The Time Technoplast management commentary was extremely positive. The management is very confident about their products and their sales and profits including their margins are to grow at a rapid pace in the next 2 years as new capacity comes on stream and they get into Tyoe4 composite CNG cylinders for cars and they will slsonbe getting into Hydrogen cylinders also. The potential is huge. In the case of their Comosite LPG gas cylinders the company said that the annual replacement demand from the OMCs for the old steel gas cylinders is 10 times the combined installed capacity of both Time Technoplast and Supre Industries put together. So demand for their products is really huge, they just need to keep expanding and make ore and more profits

Summary of Concall Q3 FY 24:

*Growth Guidance *

~15-17% growth for the next 3 years (Composite 30%, Established 10-12%.)

*Composite Guidance *

~500 Cr current year, 800 Cr next year & 1500 cr 2 year down the line.

~ CNG cascade capacity to expand from 480 to 1080 nos by next year, can give 850 cr revenue after expansion

*Valu added *

~Right now-26%

~Will increase 3-4% per year.

~Can become 36% in 3 year down the line ( Ebitda margin can go to 16% by then)

*ROCE *

~Nine Month ROCE is 15.6% against 13.6% in FY 23.

~ To improve by 2% every year.

~ Can become 20% three year down the line.

*Capex *

~ Nine month Capex 144Cr (63 Maintenance, 81 Composite & IBC)

~Full year Capex to be 175 Cr ( Reduced from 200 Cr)

*Restructuring *

~ Approved- 50% disinvestment of Middle Asea for 25 million $ ( 200 Crore), to be completed in 90 days.

~ Middle Asea contributes 7.5 % (Around 350 Cr) of total consolidated revenue.

~ As 2023 numbers are better than 2022, they may do re-exercise by taking 2023 numbers for balance disinvestment of USA, South Asea.

~No desperation for selling, will sell only when they get good value.

*Non Core Asset *

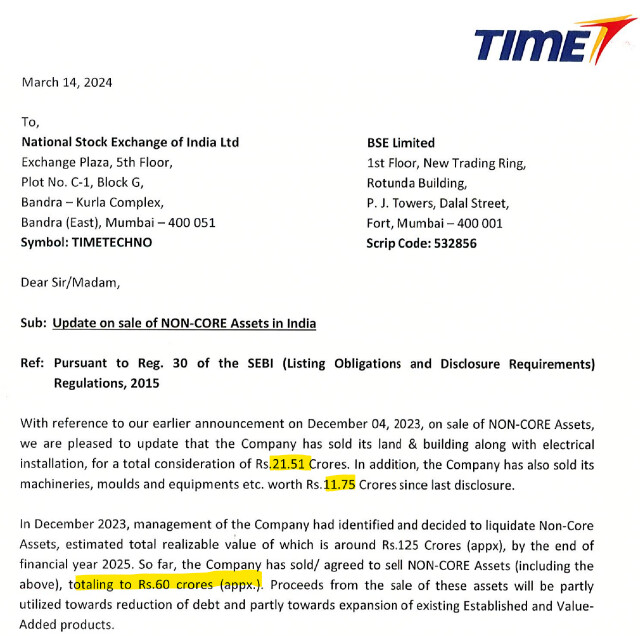

~ 125 Cr NCA to become Zero by March’25.

~Sell of 26.5 Cr land & building in South region to be completed in 90 days.

~ Proceed to be used for Debt reduction.

*Debt *

~ Target to become Debt free in next 3 year

~ By March’25 debt to be reduced to 450 cr from current 800, interest cost can go down to 60-70 from current 100.

*Entry into Automobile *

~No capacity right now, may consider it after next year’s capacity expansion

*Working Capital *

~Targeting to reach 90 days in 6 months, against 112 days last year.

*Disc *- Invested & Biased

Does anyone know company’s order-dispatch cycle?

In Q3 FY24 presentation, it has been mentioned company has an order book of ~400 Crs which at current run rate is less than one month of orders.

How does one evaluate if pending order book is good enough?

