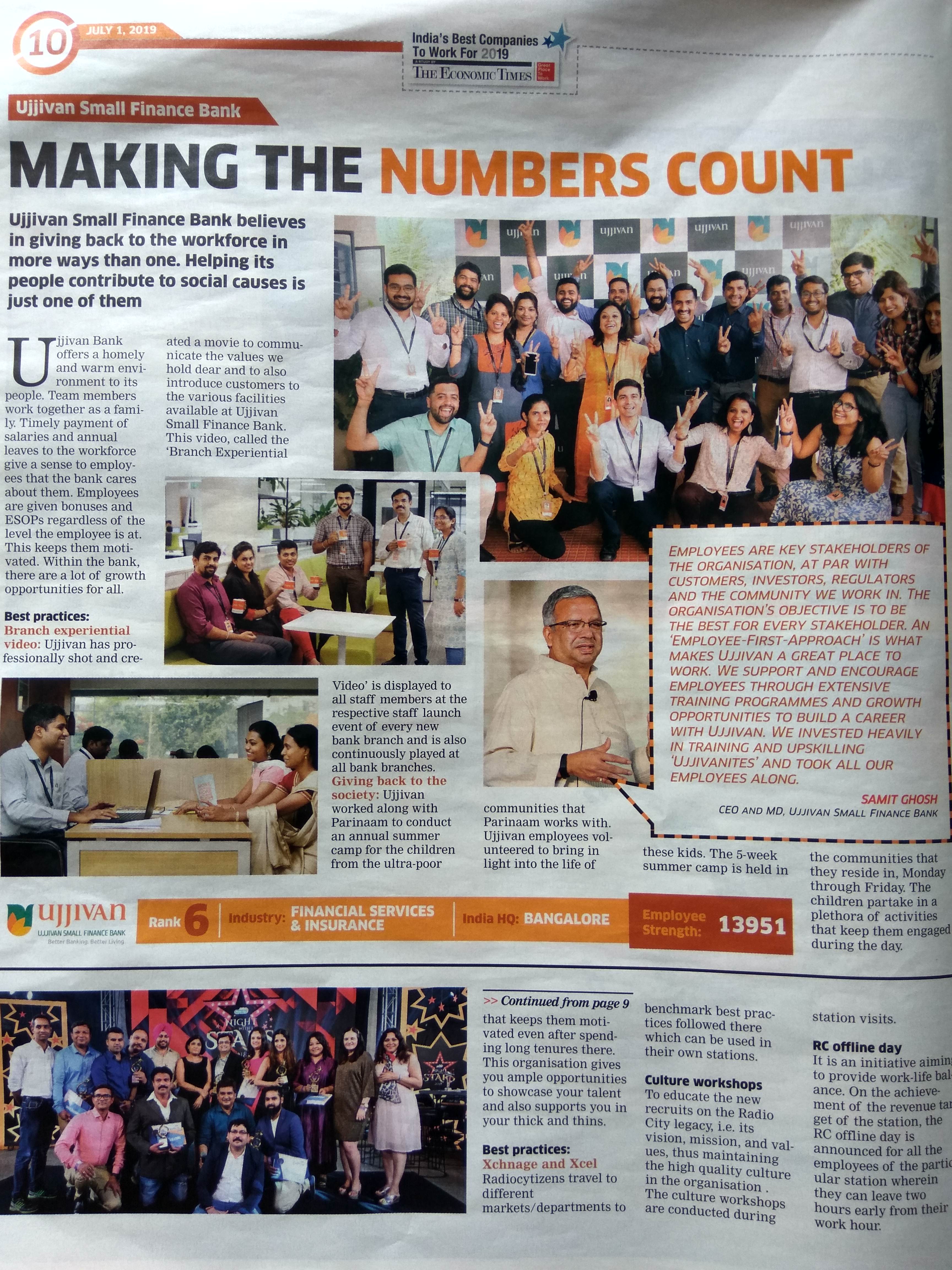

Happy employees mostly result in happy shareholders. Ranked 6th in best companies to work for in top 100. Quite an achievement I must say.

How did you know about that? What was your source? How “well know” were they? As far I could recall no body talked about them. Company didn’t say anywhere that it is IPO of Holdco.

So first it may become holding company and will reduce stake significantly in phased manner…means it will be discounted as holding company? Am I right?

it is already a holding company & there is already some discount due to this, IMO.

