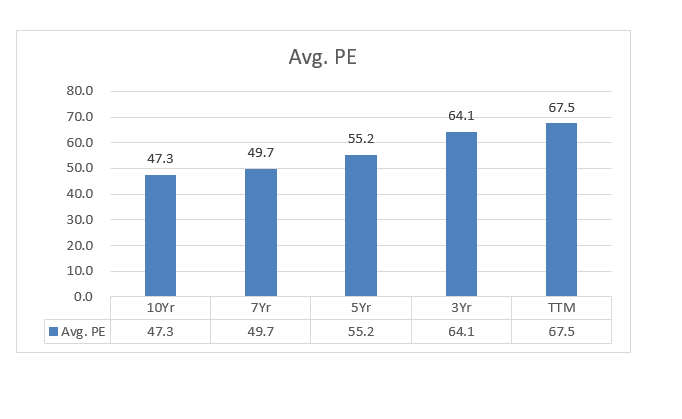

Up untill 2017, this company traded in the range of 35 to 50 PE. Last three years, 2017,18,19 have shown a high growth in the sales figure: 18%,22% and 23% respectively. This is the reason why the stock is currently trading at an unreasonable PE of 70.

Currently, the TTM figure of growth in sales is a diminutive 4% in comparison. The recent quaterly update from the management cited the dullness in the economy. This scorching pace of growth has slowed down. This is likely to continue, because the gloom is not likely to go away anytime soon.

I think Titan reaching a PE of 45 to 50 could happen in the coming months, giving us a reasonable opportunity to buy.

Hi Amit although you are partially correct by citing the PE re rating reasons of sales growth. But this re rating actually has happened on the expectation of gaining market share from the unorganized players since GST will going to play a big positive for the Organized players in the long run. Also their penetration in apparel like Taneira in 2017 also played a big role in this PE re rating since since this market is hugh and dominated by unorganized players all the way through. Slow down in revenue is a concern but the entire Economy is in a stalled situation so we can not expect much growth at this point of time but I think market tend to give PE on long term prospect not on cyclical events.

Please feel free to correct me if I am wrong at any point.

No correction Sir. I am only glad that there is a discussion going on.

The gold and diamond jewelry market is seeing a sharp recession of demand, for corporate and unorganized alike. Leveraged players are finding it tough to survive. The coming quarters will sort out these weak hands.

Reading the updates from PCJewellers, Kalyan, TBZ kind of give the feel for the demand scenario.

Now the real question is, whether Titan will survive the onslaught. And my answer is a resounding yes. Other might not survive, but Titan, Tanishq, will emerge although not without a few scars.

Titan has started taking on debt. The interest coverage ratio is more than comfortable as of now, but the debt shows that the money is now flowing in ever so slowly. Hence, any plans for expansion will have to take a back seat. Therefore, the growth, which the buyers over 40PE have paid for will start feeling the pangs anytime soon.

Non performance of stock price for the next few quarters is very likely. This will lead to fund managers discarding this stock as they have to go where there is price appreciation for their annual appraisals.

In short, growth has now stopped hence it won’t find buyers at 70PE. In fact, as the quarterlies are released there will be more selling, as Titan at 67PE is richly priced.

What I have found out abpout historical PE of Titan is this…

Source :- Screener Data

So I don’t think the PE will go down to 40 unless there are some serious downturn in the economy but even if it will go down to 50 and we consider 25% growth in bottom line then also we will get a EPS around 20, which make the fair price at 1000.

So we need to see what % of growth Titan can maintain for rest of FY20. In case it will be around 25% then current price level is acceptable otherwise there will be downturn.

EPS growth is just one factor impacting PE. The other more important factors are industry structure and position of company, sustainability, predictability and volatility of earnings, Long term market potential and probability of disruption, quality of management, corporate governance, track record.

Some of the increased PE in recent times is due to GST which has accelerated to shift to organized players. Now within organized players, competition has reduced as likes of Gitanjali have gone down and leading to trust for smaller players having reduced significantly. A lot of Gitanjali buyers are holding glass picese which they bought at diamond prices.

Sometimes it pays to have ones ear to ground and some sense of retail economics. Considering the latest numbers, will not be surprised to see a sharp decline in this counter … Ask any millenial, they would rather buy a gadget than spend on gold… It’s time we stopped eugolising the love for gold and recognise that sale of one the most unproductive asset classes cannot sustain for long …489bcd59-a77f-4876-870c-cc95dcdec138.pdf (1.2 MB)

A structurally weak play on consumer sentiment driven high ticket luxury purchase cannot sustain the impact of a cyclical downturn.

While H1 seems to be a washout, Q3 also appears bleak.

