The competition is severe in the market with low entry barrier. This is something even Mr. Velumani accepted. This was bound to happen as in any business with good growth rates and high ROCE will invite competition and put pressure on margins. I suspect the margin can go down further

In cities due to air pollutants vitD can not be absorbed as the sun rays get blocked, it is not possible to get daily required amount of vitD from natural food source. I was low on VitD for very long time and didn’t take care of it and suffered depression and arthritis, now taking vitD by injection form.

I get my blood reports done by Thyrocare for many years , cross checked the reports with SRL , Lal etc no deviations found. Very professional and ethical company.

Disclosure : Invested recently at current price.

1 Like

90 percent of Indians r low in vitamin D ,specially in urban areas. I ve heard this stats from many but don’t know authenticity but can see many in known circle to b deficient . Reason being lack of din light n only few food items providing vitamin D source . Sorry for off topic info.

http://www.bseindia.com/xml-data/corpfiling/AttachHis/086995ac-de6b-4f2b-92bf-ad9316622416.pdf

quarterly results YOY. Consolidated income up 18% , Profit up 134%. Very good results!

disclosure - not invested but getting interested

Thyrocare has impressive business model, there is not doubt about that! 42% Ebtda margin, PAT margin of 25%. Growing 25% (slightly lower at present) despite the fact that competition is more intense than ever. Remember thyrocare is the lowest cost provider in the market by some margin. PE now 41-42 odd (significantly lower than in the past). Another dividend announced - rs 5.

Disc- invested from lower levels, adding more

Interesting price perhaps to start nibbling. 500-550 will make it interesting (10-20% over IPO price).

Disclosure: Not Invested. Mildly Interested.

1 Like

The valuations seem reasonable enough, considering the cash flows. So have taken a dip. Been following it since listing but the valuations kept me out. Had recently used their Aarogyam wellness package and was very impressed with the whole process. Very good RoCE, debt-free, growth via internal accruals. Should be a good long-term bet considering more Indians are going to be crossing 35 in the next 5-10 years. Let’s see.

Disc: Invested

8 Likes

You are right n in one of interviews vellumani sir rightly pointed out that the best days of diagnostic industry will come after 7-8 years when bulk of population will cross 30-35 plus when the need for continuous diagnosis shoots up and better insurance awareness etc will act as catalyst. I have also taken a reentry post ipo profit booking as valuations ve gone under time correction. We are getting it at 34 pe where 3 year revenue cagr has been 26% but pat cagr only 17% . I think as per CRISIL report industry is expected to grow to 72k crore by 2020 at 14% CAGR which means organised players can grow faster . The key risk I feel is low barrier to entry (lot of PE money flowing in ) ,so ,won’t be surprised if this business goes through margin contraction, consolidation n then rise of the winners . The other risk could be if some of the revenue contributing tests could be done at home by technology disruption . The 3rd risk could be hospital chains trying to get a pie of b2b business ,that’s what max is doing I think. The key differentiators for survival for thyro could be volumes as I think profitability would be a volume game but I think surely this sector will see some interesting times to check nerves of investors . Disc : Added 2% . Not yet totally comfortable with price considering low barriwr to entry n high PE activity in unlisted space

