One has to be suspicious when firms in low profitability business claim high growth and profitability. Usually, either the growth or profitability or both are overstated.

At least SEBI noticed.

My two cents. Obviously all of this is in hindsight but the lesson is to try & invest in companies which have some skin in the game. The Treehouse business model is primarily based on self run pre-schools. Treehouse only provides the guidance & its brand to these preschools. They have very less skin in the game. If the pre-school does well its a win win for both the preschool owner & THEAL but if the preschool doesnt the major loss is that of the preschool owner & not THEAL. No skin in the game.

1 Like

Of its total operations, THEAL had ~ 80% preschools which were ‘Self Operated’ where the company itself did most of the heavy lifting, while the rest were ‘Franchise’ where they provided guidance and brand rights to the owner.

you are right. After you mentioned it i looked it up. There are a couple of

treehouse outlets near my home in pune & all of them are franchises so i

presumed that was the business model. When i was looking for a preschool

for my daughter i visited a few of them & was not very happy. While

preschooling is a business, the owner of one near my home tried to sell my

wife a franchise too and we were really put off by that. Since then,

barring one, most of them are closed now.

1 Like

Results out.

Company has shown losses and severe decline in sales. What more could be expected from such a Fraud promoters.

Mentions nothing about the propsed Merger and also reasons given for low performance do not seems to be satisfactory and looks stupid.

Advisory asks Tree House shareholders to vote against financial statements

1 Like

Can anyone give an update on the merger or issues with the management. There was story on ET regarding issues between promoters and management.

Mumbai: Treehouse nursery shuts 113 branches across country after facing fund crunch

The story was long over. I have said before all investment banks need to be held responsible for its IPO. There were questionable insider trading all along. The promoters happily offloaded real estate to the listed entity.

They have appointed a 23 year old kid who cant write proper english as independent director. The kid most likely applied for the post of an intern…

1 Like

1 Like

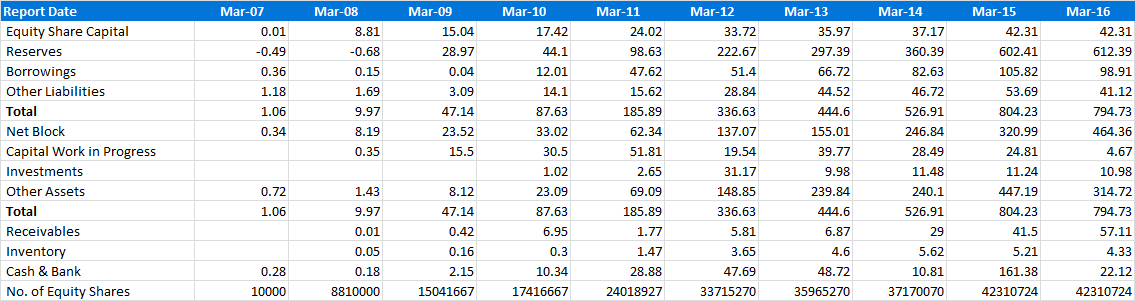

Equity dilution often predicts trouble ahead. Treehouse is another example of the many companies who have trodden this minefield. No of shares went up from 88L in 2008 to 4.23cr in 2016. In my opinion this is a red flag that should rank right at the top.

3 Likes

Sharing a presentation I and shan did during one of Bangalore group meeting regarding dissecting financial statement and corporate governance. Case in point was treehouse. Could we have gone few years back, did our ground work and find if this would be a good or bad investment (focus was reading through annual reports to understand practices of governance and financial honesty). hope it will benefit all.Dissecting Annual Reports and Governancev1.pdf (1.8 MB)

abc limited.xlsx (190.4 KB)

11 Likes

This is very interesting!

To be honest, their balance sheet and accounts looked okay unless looked in depth. I mean, they were diluting equity consistently but their debt was very much under control, consistent topline and bottomline growth, their CFO for 2015, 2016 was very decent (was a problem in 2013, 2014), management was considered to be very honest and forthcoming, presence of many reputed investors, okayish receivables (increased from 2016), regular dividends. Most of their ratios were pretty decent. There sheer visibility in every city was a big soother and brought conviction about the investment.

Main reasons for failure - Consistently high working capital requirements (working capital/sales), extremely high capex (too much expansion), consistent negative FCF, low ROA, low ROE, pledging, paying dividends despite being a negative cash flow business.

Education sector is considered to be a cash intensive, so one could have assumed them to be in expansion mode (reasons for huge capex). One usually sees CFO but ignores FCF in growing companies. This was the case with Treehouse. This was a very carefully dressed Balance sheet where debt was kept under check and dividends were given.

Case in point - Just thinking about what should one look at while investing to bypass such companies? This was actually a high conviction bet for many. If one looks at FCF when the company is growing, even Force Motors doesn’t quality as investment (abysmal EPA), but is a good business.

I felt there were enough loop holes if one goes through annual report along with very poor corporate governance and accounting practices . Have highlighted some of them in deck above

this is now a cigar butt …just crazy promoter tooo