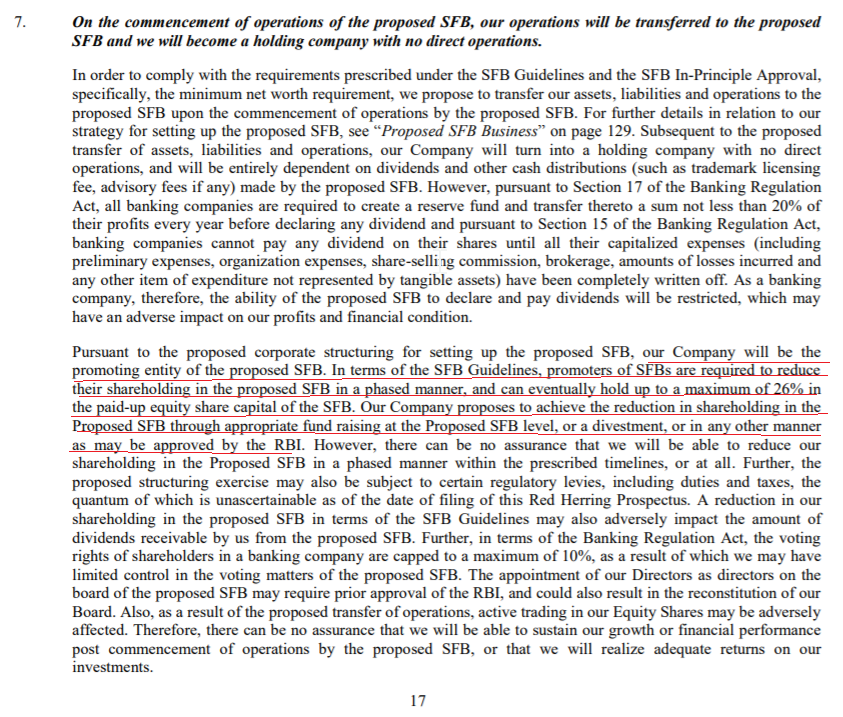

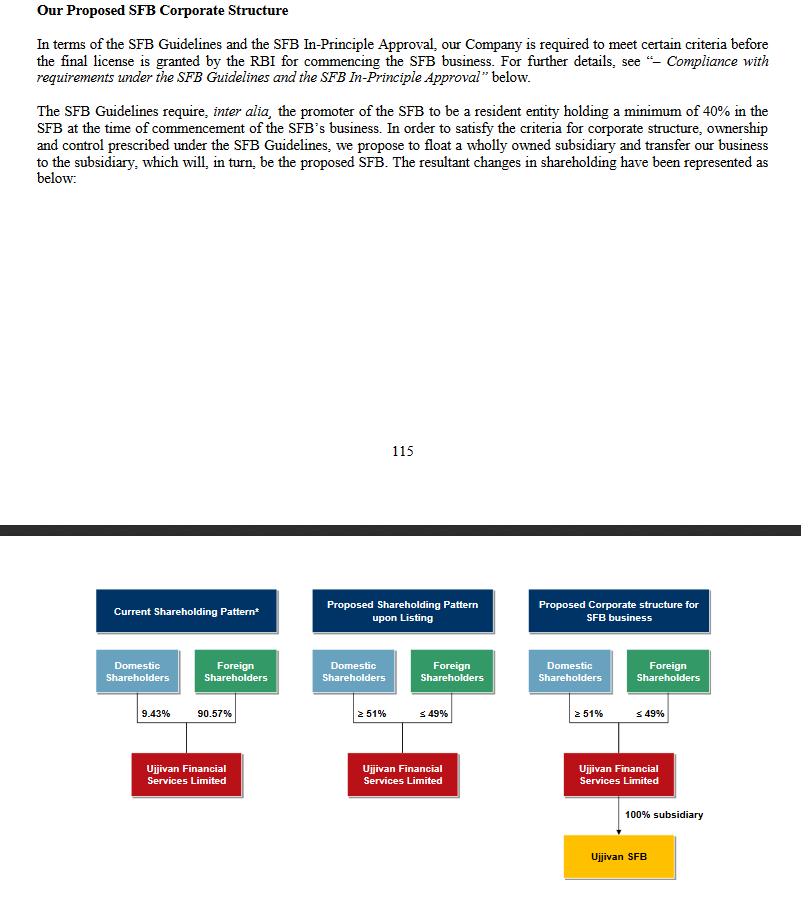

From the Ujjivan DRHP:

Clearly states IPO is of Ujjivan NBFC

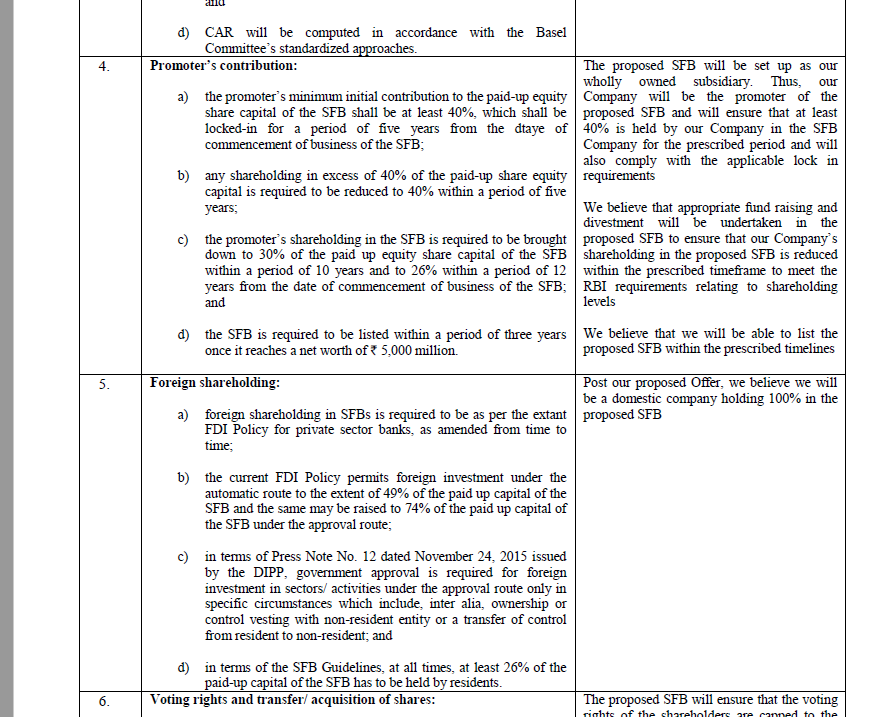

Clearly states NBFC is recipient of a SFB license from RBI, which they propose to set up - entire subsection devoted to this

Clearly states proposed corporate holding structure for the SFB

Clearly states the listing requirement and their plan for the same

RHP of Ujjivan FS has total 408 pages. You are trying to tell me that you read RHP of Ujjivan FS and found out the it’s a holdco & operational company will be listed in future.

If you did so kudos to you. As far as I am concerned I could not read 400 pages RHP before buying from secondary market. But I followed all the management interviews, didn’t hear a single work from their mouth till recently.

All these points are covered in 7 pages in the Summary of Business section and further 7 pages of SFB section. Business summary and financials should at least be perused when browsing a DRHP.

1 Like

More power to you sir.

Just to clarify I did not read 400 pages of the RHP.

Any idea how the holding structure of equitas is different from ujjivan? why there is a difference in future listing?

By Q1 results or by AGM next month things will be more clear. Definitely management will try to have a concrete solution by then as they have to face investors.

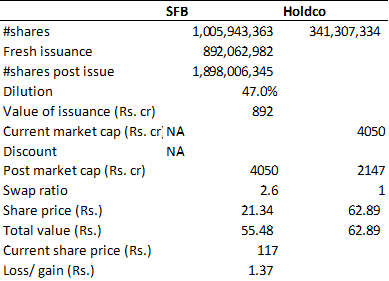

Hi @eshwar , there is no difference in the holding structure of the two entities, Equitas also wholly owns its SFB and the holdco is listed. Equitas has proposed to list its bank by issuing fresh shares of the bank to its existing shareholders in the holdco (in the ratio of their shareholding) amounting to a 47% stake in the bank. Each shareholder will receive approx 2.6 shares of the SFB for 1 share of the holdco. There will be no cash consideration and the consideration amount of the issuance will be adjusted against the bank’s securities premium and reserves. Equitas will then approach SEBI to directly list the shares of the bank on exchanges - till SEBI approval the SFB’s shares will be locked in demat. I did a rough working of the impact of this assuming that the bank will list at Equitas’s market cap today (approx 4050 cr) and Equitas market cap will reduce to its value of 53% holding in the bank.