I don’t know if I am interpreting this correctly but…

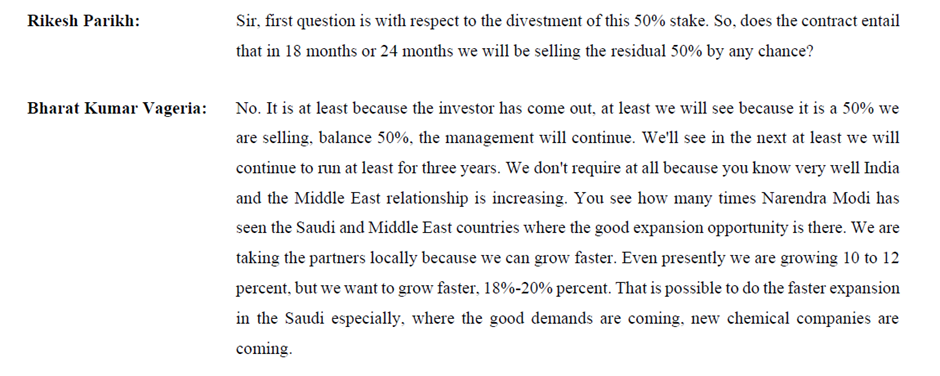

Besides selling only 50 % instead of the earlier announced 80, and retaining management control Mr. Vageria now says this situation will remain for 3 years at least and then “We’ll see…”. The buyer is referred to as “investor” meaning one having only financial interest and not strategic. Mr. Vageria dwells at length on increasing potential in the region. Even with other overseas territories, Mr. Vageria has said (elsewhere) he is 'not desperate to sell’. Overall, the language seems to indicate they will go slow on the overseas divestment plans, do it selectively while retaining management control and consolidating the numbers into TTL. If I remember correctly, earlier the stated intent was to sell 80 % and focus on “core business in India”, implying forget overseas. That may no longer be the case now.

Any views?

Overall the management is not consistent. I have seen previously they used to over promise and under deliver. In my thesis, I keep that in mind. Invested from 75 levels. I think they have a good product opportunity but are not encashing it fullly.

The recent management to me seem to have good intention for shareholder value creation and not like Anil Jain where they achieved every target in terms of number of what they said and as far as sale for foreign business is concerned they were able to sell in line with what bharat ji told i.e., geography wise and from my recent channel check i was able to identify that big growth opportunities in terms of industrial packing is available in middle east and also big development is happening there esp. in Saudi so if they retain 50% stake in it is a good point.

but recently confidence petroleum also announced that they would be undertaking capacity installation for type 4 CNG cylinders and they have a plan to add 500 CNG stations by 2025 so how we should see this in terms of value creation?

who has better probability of it because both have similar margins in range of 14-15% while time techno has LPG cylinder capacity of 1.4 million and 1080 cascade CNG will be onboard from this year end

can anyone help me with it?

I have zero confidence in confidence petroleum it is another management that promised big but under-deliver. I agree that the current management of time techno is better focused on execution than the previous. At least there is effort to reduce debt

Time Technoplast Q3FY24 Earnings Conference Call - 13th Feb 2024

Financial Performance

-

Time Technoplast reported a 20% YoY volume growth and 17% revenue growth in Q3 FY’24.

-

The value-added products segment grew by 25% YoY, while the established product grew by 15%.

-

EBITDA and PAT margins grew by 26% and 50% YoY respectively.

-

The company achieved a turnover of 3,601 crores in the first nine months of FY’24, a 16% increase compared to the previous year.

-

Profit after tax for the nine months stood at 218 crores, surpassing the entire previous year’s profit of 219 crores.

-

Return on capital employed (ROC) increased by 2% to 15.6% in the nine months compared to 13.5% in the previous year.

Strategic Developments

-

The company revised its CAPEX target for the full year to 175 crores from the original target of 200 crores.

-

The board has approved the disinvestment of the 50% business in the Middle East for an evaluation of around USD25 million.

-

The company has identified non-core assets worth Rs.125 crores and plans to complete the first transaction of Rs.26.5 crores for the sale of land and building within 90 days.