4 Likes

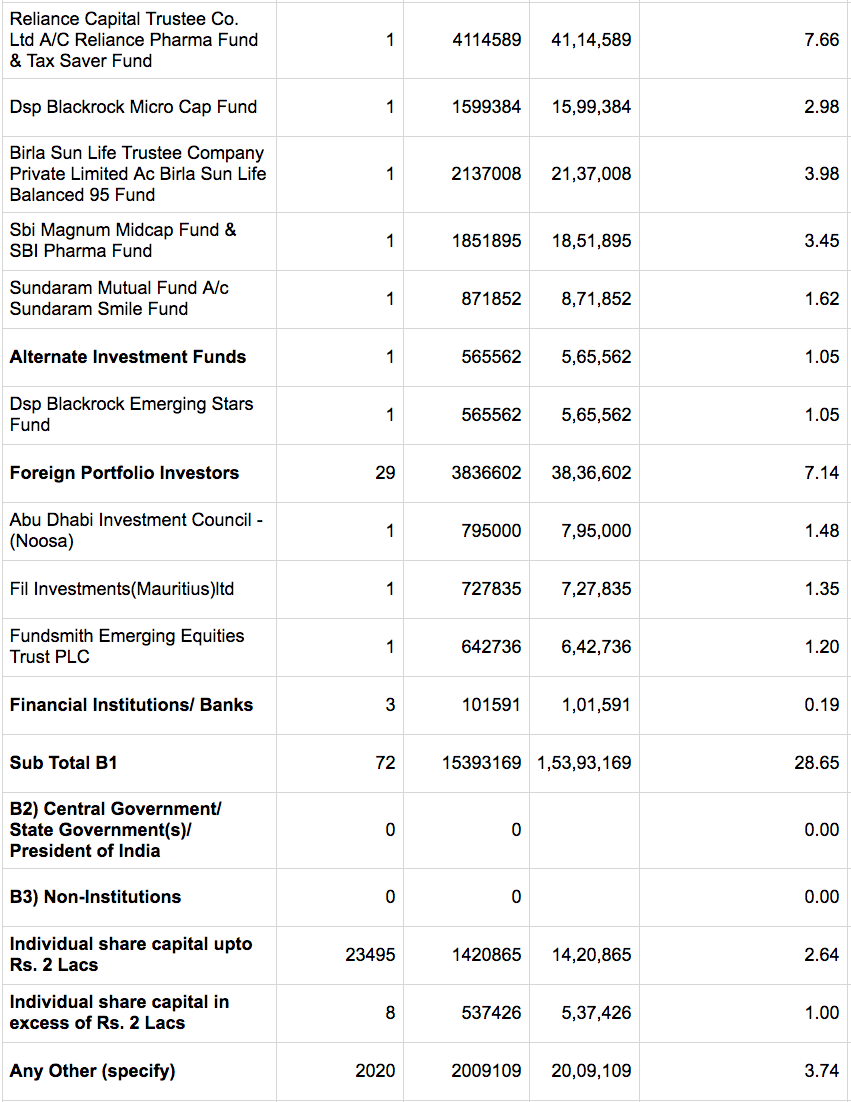

Am with you on the opportunities and threats. Interesting thing I noticed was that as of May 2016, 8.50% was held by retail and the rest by Promoters (64%) and VCs. But as of Dec 2017, retail holds only 3.64% and the rest is held by MFs and FPIs.

Clearly an institutional favourite.

5 Likes

@phreakv6 - Good observation regarding shp, mate.

@suru27 - I agree with all risks and opportunities you mentioned. My rationale for investing in this company is very straightforward…

Opportunities

- Non-cyclical play

- very efficient business model (centralized labs running 24*7)

- decent 20%+ ROE

- can’t get more ethical promoter

- business longevity

- moat in pricing power (cheapest by a good distance and still maintaining 40% ebitda)

- lollapalooza effect (healthcare as percentage of gdp is 4% at the moment; will be more than 10-12% in about a decade as India grows)

- huge potential for medical insurance resulting in lesser out of pocket expense

- volumes not an issue as even a 200 bps ebitda reduction can give them much more b2b volumes,

- incoming pricing and quality regulation will only help those organized entities already following best practices and having cheapest offerings while will increase costs for smaller players and will hurt those having low margins at the moment

- asset light model (low capital intensive)

- zero leverage

- good free cash flows

- trend setters rather than followers

- demographics in India

- and many more reasons.

In words of Dr. Velumani - The business looks easy and straightforward but is very-very difficult to scale for small players due to competition and upfront costs.

Threats

- Risks as pointed by Dr Velumani himself will be disruption. But the man himself says in the same breath - what could be more disruptive than what they have done themselves!

- Competition is there, but pie will keep getting larger over next few decades (gdp growth, healthcare as percentage to gdp, regulations coming in).

- Also, moat as the lowest priced player (think of d-mart) will help them generate much needed volumes as they market.

- Regarding hospitals themselves developing labs/conducting tests/generating reports, i think it is much better for hospitals to outsource if the provider is as cheap as Thyrocare. Just thinkas to why outsourcing in any domain is so much helpful to the outsourcer when all outsourced works can be managed internally as well. It is because outsourcer will have to focus on one less thing (can focus on the core), and provider with optimized setup and structure bungled up with volumes will be much cheaper than the hospitals themselves. Max is ramping up pharmacy as it doesn’t want patients to go out for tests; it is kind of an integration for them. But, i doubt if max will be cheaper doing tests internally than outsourcing actual testing to Thyrocare or for that matter any other organized player with volumes. Hospitals will be happy outsourcing these tests to cheapest provider and in turn keep fat margins for themselves. So an asset light structure for hospitals.

