Yeah, add to this they have also hinted at a 60% listing to old shareholders in an older quint interview. Best we can do is wait and watch.

1 Like

Wonderful clarification from ujjivan.

10% of bank shares can be given to existing shareholders at a special price.

1 Like

It looks more loss for existing shareholders…suppose I am holding 100 shares of ujjivan, it means even if I will get say 10 shares at special price, As a holding company my existing shares will be valued at 50 to 70% discount. That means even if bank share would be listed at 400 per share, my existing share would be valued inbetween 150 to 200 rs.

Am I right? Any expert here who can give calculation?

Holding company discounts are rarely more than 50% and are only applied when holding company is a minority shareholder. It depends on who is in control of the business decisions. After 10% listing of SFB, Ujjivan will still hold 90% in the SFB. Which means all decisions will still be driven by the Ujjivan financials and not SFB. Till the time Ujjivan holds a majority share, it can continue to report consolidated financials the way it is currently doing. So, ideally there should be ZERO discount for the holding company here. But markets are crazy and in panic discount can remain high. In a Bull market, discounts will be next to nothing.

7 Likes

Even if the discount is 50% to SFB valuation, if the Valuation of SFB is 10000 cr suppose, ujjivan will trade at 5000 cr mcap. which is 40% higher than the current mcap of ujjivan.

The possibility of a reverse merge after listing is also confirmed by management.

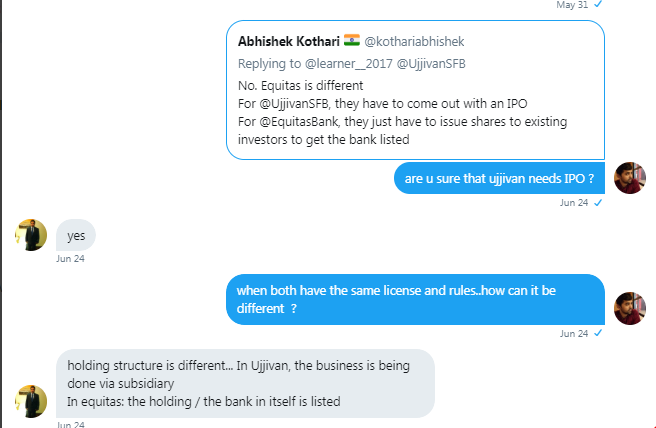

One of the question is if Equitas has decided to go with option 2 (47%) what compels Ujjivan to go with option 1? Equitas is not coming up with IPO.

The holding structure seems to be different. Hence an IPO.

Had a discussion with Abhishek Kothari of CNBC about this tweet.

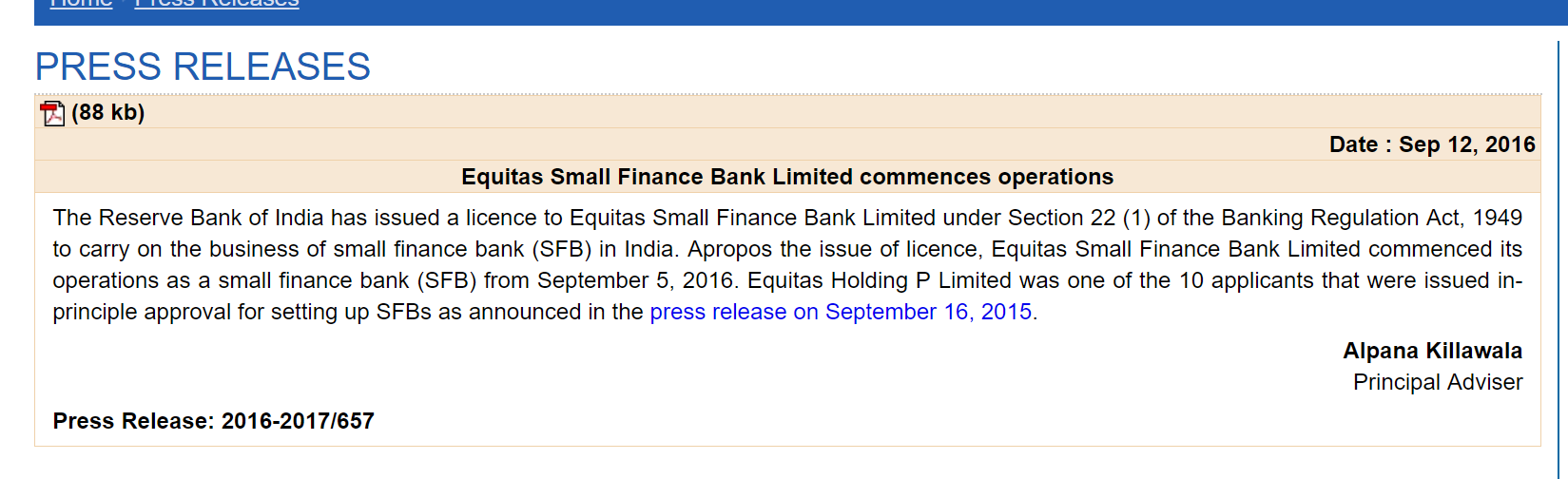

Equitas Holdings Ltd is listed as the holding company whereas Equitas Small Finance Bank Ltd has the banking operations. Similar is the case for Ujjivan. Both have the same structure. Same was bought out by Sumit Ghose in the con call too.