Scheme available here: https://www.equitas.in/holdeqis/pages/forms/uploads/sei-soa-bse-nfsa-draft_scheme.pdf

Management discussion here: https://www.equitas.in/holdeqis/pages/forms/uploads/fipr-eaic-qct-nf-ehl---q3fy19---conference-call-transcript.pdf

Working for Equitas SFB

With a holdco discount, there is likely to be a loss here for shareholders. Given that a merger is the most natural way to achieve the 40% dilution requirement in 2.5 years, imo the holdco value should not be discounted as it is as good as having a buyback attached to it for proportionate value in the bank. I think Equitas’s proposal, due to the approval requirements, is a bit riskier as SFB shares will be liquid till the listing is complete. There is also no price protection being given to investors to hedge against declines in their holdco share price - value preservation depends on the listing price of the bank. As against this, Ujjivan’s plan seemed to be to make a small IPO via the normal route but via a fresh issue to existing shareholders at a preferential price - on the surface, not sure, but this seems less regulatorily risky, and contains the price protection element, further by only diluting 10% of the bank, they reduce the risk of the holdco discount.

4 Likes

this can be big in longer run, execution is key…

1 Like

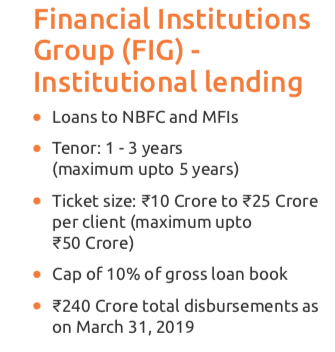

This screenshot is from Ujjivan’s FY19 AR and raises a few questions:

This screenshot is from Ujjivan’s FY19 AR and raises a few questions:

- Why is Ujjivan lending to NBFC-MFIs?

- Won’t this lending be a low return (compared to 20% that it makes on its regular loans), higher risk & higher ticket size lending?

- Rs 240 Crores is a small part of the asset book (about 2%). But its the message that is unclear to me. Is the bank unable to find borrowers in its low-ticket MFI or regular loans?

- Or is this mandated by any regulatory requirements? Or is it due to non-financial considerations such as goodwill with funders & with an intent to help out others in times of difficulty

Any insights from long time watchers of the company?

1 Like

Ujjivan posted good results, but some big folks already know about it a day ago.

The average volume of last month is around 2M, yesterday it was 8M!!. That too when nifty, small and midcap cracked around 2%. Shows how certain they were about the event!

3 Likes

Q1FY20 Conference Call Update

All prospective and current shareholders should definitely go through this quarter’s conference call as a lot of questions were answered about the IPO listing, holding company, the scheme of arrangement and a possible reverse merger.

As per my understanding of the call, the reverse merger will not be as easy to enact in future as I previously thought it to be. Refer to the question asked by Mr. Amit Nanavati on Pg. 16. The shareholders of the USFB will be different in the future, and the reverse merger voting will need 3x (75%) voting for or 51% of regular shareholders, excluding the promoters, who are the current shareholders of the holding company.

RBI is supposedly coming out with new norms in August, which should open the door for a reverse merger in the future. There is also talk of collapsing promoter holding after 5 years.

Scheme of arrangement for Ujjivan as followed by Equitas is also causing confusion in the investor’s mind. In some interviews, the management says our structure is different, in an article (refer below) I read that they do not have enough free reserves to follow the same, and in the conference call, they are saying they have left that possibility open.

The current situation is that they are observing whether Equitas gets their approval of SoA from SEBI to which they had applied back in Feb. After this, Equitas will have to apply to NCLAT, which will take another 6 months. So Equitas in their Conference Call said that they will apply for an extension to list to RBI. Ujjivan said they will follow the same approval if Equitas gets the nod from SEBI.

This question was asked in the conference twice, why we are waiting for Equitas to get approval when it takes such a long time. The reply was that since the process takes so long, and they are trying to protect the downside (As per the Nirmal Bang report, there will be tax implications if an SoA is enacted due to the transfer of funds from USFB to UFSL).

If Equitas doesn’t get approval by September 1st week, Ujjivan will go ahead with the IPO. It seems that the management is not as keen to seek an extension from RBI as Equitas is. Perhaps the reason for this is that they want to show excellent corporate governance, compliance to RBI and when they do apply for a reverse merger, they do it with an impeccable record. That’s the feel I got from hearing Samit Ghosh on the call.

On the question of availability of reserves for an SoA, this is what the management had to say, “So even post this our reserves are also there in the operating level as well as we also have other options available to distribute the shares to the shareholders of the Holdco. Both options are available. On the reserve side, we have a healthy reserve at the bank level.”