-

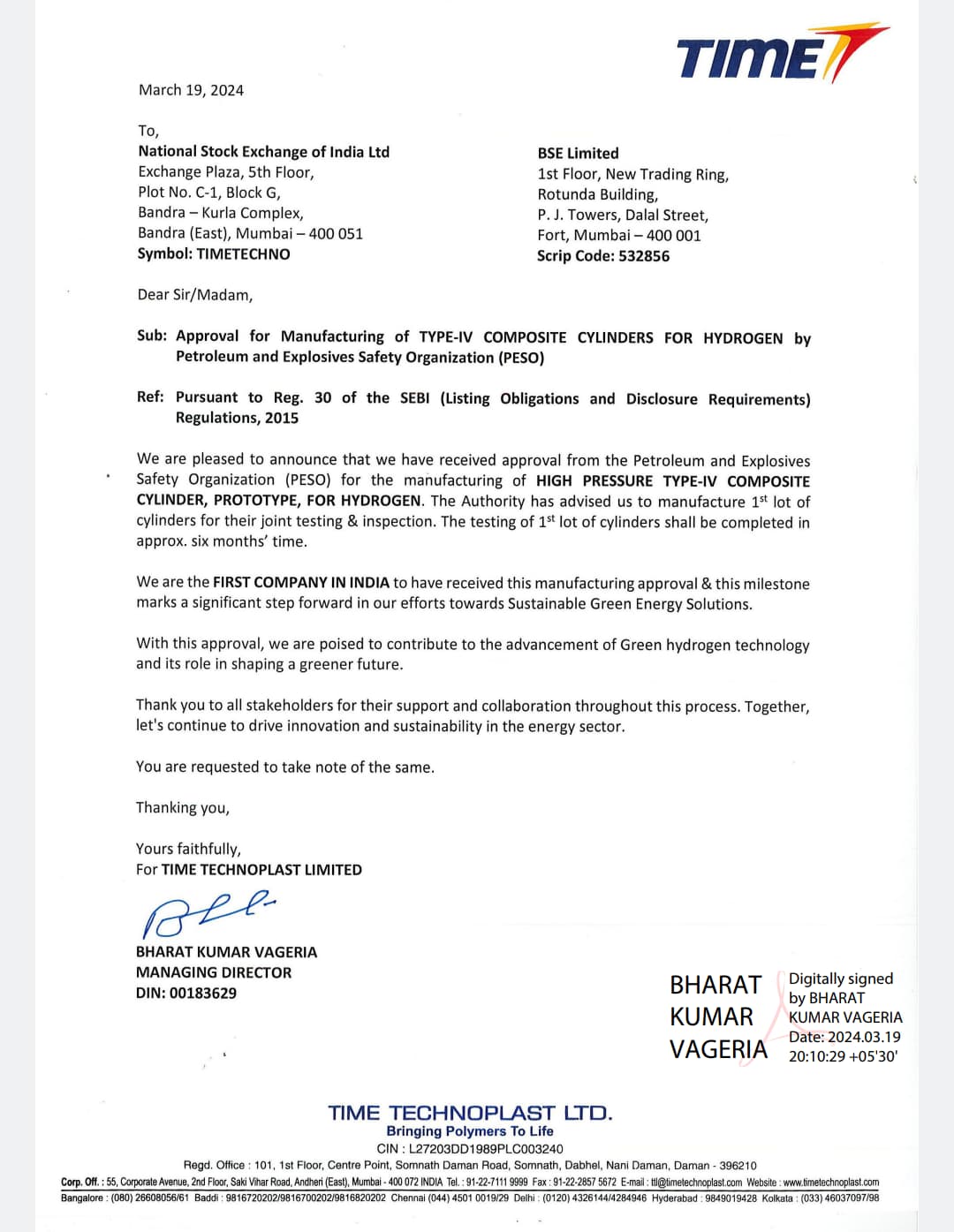

The company is developing products towards green energy, including composite hydrogen cylinders and other composite products for use in the automotive industry.

-

The company is participating in new tenders for LPG orders and expects to secure business for the next year.

-

CNG composite capacity is being expanded from 480 to 1,080, with revenue expected to increase from Rs. 350 crores to Rs. 850 crores next year.

-

The company has started the process of registering with the army and navy authorities for oxygen cylinder supply.