1 Like

The point here is how do we calculate the valuation of SFB? In my personal opinion it’s better to wait and watch and fresh investments to be made only when one has clarity on it, though some upside might be lost in that time but capital protection should be the aim.

Dis: sold all my holding today

I could not understand how Equitas and Ujjivan structure is different. I think you should ask for more clarification/explanation.

In both cases holding companies that is Equitas Holdings and Ujjivan Financial Services hold 100% of Small Finance Bank(SFB). They both essentially have same structure as far as I know.

Looks like Ujjivan SFB management is trying short change the shareholders of Ujjivan Financial Services (FS). As such management of Ujjivan FS is very weak and do not expect them to protect the interest of shareholders of Ujjivan FS.

All the shots are called by Mr. Samit Ghosh who very cleverly shifted to Ujjivan SFB.

I am little surprised although because Ujjivan Financial Services is majority owned by institutional investors. (mutual funds, aif, fpi, banks, insurance companies & PE funds) Together they hold around 57.27% as per March-2019 shareholding pattern released to BSE.

Does IPO of a 100% subsidiary does not require majority shareholder approval?

Thanks for the detailed write-up Abhinav, very helpful as always.

Below is my analysis, more so, on the probable value creation / destruction.

Firstly, let’s not mince the words w.r.t to promoter shareholding guidance of RBI. Here’s what it has to say.

“The promoter’s minimum initial contribution to the paid-up equity capital of such small finance bank shall at least be 40 per cent. If the initial shareholding by promoter in the bank is in excess of 40 per cent, it should be brought down to 40 per cent within a period of five years. The promoter’s minimum contribution of 40 per cent of paid-up equity capital shall be locked in for a period of five years from the date of commencement of business of the bank. Further, the promoter’s stake should be brought down to 30 per cent of the paid-up equity capital of the bank within a period of 10 years, and to 26 per cent within 12 years from the date of commencement of business of the bank”

The promoter, which in this case the current listed entity, has to bring down the ownership stake to 40% by January 31, 2022 and to 26% by January 31, 2029 (assuming it doesn’t get Universal Bank status in the interim period).

Now, let’s assume various scenarios through which the current listed entity can achieve that.

Case 1: Ujjivan Financial decides to list 60% of SFB and gives the entire 60% to current shareholders.

The current book value of Ujjivan is INR1,900Cr. Let’s assume it commands a P/B of 2.5x as SFB. This amounts to INR4,750Cr. Now, the current shareholders who own 60% in SFB directly and 40% through Holdco will get you a market value of

60% * INR4,750Cr + 40% * 60% * INR4,750Cr = INR3,990Cr (assuming 40% Holdco discount)

This is effectively what Equitas is doing, albeit, with a different distribution percentage. This was announced by Equitas in Feb-2019. The reason that it is still trading a 2x book value prompted me to use 2.5x P/B multiple for SFB and 40% Holdco discount as awarded by the market.

Case 2: Ujjivan decides to raise INR500Cr (which is roughly 10% equity dilution) through IPO simultaneously.

Current NOSH of Ujjivan is c.12.2Cr and this additional capital will take it to c.13.3Cr.

Now, the new book value is INR2,400Cr. And, at 2.5x P/B this should trade at INR5,250Cr

You are holding 40% of this through Holdco and 50% directly in SFB. The new 10% is with the fresh investors. This structure will get you a market value of

50% * INR5,250Cr + 40% * 60% * INR5,250Cr = INR3,910Cr (assuming 40% Holdco discount)

Either way, it shouldn’t lead to significant capital erosion if the market remains sensible.

However, my biggest apprehension is if the reverse merger doesn’t go through I will be stuck with Holdco discount for my life. My rationale for investing in Ujjivan was growth coupled with P/B expansion for the risk that I was willing to take in the risky business model of non-secured micro finance lending. Now, if the P/B expansion won’t materialize you’ll end up generating a CAGR of c.16% equivalent to its ROE. A serious let down for me!

Happy to be disputed.

Note: All the numbers are only ballpark estimates.

4 Likes

We know …there are multiple rumours floating around on the listing/no listing/valuation

Given Ujjivan’s Samit Ghosh’ reputation and given significant money of the 1st generation entrepreneurs are involved, I am sure, whatever be done, it will be done keeping interests of minority shareholders’ in mind

RBI rule on SFB is divided in two parts…. First listing of SFB within three years and promoter holding to be brought down to 40% as mentioned by you in five years.

Since three years are getting over for in Jan 2020, they may currently just went ahead with IPO wherein 10% is new investors and say 90% (or max allowed as per listing rules) current hold co shareholders. And then in subsequent two years further scale down in SFB can happen.

Your calculations than would be 90% of 4750 + 10%*60% of 4750 = 4560 cr

Let’s hope shareholders interest is preserved

Correct me if wrong….

