You are conceptually correct. Targets though are always subjective and besides the main utility of these formations is to help you to develop the conviction to hold the business if you are invested in them fundamentally ( which i am )

strong upside moves in TGL for the past few days taking out some tops. The 200d should act as a strong barrier so would be waiting keenly for that to be taken out. That would firmly put to rest any doubts as to the trend in the medium term.

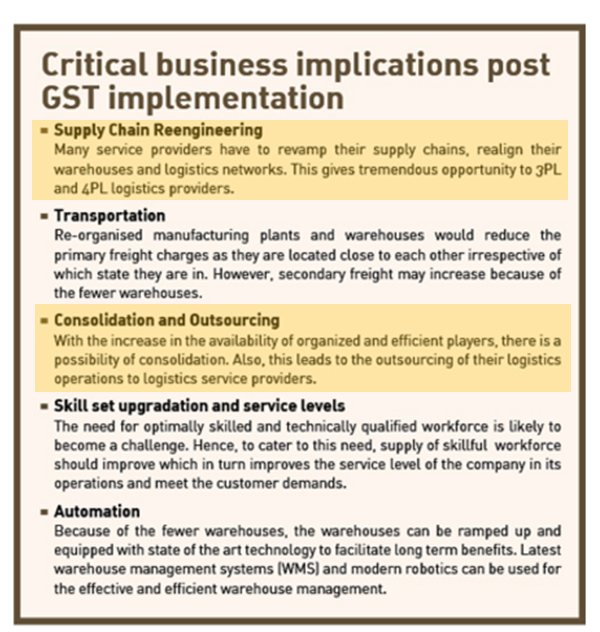

Consolidation in the logistics industry post GST is expected to favourably impact 3PL players.

TGL has formed a nice channel at the bottom signifying a structure to the prices. Fully expect TGL to move within this structure till it tests the 200d.

Those interested can read the DHRP if and when available…to know how tough this business is…with an avg pat margin of less than 2% over last 3-yrs (in case of M&M)…there is little margin for error.

So, it would be interesting to see how this high growth, high RoE biz gets valued which also offers low margins and very high receivables. Are there other such businesses just for learning??

Also why are promoters are not seeking any capital for the biz if it is really a high growth, high roe biz. esp. in times like these when logistics sector supposedly offers unlimited growth opportunities. Why are they bringing their stake from 100% (from early 2000s) to 50% now??

PS: M&M cud still get a high valuation in this bull mkt and the same can rub-off on Tiger

Rgds

RR

Disc: Not invested but trying to understand how to value such businesses.

This ICRA writeup may help to clarify things. As you correctly pointed out the valuation that Mr Market gives to MLog will be a key monitarable going ahead. The basic nature of the business seems to be thin margins. However, ROC has been good both for Mahindra and Tiger despite the challenging margin profile. The upcoming Tiger Logistics results are awaited and I am keen to see whether their foray into Defence Logistics - which is a high margin business has born any fruit so far. There has been tremendous activity in the Defence space with companies like Solar Industries showing good growth numbers. BEML has also indicated a growth oriented future. Their decision to get into Defence Logistics is well timed but so far no indication as to what is the scene on that front.

The writeup mentions that Mlog is trying to get into export logistics ( international freight forwarding) after being a big player in domestic logistics ( it aquired Lord Freight for that ). The reverse is the true for Tiger. While not a big player in export logistics, its focus has been export logistics from the start and now the management commentary seems to allude to the possibility of doing domestic logistics. Mahindra Logistics -R-06122016.pdf (151.2 KB)

The 3PL space has been growing at about 21%. There is another possibility of Tiger being taken over or acquired that cannot be ruled out given the consolidation that is happening in this space.

Not that i am aware of. There was a promising uptrend that developed in tiger logistics alluded to in my earlier posts which i was pretty sure would test its 200 moving average but that faded away as it was a correction in a downtrend. I am very optimistic about the business prospects though but that could be because of ownership bias so one must take that into account.

Although easier said than done, one must resist the temptation of creating bull stories about the company when prices are up and bear stories when prices are down. So i am learning from others with a better emotional and rational rudder than mine.

My own sense is that TGL is growing its revenue & earnings at a pace that is slightly less than the sector average so PE expansion is not happening and a PE contraction is underway. So even if the the EPS may increase YoY the stock price will remain muted. The blockbuster returns come from a PE expansion with that PE remaining at that elevated level for several time periods. This generally happens in high quality businesses with a proven track record of consistent revenue and earnings growth. TGL is not in that league yet but in a very nascent stage of its evolution.