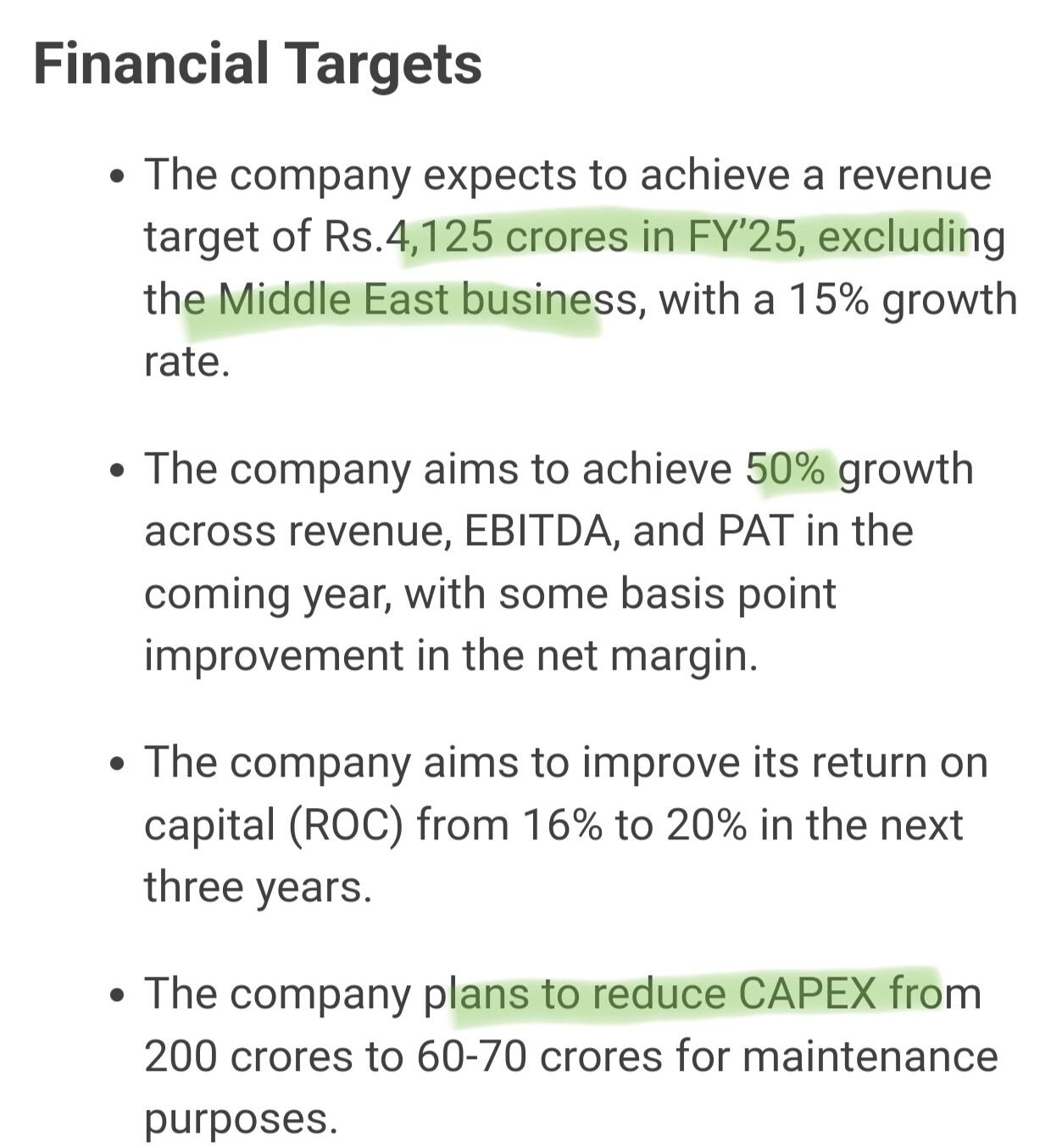

Financial Targets

-

The company expects to achieve a revenue target of Rs.4,125 crores in FY’25, excluding the Middle East business, with a 15% growth rate.

-

The company aims to achieve 50% growth across revenue, EBITDA, and PAT in the coming year, with some basis point improvement in the net margin.

-

The company aims to improve its return on capital (ROC) from 16% to 20% in the next three years.