Fundraising through IPO for about 10% is positive as this will take care of medium-term capital requirements. The good part is that this capital can be raised through existing shareholders as well, which will limit dilution for current shareholders. There is a special price of 10% discount for retail investors (less than 2 lac holding) in the IPO, limited to 10% of the IPO OFS. There will be a possibility for institutional holders to also apply for the IPO.

The Economic Times article has been refuted by the management in a clarification sought by the exchange (refer below).

Ujjivan Financial Services-1QFY20 Result Update-5 August 2019.pdf (555.1 KB)

Ujjivan Q1FY20 Concall Transcript.pdf (329.8 KB)

https://www.bseindia.com/xml-data/corpfiling/AttachLive/07132d25-5033-4295-aba8-bf1ec51d16bc.pdf

2 Likes

Felt very bad after hearing the concall.

There are no free shares to existing shareholders. Even if I have 1 share of Ujjivan, I will be eligible for 10% of ipo Quota at 10% discount.

Though they kept sept 4th as deadline to proceed with ipo, they are in no mood for extension. So IPO is confirmed.

Reverse merger decision will be taken to RBI after Jan 2022. Can we get guarantee for 1:1 merger after 2.5 yr wait. NO.

So why shud we hold the current shares ?

In Equitas concall, the management was quite confident about getting approval from RBI for their SoA & they don’t see any reason that RBI would decline, as they are not diluting any equity but issuing bonus shares out of capital reserves, not favouring promoters and so on.

Not sure why Ujjivan management is apprehensive about this SoA getting approved and they cite this as reason for their alternate IPO plan.

Assuming that they do this under the best interests(?) of existing shareholders with reasons such as stamp duty & Tax charges,etc, and holdco shareholders would anyway be holding 90% of SFB which in turn is expected to be valued around 8500 Cr., any fair assumption on what would be the post listing value of both USFB & USFL?

Disc: holding since IPO

1 Like

As per latest announcement the management has filed drhp for 1200 cr ipo, current book value is around 1900 cr. For this ipo to be a 10-15% dilution the ipo valuation would have to be between 4 - 6 price to book. Guess this is the holding company discount already factored with UFS trading at 1.87 PB.

Here is another way of looking into it, if the 1200 cr ipo forms 15% or 10% of outstanding shareholders capital then the market cap of USFB will be 8000 cr or 12000 cr respectively. UFS shareholders will have a 85% or 90% stake respectively whose value will be 6800 cr or 10800 cr respectively. With a 50%+ holding discount that would mean 3400 cr or 5400 cr or lower market cap for UFS. We are already at 3500 cr market cap. I am guessing 10% is out of question in this market, getting subscription at 6 PB will be difficult.

Another question to ask is what will happen to dividends, will UFS shareholders get them? I am guessing here, that until now since 100% of USFB was owned by UFS they just transferred reserves to the holding company and they paid the dividends. Now if USFB declares dividends for their shareholders then 85% of that will come to the holding company too, but will they be able to distribute them without being taxed again.

PS: A small correction, the dilution will be calculated based on new total equity. The dilution will be x/(1900+x).

PPS: Here are a few numbers I have worked on to the best of my knowledge and understanding. If I am wrong in any calculation, please do correct me.

| IPO Amount | 1200 | |||||||

|---|---|---|---|---|---|---|---|---|

| USFB Book Value | 1877 | |||||||

| PB | Share Issued | % Dilution | New Book Value | Market Cap SFB | UFS % Ownership | UFS Holding Value | 50% Disc. | 60% Disc. |

| 3.5 | 342.86 | 15.45% | 2219.86 | 7769.5 | 84.55% | 6569.5 | 3284.75 | 2627.8 |

| 4 | 300.00 | 13.78% | 2177.00 | 8708 | 86.22% | 7508 | 3754 | 3003.2 |

| 4.5 | 266.67 | 12.44% | 2143.67 | 9646.5 | 87.56% | 8446.5 | 4223.25 | 3378.6 |

| 5 | 240.00 | 11.34% | 2117.00 | 10585 | 88.66% | 9385 | 4692.5 | 3754 |

| 5.5 | 218.18 | 10.41% | 2095.18 | 11523.5 | 89.59% | 10323.5 | 5161.75 | 4129.4 |

| 6 | 200.00 | 9.63% | 2077.00 | 12462 | 90.37% | 11262 | 5631 | 4504.8 |

3 Likes