In the light of falling sales, Tanishq shall be forced to sacrifice their rich making charges and other discount offerings directly affecting margins. Today, Tanishq is facing the double whammy of increase in employee cost (approx 18%) and rent escalations (3-5%) arising from existing and new store additions besides higher carrying cost of jewellery against stagnant sales. A 25% discount on making charges currently on offer at Tanishq would directly result in commensurate reduction in EBITDA resulting in single digit margins (perhaps at 8-9%) since Tanishq does not earn much on grammage or prices increase (infact they would lose money in case of fall in prices owing to inventory hedges) as was indicated by them in their latest exchange submission.

Not sure if the P/B above 10 and PE above 70 is warranted considering the evolving market scenario. While Indians will continue to buy gold for marriages (incidentally this does not constitute more than 50% of total annual gold buying), the fall in demand during the non-festive season can impair the business model unless they are able to meaningfully grow their non-jewellery verticles in a sustainable and consistently profitable manner.

Personally expect sharp correction by minimum 20% post earnings release and dismal Diwali season.

in long term trend , gold demand will go down year by year . millenial are not intersted in gold jewellery. they buy junk immitation as its cheaper and they can buy plenty of items in small budget and wear .

ask any retail jewellery shop and they will say sales going down every year and especially when their is sudden rise in gold price.

Sir, in my opinion Titan should not be alone consider as gold jewellery Co, it has other discretionary (or life style products ) items and very recent addition in portfolio - Sarees. There are couple of points we should keep in mind, firstly if keep we apart PE or PBV ratios, jewellery or saree are largely unorganized sectors where Titan with organized set-up will draw traction and above all there will be brand pull-effect, we will agree Titan eyegear gives much consumer delight in terms of value and price (aspirational side). So, scalebility of revenue will be high with time if someone really wants hold long say 5~7~10 years.

Secondly, this Co, had worked very well on the consumer taste, trends and style i.e. on behavioral aspects, with change of time it has evolve itself from watch making Co to Lifestyle Co. as we all know how HMT has fared over the same time and fate.

And I strongly believe good Co thrives well if it has evolve itself with consumer change behaviors and patterns and able to positioned well.

And India largely consumption based economy, with 2nd most populous country demand will be there but important thing is price/affordability and attractiveness(gold/diamond to platinum) and positioning ( brick-motor to online, stores to mall/hypermalls).

Titan’s wedding jewellery is around 30% of its jewellery sales (so not the major driver for Titan, though they want to increase the contribution over time). Secondly, I do not believe that millennial spending trends are overrated. If a bride wishes to have a more practical gift such as a Louis Vuitton bag instead of jewellery, why not? The trend in 10 years from now can be very different from what we are seeing today.

I feel Titan has understood this and is evolving into a complete consumer discretionary company. WIth Taneira, Skinn etc it is looking to capture the complete wallet share rather than focus on just jewellery. And remember, it started off as a watch company (todays revenue contribution of c.20%)

Shringar Ras never goes out of favour. It is an eternal human desire to look good. An bag or Iphone cant substitute it. It is for Titan to continuously evolve as per changing preferences. I already see that Tanishq’s partner ‘Caratlane’ stores are attracting younger customer who are looking for office wear jewellery.

Even if not gold, it can be Platinum, Diamond, Iridium or even Silver. And Titan Company has the full brand power to leverage on jewelries made by any of those. Temptation for luxury fashion and smartphones might be increasing but my hunch is that those are not happening at the expense of the passion for jewelries because the overall spending power is also increasing, which can accommodate all of these.

Agreed. And even if jewelry might go out of trend ( which is not possible IMHO ) , then they have huge lifestyle range at their disposal. Their nimbleness would be the key to watch and they are quickly adjusting to new trends till now which one can gauge from the way they moved away from watches to jewelry and also into sarees, eyewear ,perfumes ( although these are early days ) but the execution capability till date is good . Lifestyle as a sector and consumer aspirations sector would always have endless possibilities. Valuations is a different matter altogether however the business has a great going till date . One more thing to watch out for would be the price of gold although theres a view that high gold price affects demand only temporarily and then might catch up . But still its a thing to keep an eye on

Titan and Tanishq are more fashion jewellery brands than gold to me. If i want to buy a junk, i would still prefer Tanishq junk which may have a slightly better materials at some premium. Swarovski is new age and if i have to buy crystals, i might still buy a Tanishq/Titan at a small discount…point is Titan may be more than gold although it’s strength is gold at present.

Secondly, i see some synergy in Titan and Trent when it comes to non gold businesses of Titan. For example Trent came up with a new brand of stores for women which opened its maiden store in pune and Ahmedabad if i am not wrong. It is ethnic wear focussed. I would have loved to have it selling sarees as well rather than a Titan.