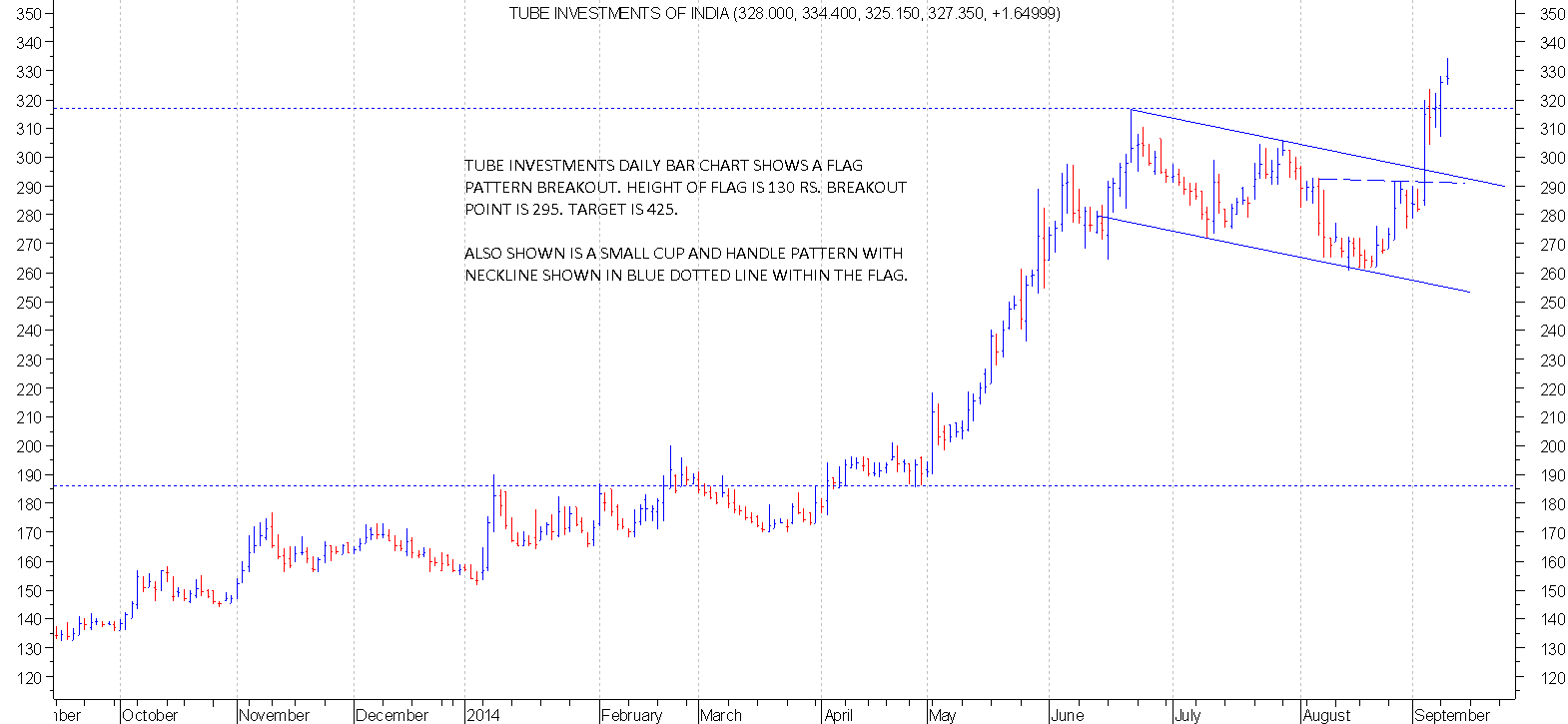

Stock is at all time high and so has little by way of resistance.

Fundamentally it belongs to the well respected Muruguppa group and is a conglomerate of various companies. Main business remains auto ancillary. Other subsidiaries include investments in insurance and NBFC arms.

Tube Investments consolidated results are as follows

period

q2 fy 15

q2 fy 14

H1 FY 15

H1 FY 14

FY 14 (12M)

total income

2483

2221

4860

4324

8834

op profit

271

224

512

448

885

PBT

200

238

451

398

789

NP

100

85

190

166

311

eps

5.35

4.55

10.1

8.8

16.7

One has to look at the consolidated results shown above to get a better idea about the company.

Overall results look quite encouraging.

Full Year EPS could be close to 20 per share. Based on that, at current prices stock is quoting at 17-18 PE. Another way to value this company could be sum of the parts valuation method where one has to value the standalone entity and add discounted valuations of holding in subsidiaries.

Moneycontrol shows the Industry P/E for Tube Investments as 68.51

Also the P/E for Tube Investments is shown as 67.07 with EPS as 5.17

Could you explain how they arrived at that P/E for Tube as well as the industry? And are there any other sources where we can get the all the Industry P/Es?

OPM and NPM improved in this qr. compared to June Qr.

Review of Business

Bicycles

Continued to maintain growth compared to corresponding quarter

in the previous years

period

q2 fy 15

q2 fy 14

Growth %

Revenue

342

325

5

PBIT

15

14

7%

Engineering

As per management Positive growth in 2 wheeler and passenger

cars enabled Engineering and Metal forming business to maintain their growth. The

company inaugurated large diameter tube plant in Tiruttani in oct 14 which will

further propel the growth in infra segment.