Valuation

Overall, valuation kept me at bay for last couple of years. It was trading at 50-55x at one point. Much cheaper at 35x p/e / 10x sales, but still not ‘real cheap’. In projecting valuations, everything changes depending upon p/e market assigns despite earnings growing as per estimations. Say you assign 25x exit p/e with everything else remaining same, it wd be 10/11% CAGR return in 10 years from here; if it grows its earnings at 20%, return would be close to 15-16%, though if exit multiples remains 35x and growth is 15%, returns are close to 13-14% CAGR, (plus div yield of 1.5%). Safe side 12% returns in 10 years. Best case 16-17% return in 10 years. Though, i doubt if there will be a threat to this business model even after 10 years. Rather, the moat may get stronger with network effect.

Disclaimer: Entered this month. Looking to build my position here gradually.

13 Likes

Datar Cancer Genetics and Thyrocare Gulf Announce Collaboration to Offer Oncology based Genomic Solutions

PM Modi sets target to end Tuberculosis by 2025, 5 years, before the deadline set by the UN. He also launched the National Strategic Plan for TB elimination. This plan is backed by a historic funding of over 12,000 cr for next 3 yrs. Advantage Thyrocare!

Capping pricing of essential tests is definitely not good news for Thyrocare. I hope this policy takes time to see the light of day. Govt. intervention in general is not good news for any sector.

1 Like

On the other hand, this could be a good news for Thyrocare as they are the lowest cost provider with high volumes. This will push out many labs with low volumes out of business or force them to outsource to Thyrocare.

4 Likes

Please go through last few con-calls. This indeed is a good news for Thyrocare, if implemented properly. Imagine, all those non efficient big/small players will get hurt pretty badly if this move is implemented, as it should be.

Thyrocare provides services at lowest cost in India. I have verified this multiple times. Other larger players claim that they offer better quality than Thyrocare, and thus charge higher. But in essence, there is practically no difference in quality provided by larger players. These guys are much less efficient than Thyrocare even after charging double the rates. So who will get hurt? In fact, Thyrocare’s model for quality at lowest price would get substantiated.

7 Likes

@Mridul - In general when there is price regulation and it affects your competitors at first, there is no telling when it will get to you. Regulation never stops at a safe distance. I am in general against regulation of any sort and like it better when the govt. keeps its nose out of such things. I find an unregulated sector better in general.

Who will get hurt or who will get hurt the most - I have noticed that if a sector’s prospects comes down to these questions, business has become a zero sum game with winners and losers. I like it best when most businesses in a sector are doing well and business is a non-zero sum game. The reason is that the winner in a zero sum game might actually be winning less than the leader among winners in a non-zero sum game. I don’t know if I have explained myself clearly.

Consider margins - If Company A can sell a product for Rs.100 and its margin is Rs.40 in it and its nearest competitor (lets say Company B) is selling same product for Rs.120 for the same margin of Rs.40 - clearly company A is efficient and has a 40% margin while its competitor makes same profits at a 33% margin. Now if price regulations come in and restrict price of products to Rs.80 only. Clearly Company B will be hurt the most because their COGS is Rs.80 and so they will have zero profits. Company A is the winner here and their profits will be Rs.20 at a profit margin of 25% (much less than the 40% they had in an unregulated market).

So you can say Company A will get all of Company B’s business as Company B will have to shut shop soon. Fair enough. But Company A will have to work almost doubly hard to make the same profits they were making earlier. Now the regulator sees Company A is still got a great margin - Hey why not regulate price from Rs.80 to Rs.70 and see what happens? (Maybe I can get more votes as a politician, doing this). You see where I am going with this? This has happened too many times in the past so I am very cautious when it comes to regulation.

10 Likes

Note: These are rough notes, so pardon me for being rhetoric. Just trying to put my point across.

@phreakv6 - There are two domains - Sickness and Wellness. Thyrocare is hardly into sickness (1/2%). Most of the business comes from wellness. Now, we will have to wait and see how will regulations come in and how would they impact either vertical. I think tests like H1N1, dengue, general blood & seasonal fever tests might get regulated (sickness), whereas those related to wellness might not be touched. Though, in the above article, there is a comment from one doctor who is part of that regulating committee that many NCDs related tests will be included in the capping list (diabetes, hemoglobin, iron, etc), so i could be wrong here as to what would be capped.