-

The company plans to reduce CAPEX from 200 crores to 60-70 crores for maintenance purposes.

-

The company expects a 15% CAGR in topline growth, with 30% CAGR in composite products and 10%-12% growth in established products.

-

The share of value-added products is expected to increase from 27% to 36% in the next 2-3 years.

-

The company is targeting an EBITDA margin of 14%-16% in the next three years.

Debt Reduction and Disinvestment

-

The company plans to use the proceeds from the disinvestment and the realization of non-core assets to reduce its debt by March 2025, targeting a reduction from Rs. 800 crores to around Rs. 450 crores.

-

Time Technoplast does not have any immediate plans to sell the remaining 50% stake in the divested business and intends to continue running it for at least three years.

Market Expansion and Diversification

-

The company aims to grow its revenue faster, targeting an 18%-20% growth rate, particularly in Saudi Arabia.

-

Time Technoplast has received approval for its oxygen cylinder for CNG in the automotive industry but is yet to capture a significant market share due to capacity limitations.

-

The company is exploring the possibility of expanding into the Southeast Asian market.

Please correct me if i am wrong @aashu4uiit

-

FY 24 Total Revenue can be 5000 Cr

FY 24 Middle East can be -350 Cr

FY 24 Revenue excluding Middle East can be=

5000-350= 4650 Cr

FY 25 Revenue excluding Middle East can be= 4650*1.15= 5347 Cr -

The company aims to achieve 15% growth

-

Maintanence capex has been already reduced from 200 Cr to 60-70

Middle East culture require local partnership to grow substantially for Govt contracts . This is how Middle East work !

No . That’s not true. You can have 100% ownership and control of your business in UAE.

Here I have attached Time Technoplast Research Report which I made and I hope you guys derive some value from it.

Time Technoplast Limited Report.pdf (1.1 MB)

Time Techno seems to have hit a purple patch in terms of delivery (17% sales growth, 49% EPS growth) and investor confidence. Its hard to believe that the co was available at 3x PE during COVID fall! Management now seems very confident of exceeding 15% growth in the medium term. Concall notes below.

FY24Q3

-

Targeting 15%+ sales growth in next 2-3 years (10-12% packaging + 30% composite)

-

Established product growth of 15% was driven by polyethylene pipe businesses (expect 25% growth in pipe business in next 2-years)

-

9M debt reduced by 65 cr. and will reduction will exeed 100 cr. in FY24. Without any further divestment, debt will reduce to 450 cr. and interest cost will reduce to 50-60 cr.

-

Capex : 45 cr. (23 cr. towards established products + 21 cr. towards value-added products). Reduces FY24 capex to 175 cr. (vs earlier planned 200 cr.)

-

Middle east disinvestment : 50% business for $25 mn (13-14% EBITDA margin, ~350 cr. FY24 revenues; include Dubai, Bahrain and Saudi; excludes Egypt plant; out of 1.4mn IBC capacity in Middle East, divesting 0.1mn IBC capacity). Net of taxes, will get ~175 cr.

-

Target divestment of 125 cr. of non-core assets (earlier 100 cr.) and no non-core assets by FY25. First transaction of 26.5 cr. will be used for debt reduction

-

In IBC manufacturing, leader in 7 out of 10 countries. Are not leaders in US. Total capacity: 1.4mn abroad (60% utilization) + 0.5mn India (75% utilization). 60% IBC sales comes from overseas and 40% from Indi a

-

In CNG cylinders, will target auto segment after next capex cycle in FY25

-

CNG composites : capex of 125 cr. (capacity increase from 480 to 1,080) can generate revenue of 800-850 cr.

-

Targeting 1500 cr. revenues from composite in next 3-years (vs 500 cr. in FY24)

-

Oxygen cylinders: started registering process with army and navy authorities. Fungible capacity with LPG

-

LPG Type-IV cylinders: Only Supreme and Time techno are making this (combined capacity of 2mn)

Disclosure: Invested (position size here, no transactions in last-30 days)

Looks like FIIs are constantly reducing stake in Time technoplast , however DIIs are increasing their stake

Recent gas pipeline scheme for each home will dent company business?