You should know first hand that anyone on the forum has no compulsion to answer anyone else. This is a forum for learning and sharing.

If u have bought zensar and tube investments you should have had an investment thesis and rather desperately wanting an answer from me you should have your own views on the company.

You can put up the details of the Chola stake sale on the thread and then we will take it forward if u so wish.

Tube Investments of India Ltd has informed BSE that the Board of Directors of the Company at its meeting held on December 25, 2015, has approved the divestment of 4,18,32,798 equity shares of the face value of Rs.10/- each held by the Company in its general insurance subsidiary viz., Cholamandalam MS General Insurance Company Limited (“Chola MS”), constituting 14% of the equity share capital of Chola MS, to its joint venture partner viz., Mitsui Sumitomo Insurance Company Limited, Japan (“MSI”) for a consideration of Rs.211/- per equity share, aggregating Rs.882.67 Crores.

Post-closing of the Transaction, the shareholding of MSI in Chola MS will increase from the existing 26% to 40% and the Company’s shareholding will be at about 60% (existing: ~74%).

Anybody tracking this Company?? Views invited…

Disc- Holding since past 2 years and forms approx 15% of the portfolio.

I was just analyzing this stock and flourished by its growth since last one year. It had also doubled its stock value in 2 years.

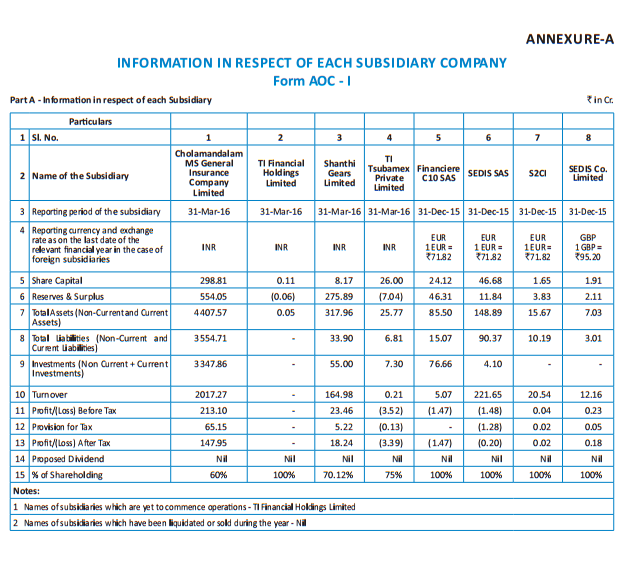

Below is the list of its subsidiary with relevant information:

Here is a short note on tube investment demerge details taken from 267 paged document on http://t.in.com/Daty NCLT approval received record date -28 AUg. Shares holders to receive one share of TIFHL each for every share in tube investments.

Revenue split TI-manufaCTUring -82% TI-Financial services-18% TI FHL Revenue details- 2015-300 CR 2016-361 CR 2017-420 CR Share capital 37.47 cr Reserve and surplus 1902 cr Post demerger Share capital for each will be 18.6 cr approx. Reserves and surplus for TIFHL will rise from -0.06 cr to 967 CR Assets on books-953 CR each for TIFHL and TI Ltd AN old note for referece- Chennai, April 30: Tube Investments of India Ltd, part of the Chennai-based Murugappa Group, has posted a consolidated net profit of Rs 77 crore for the quarter ended March 31. This represents 93 per cent growth over Rs 40 crore in the year-ago period. The consolidated turnover for the quarter stands at Rs 1,809 crore (Rs 1,460 crore). As a standalone company, it has posted a net profit of Rs 58 crore on a turnover of Rs 871 crore during the quarter as against Rs 46 crore on Rs 782 crore in the previous-year quarter. Cholamandalam Investment & Finance Co Ltd, a financial services subsidiary, posted a net profit of Rs 61 crore during the quarter (Rs 36 crore). Cholamandalam MS General Insurance Company Ltd, an insurance subsidiary, posted net profit of Rs 5 crore in the quarter (a loss of Rs 34 crore). Financiere C 10, the company`s overseas subsidiary that makes industrial chains, achieved a turnover of Rs 216 crore and net profit of Rs 5 crore. In the past financial year, Tube Investments posted a consolidated turnover of Rs 6,265 crore (Rs 4,917 crore). Net profit stands at Rs 269 crore (Rs 196 crore). According to Mr L. Ramkumar, Mag Director of Tube Investments, the bicycles division registered a growth of 8 per cent in volume and 15 per cent in revenue during the year. The slow down in auto industry impacted the turnover of engineering and metal formed product segments. Besides, thanks to inflation, the margins too were under pressure.

Tube’s cycle business is stagnant (rather degrowing), but all other verticals are firing very well, which is evident from the capacity utilization of different verticals. Cycle manufacturing, as an industry, has stagnated in last 2 years. Performance cycling is doing well but other cycle verticals are not gtrowing.

On the other hand, the demerged business (finance segment) has been growing very well on back on good growth in insurance segment along with lending division. Though, this demerged entity being a holding company, how are the prospects for this going forward? Will this always trade at discount to the actual businesses (Chola, etc)? How would the holding company hold its shareholding, once the capital is raised in the NBFC?