-

Did management of Ujjivan FS expressly told investors that SFB has to be compulsorily listed as part of licensing condition?

-

I am pretty sure that management of Ujjivan has already curved out a plan about IPO, listing and shareholding structure. (Who would appoint bankers for IPO without having a plan?) Does shareholders of Ujjivan FS know what is the plan? Opacity in working is neither a symbol of reputed management nor of a great company.

-

The reputed person you are talking about has sold all his shareholding in Ujjivan FS. Also, he is not part of Ujjivan FS in any way, he is MD of Ujjivan SFB.

-

Instead of all kind tricks the so-called reputed management is playing with existing shareholders. They should have ensured exactly mirroring shareholding in SFB and FS to existing shareholders and any future fund raising should ensure same dilution in both Ujjivan FS & SFB.

-

Given what they are doing now, one should remain very careful of the tricks this management will play with public money in future!!

1 Like

I wish not to believe you but promoters action speaks larger than words.

Is there any particular reason promoters (Samit Ghosh etc) sold off their entire holding (any regulatory reason etc)? Also do they have shareholding in Ujjivan SFB or he is just MD with 0 shares?

-

As far as I know Ujjivan FS owns 100% of Ujjivan SFB. If they have created some other interests in SFB that is further negative.

-

I vaguely remember that reputed person you are talking about sold all his shareholding in Ujjivan FS. I may be wrong here. I do not know of any regulatory requirement. But I am pretty sure there is no requirement for a director to hold any shares in the company.

You truly said actions speaks louder than words. Actions of not telling shareholders expressly that Ujjivan FS is a holdco and SFB has to listed on a future date is enough for me gauge the reputation of this management.

In fact I faintly remember reputed person talking quite loudly on TV interviews that Ujjivan FS holds 100% SFB and is as good as bank for all purposes. I can dig that up on youtube.

Infact I recently looked up the RHP on page 136, item numbe-12 it is mentioned that - “The shares of the SFB shall mandatorily be listed within a period of three years from the date of commencement of business of the SFB.”

Please find RHP here. (I have saved copy in case link is removed)

And company had in-principal approval of RBI for SFB at the time of IPO.

Therefore, it can be concluded that management knew they are coming up with an IPO of a holdco from day one, but never cared to highlight this to retail investor.

Disclaimer - I am a long-term investor in Ujjivan FS obvious feeling cheated therefore views may be biased.

1 Like

Think some of the angst in this thread is unnecessary. If you were following the SFB story at all, the rules around it and the holding company structure adopted by many of the NBFCs and MFIs who applied was well known. Allegations of misleading retail investors is uncalled for.

I assume management has run into a challenge with RBI taking a particular interpretation of their guidelines that rules out a merger - here is my reading of the source of the conflict:

-

SFB is required to be floated by a promoter entity. Ujjivan fulfilled this by converting its existing NBFC into a hold co, which became the SFBs promoter - the SFB itself was set up as a new entity and the assets of the erstwhile NBFC was transferred to it in a slump sale.

-

SFB regulations require the promoter to be locked in for 5 years from the date of commencement of business of the SFB. Ujjivan got its final license in Nov 16. This would mean its 5 year promoter lock in expires Oct 2021. By the time the promoter lock in expires, the promoter should have bought its shareholding in the SFB down to 40%.

-

SFB regulations also require that where the SFB’s networth exceeds Rs. 500 cr, the SFB must be listed within 3 years. Assuming this is 3 years from the date of final license, this would be Nov 19 - press reports state that Ujjivan’s deadline is Jan 2020.

Given the two above requirements, RBI may very well have taken the view that a merger is not permitted as it would violate the promoter shareholding lock in by eliminating the promoter all together. At the same time, the SFB must be listed. Ideally, they would have liked to list post the expiry of the lock in, wherein they could simply have merged the SFB and the hold co to comply with the regulations (regulations do not require the promoter to be locked in at any specific threshold post 5 years). I think the simplest thing for them would be to make a small issuance of 10% to existing shareholders, wait till the lock in expires, and then merge the SFB and the hold co. Ideally, existing shareholders should be issued warrants at a preferential price in the SFB to hedge against declines in the hold co share price - I assume this is what management means when they say that 10% of the SFB’s shareholding will go to existing retail investors at a special price. Eventually, once the promoter lock ins periods are over, the hold co can be merged into the bank, so value will be rationalised as the SFB can always effect this by issuing a 1:1 stock swap. Given the presence of institutional investors who would push for value retention, this is the likely path.

Disc: invested

7 Likes

The rules of 3 yr listing and 5 yr holding are marked from date of start of bank operations. Ie., Jan 2017. Hence listing deadline becomes Jan 2020 and holding deadline becomes Jan 2022.

1 Like

Thanks for the correction, Gautham.

How many shares of SFB do we get if 10% of the SFB is straightly distributed to us ? Book value being 1900 cr and expecting 3 times book valuation. ? So 6000 cr valuation for SFB, 600 cr distributed among 3500 cr Current ujjivan size ? 1:6 ??