So you mean to say that the dumping is still going onn ?

And regarding speculation & mis information part i have clearly written “expected” I don’t think I mentioned that it will surely stop by Q3FY24 ??

And other then this did you find any other mis-information or speculative type of data in my pointers ? And if yes then please point out.

Q3Y24 is already past, Thirumalai still making losses and might continue doing so till Jan ![]()

Mitsubishi Gas Chemical (MGC) of Japan has made a strategic decision to suspend the production of orthoxylene and phthalic anhydride at its Mizushima facility from mid-January 2025.

1 Like

I G petrochem is no.1 PLayer with largest capacity around 2,70,000 ,from their recent concall

Aditya Khetan: This improvement in spread, so this is largely because of the decline in OX prices? Pramod Bhandari: I think I will put it in that way that earlier when the PA prices have gone down, then OX prices has remained more or less same. So, there is a compress in the overall margin. Now, the OX prices has remained same because of the ongoing demand which we have seen the recovery, the PA prices has improved. So, the margin has improved. Earlier, it was depressed because the OX prices remain same, PA prices were depressed. Now, OX prices has improved slightly, but PA prices compared to the OX prices have gone up sharply because of the continuous demand from the downstream segment. It’s about the size. aditya Khetan: So, PA prices have actually gone up. Okay. So, sir, with the recent price in the crude prices again

now we have started to see crude prices rising. So, these OX prices might not remain at that

level, they will also start to go up.

Pramod Bhandari: I understand that, but generally what happened is, when the crude prices gone up, there are late

lag impact on the OX and then it is on PA. So, it’s generally a 15 to 30 days lag effectwhich will

be there. Directionally, when the crude prices go up, OX prices go up and accordingly PA price

also go up. Then the crude prices go up, It doesn’t go immediately, probably by one, one and ahalf month you can see the impact on both OX and PA. One more thing I need to clarify. When

the price goes down

1 Like

Thirumalai recent credit rating report

With regard to supply, the market dynamics change significantly based on the production and consumption in key markets such as China, Korea and South East Asia. Though TCL has medium to long-term contracts with many customers, the product realisations are volatile. Imports of PAN had moderated to 94,250 MT in FY2023 from 1,21,211 MT in FY2022 due to trade protection measures on imports from several regions. Going forward, as domestic demand is higher than the domestic capacity, the offtake risk for producers like TCL is low at present and is likely to remain so in the near term. However, domestic PAN companies are undertaking significant capex. Hence, once the capacities are stable, PAN is expected to be exported for a period of 1-2 years before domestic demand matches the increased supply.

so net net there can be supply void to equilibirium for 1 yr-1.5 yr after that with new capacities coming from all the domestic palyers ,Supply will be higher than deman ,So,Should create pressure on realisation on PAN ,Having said that both I G and Thirumali both venturing into diifferent down stream chemicals.IMHO it is very important to see how that pans out

On a margin basis, it seems like Thirumalai could be at the bottom of the cycle. For a cyclical stock P/B could be another parameter to look at. On a P/B basis it still looks expensive compared to previous downcycles. Debt has significantly increased due to the company’s expansion plans. Interest burden could make things even more difficult for the company in this downcycle.

3 Likes

Chemicals - Others_12Mar24.pdf (341.8 KB)

3 Likes

Thirumalai Chemicals.pdf (4.2 MB)

how do we value such a company ??

As this is cyclical, some valuation metrics like historical Mcap / Sales, P / B may give some guidance. Neverthless market most of the times values based on the future potential of earnings. The US subsidiary has been commissioned or atleast major capex is done and the ramp up is expected to bein 1st half of H126.

You can refer the press release about the same.

Disc: Taken some exposure for tracking recently.

2 Likes

one more point of question i had is IGPL the closest comparative to this company has better ebitda margins this year as compared to Thirumalai chemicals and thiruamalai chemicals has a much more diversified business in terms of export ; so this is one thing that concerned me

1 Like

if you go through the transcript of IGPL, management claims that they get $100 / ton more on top of the spread b/w Orthoxylene and PAN. Not sure how they achieve this. They claim they are the low cost manufacturer of PAN. This could be the reason for IGPL clocking more margins compared to TCL.

2 Likes

but still the concerning thing is igpl recovered from previous year even after having some extra costs - but tcl didnt instead if you compare the eps trend of both the co’s igpl went 3x in a year and tcl didnt , 3x is a big number - the fact that tcl didnt follow the trend is a bit concerning plus the increase in debt as welll , coupled with the fact that cfo is negative after a long time is conerning .

Also if someone who works in the chemical industry could give a little insight would be great

2 Likes

From FY25 - Annual report.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/bca39717-113c-4c87-87bc-524c24220cf7.pdf

4 Likes

Hi, Thank you for the work, you guys put into this thread.