Thyrocare’s strength lies in providing wellness packages at a very reasonable price points. So, if a test which someone wants to undergo costs 500/-, while a package that has 50 tests (including the one that patient wants to undergo) is priced at 1200/-, many people opt for this Aarogyam package. There is no way to determine cost of individual test in these packaged offerings. Though it would be much lower than what would be charged for an individual test

Now, it all depends upon pricing caps, as to how low government prices these. If they price things even even below what Thyrocare is charging, most of the labs would be shut, as it would be pretty hard for them to cut down costs to such insanely low levels without having centralized structure like that of Thyrocare. Take for instance XYZ labs (listed company) which has EBITDA margins ~25%; though most of the tests there are charged ~1.5x than that of Thyrocare in the name of quality. Now, if government caps the cost down to Thyrocare levels (keeping in mind Thyrocare’s margins ~40%), then XYZ Lab will go out of business as they won’t make any money at EBITDA levels! (Please note that test costs are hypothetical, though i have myself compared prices for some tests at different labs. People are charging 2-3x that of Thyrocare for same test).

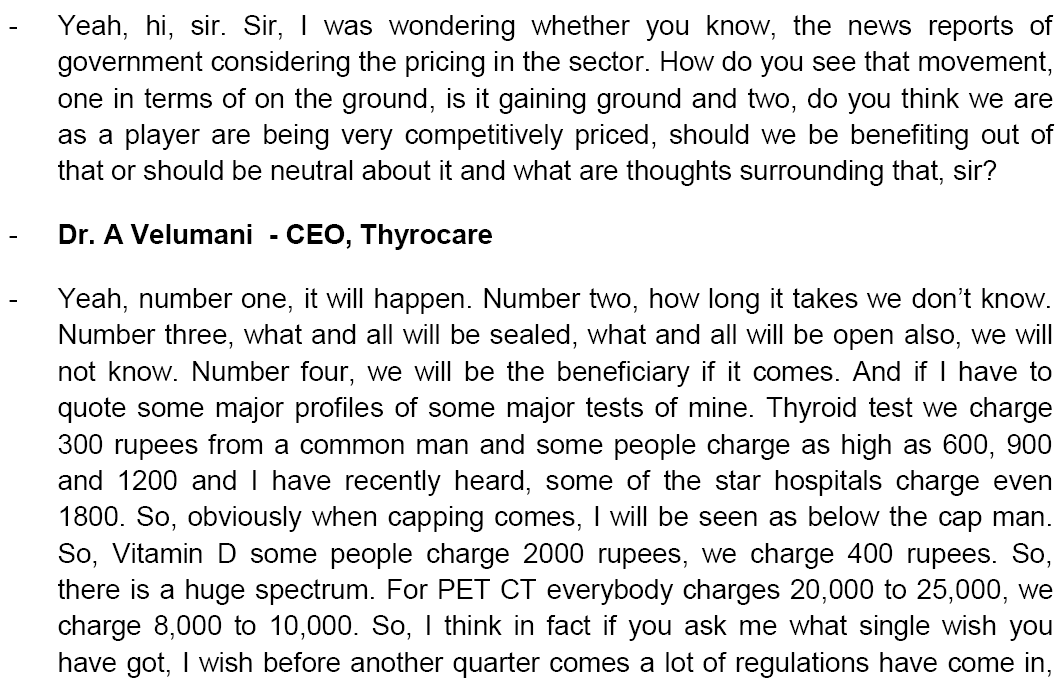

Here is an excerpt from q3 concall -

Regulations are bad, but abnormally high test pricing in a country like ours where per capita income is too low is resulting in hurting both people and the providers. How? After one level, differentiator here is price, not brand/quality (as per Dr. Velumani). So, if the prices are low, more people will be able to undergo tests that they actually need. Take for instance (note from Q3 concall) -