TGL could be one of those happy stocks that you can accumulate over quarters while the price doesn’t move. If the performance continues, the market will one day see it for the asset-light high return company that it is.

Or till some P, R or K type chap buys a big chunk and rigs it.

How do you folks see the price increase in diesel to the order of 7 - 9%

after the everyday free pricing came into effect. Obviously it will hit the

margins of all transport logistics cos. Couple it with the reduced freight

demand due to the disruption of GST in July and August, the topline shall

be impacted too. So a hit on the Income and expense too in Q2. IMV, Q2 is

not going to be good at all for all the logistics cos…Views welcome…

Addressing to your concerns, I would like to mention a few points.

Diesel prices are likely to go up when a long term perspective is taken into effect. But, the fact remains in a country like India it is not very likely in near term that we see a mass shift to alternate fuel and/or use of Electric Vehicles as far as Logistics Transit is concerned. So, the fuel price hike and its effect on the margin is likely to hit all the logistics players equally, but at the same time as you cannot do away with the Logistics support it is not very likely to hit the business models. Besides the abolished Octroi would mean a overall reduction in transit time even to the extent of 30% on longer routes and that directly means reduction in fuel consumption as well as savings in servicing costs.

GST roll-out is an absolute boon for the large logistics players in India. So, in contrast to your views it is very likely to increase the topline of all such companies. Let me tell you how. First of all this industry is one of those few around, which was largely ruled by unorganized players (Such as, small tempo services, roadlines, and even individuals setting up business with absolute minimum number of vehicles) who were enjoying a lower tax rate and even in most cases evading the whole systems of taxation as they used to largely operate in the local levels. Now with already an established set up larger players would enjoy margin advantage compared to these smaller players. Coupled with that, warehousing networks should also come in handy. But, I absolutely agree with the point that there is all possibility of temporary disruption which might hit Q2. But down the line, within 4 quarters time frame entire flattish kind of topline is likely to get compensated.

Third and most important point to mention is, if your concern is with Tiger logistics Limited (which is not clear from your post) then let me clarify, TGL is a 3PL and their business model is not a comparable one to the likes of TCI or VRL and their primary business happens to be providing the players like Concor, TCI and many others with Strategic Logistics Solutions rather than transiting the freight themselves. Out of the concerns you have raised only the GST related one is likely to hit at the domestic level to TGL as the Strategic Warehousing Offloading and transit is no longer a worrisome isuue for the feeders of TGL, but provided that a lion’s share of TGL’s revenues are from overseas transit, it is not very likely to hit TGL’s topline coupled with TGL’s foray into Defence Logistics which has been pretty much an untapped segment in India which is likely to boost its topline farther.

Well, at the end would like to disclose that I’m very new into Stock market (entered in April this year) and my understandings might be a little vague, but as far as TGL is concerned, I’m invested in it and would like to hold it as long as their business model satisfies me which I’ve understood going through their AR minutely.

Would further like to see veteran boarders like @bheeshma to enlighten you and all other boardes on this matter and more.

As mentioned above TGL is a 3PL player and an apple to apple comparison would be difficult. However flexible fuel prices add another moving part to the entire logistics value chain causing uncertainty which market dont like and generally uncertainty penalises the lower rung players like tgl which bear the brunt.

The consolidation happening in this space is the big uncertainty and lowers the growth visibility runaway again. Lower the visibility lower the PE and when you look at TGL , as mentioned before its nowhere near the league and stature of the biggies & their tried and tested business models.

At a company level, the lack of free cash flow is another area to monitor and no matter however bullish one is about its prospects , free cash flow is a strong indicator of a healthy company and right now its not there.

That said, 3PL players have a self reinforcing business model and just need to keep on adding branches to increase their network - the business flows automatically.

Mr. Harpreet and Mrs.Benu seeking members approval for increasing their salary multifold.

Mr. Harpreet has drawn 1.05Cr in FY17 compared to 0.84Cr in FY16. Now he is seeking approval for 2.4Cr

Mrs. Benu Malhotra drawn 5 lakhs in FY17. Now she is seeking approval for 30 Lakhs.

For a small company like Tiger logistics which is earning 10Cr odd profit 2.7Cr Management salary looks very high.

You are completely correct and it certainly warrants a call on whether the management is looking out for shareholder interests or not. With 1.06 cr shares outstanding & promoters holding 73% of it , a dividend would serve the dual purpose of remunerating the management & sending the right signal but unfortunately that is not to be.

In the past whenever remuneration has been increased it has been a precursor to the forthcoming good results but regardless of that, one should take a call.