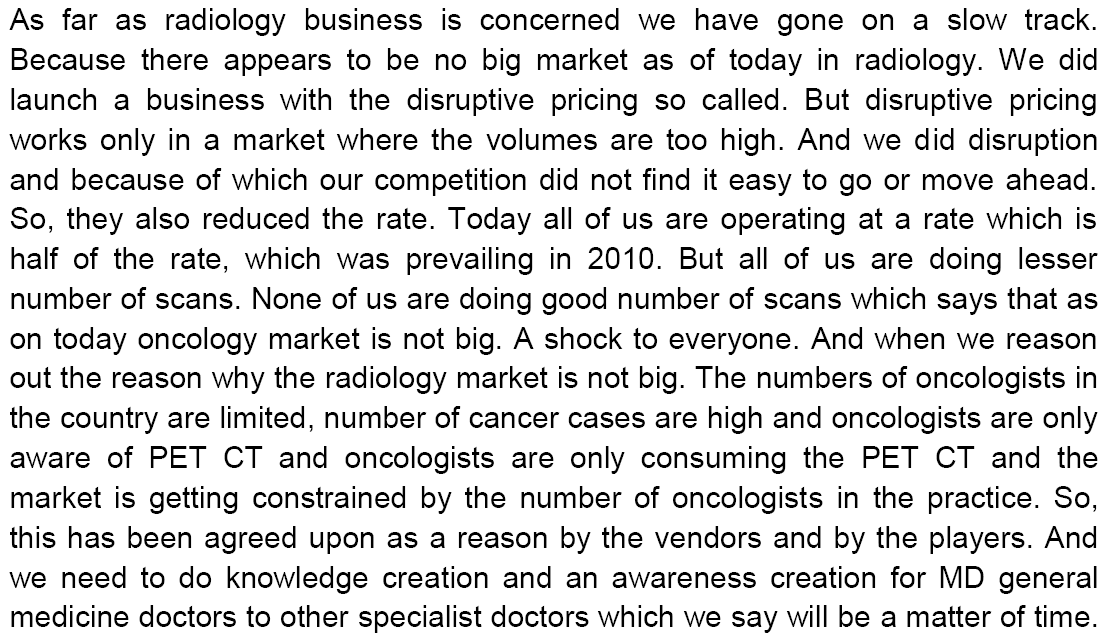

Apart from low radiologists count, another major problem in my opinion is perception that these tests are abnormally costly. Well, at most of the labs, they are! So many a times, due to lack of funds, people do not undergo tests despite doctors prescribing one. Once there are regulations, there might come a cap, which will help bring more volumes overall due to lower pricing, which would help every efficient player. Not everyone can operate at cheaper prices than Thyrocare (i have not seen anyone operate at the levels these guys can) due to centralized model. So, if, government caps at 80, most of the payers will have to shut the shops, which would result in volumes diverting to only efficient players. Dr. Velumani says volumes are much more important than margins. He also says, what can be more disruptive than what they did to the sector themselves.

I do not think government will impose pricing seeing the lowest cost operator (Thyrocare). For instance, PET scans by Thyrocare at 9999/-, whereas others are charging anywhere between 20000-25000/- for the same test. Now, if government caps it at 15000/-…well, fair enough. Though, it would be strange if they cap it at 8000/- seeing the lowest cost operator, as it doesn’t make any business sense for rest of the labs offering this test due to negative margins. So, despite volumes rising, provider count will decrease sharply, which would again be a headache for the government. (These are hypothetical discussions; took this example just to explain my point).

Now, if someone thinks they can price it like Thyrocare and survive, here’s the answer.

13 Likes

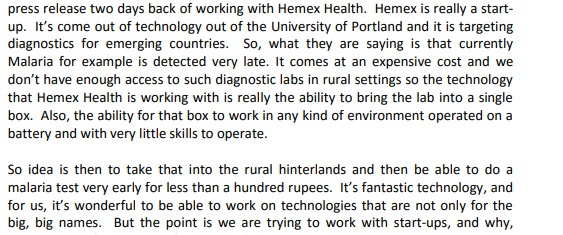

Despite this being considered a very long term investment, disruptions will happen in this space. As an investor, one should always keep an eye on new developments and their impact on one’s investments. Here is an example of a potential disruptor in medical diagnotic space (from Tata Elxsi concall) -

Doesn’t impact Thyrocare, though just want to put it here in order for us to be aware that things these days change very rapidly.

6 Likes

Hello Friends,

Some basic questions:

My understanding on the offerings are this:

B2C:

Aarogyam - mother brand for all wellness packages

Thyrocare - for Thyroid testing (Think Thyroid Think Thyrocare…)

Focus TB - for TB testing

Do we know what are the tests offered for B2B?