Would like to add few things:

-

Company has done a Preference issue of shares @277/share for INR 450 Cr.

-

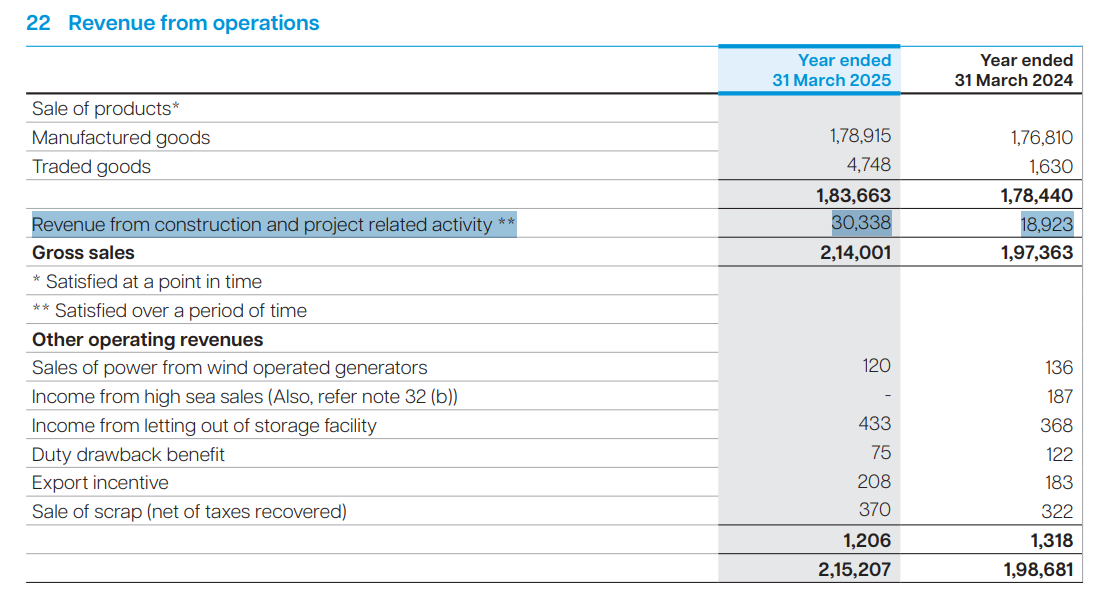

People often mentioned margin issue in comparison with IG Petrochemicals which I think in Standalone is due to Revenue from Construction routed from subsidiary to Parent Co. and Sub-Contracting that from Parent Company which has resulted in Higher Rev and Higher Cost.

In the Consolidated, I think it is due to Loss making Subsidiaries.

What caught my interest in this Company is:

- Capex will ramp up from here.

- High Likelihood of Stablisation in Raw Material.

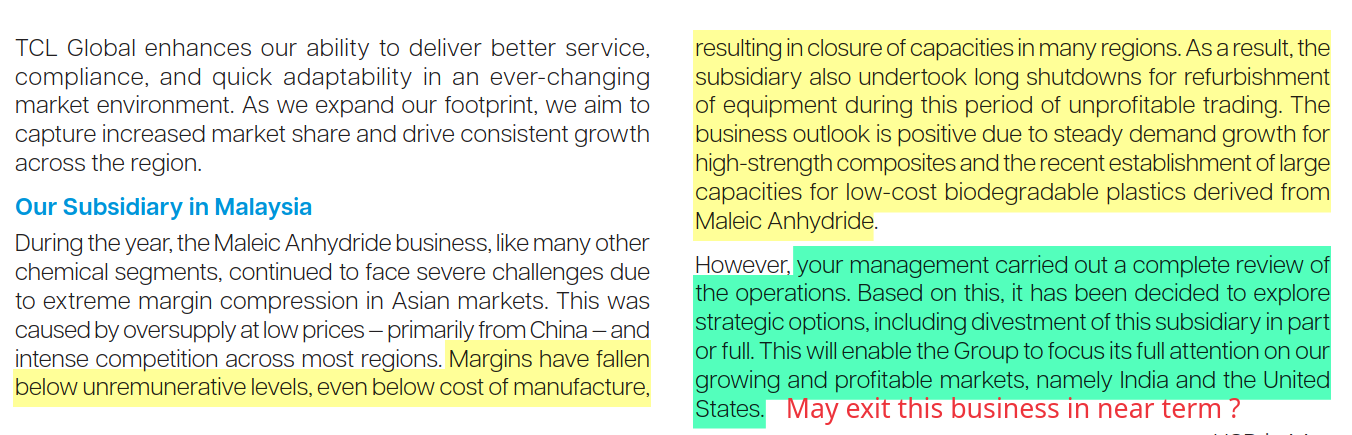

- Divestment/Partnership to reduce losses in Malaysian Subsidiary.

Disc: Currently not invested

5 Likes

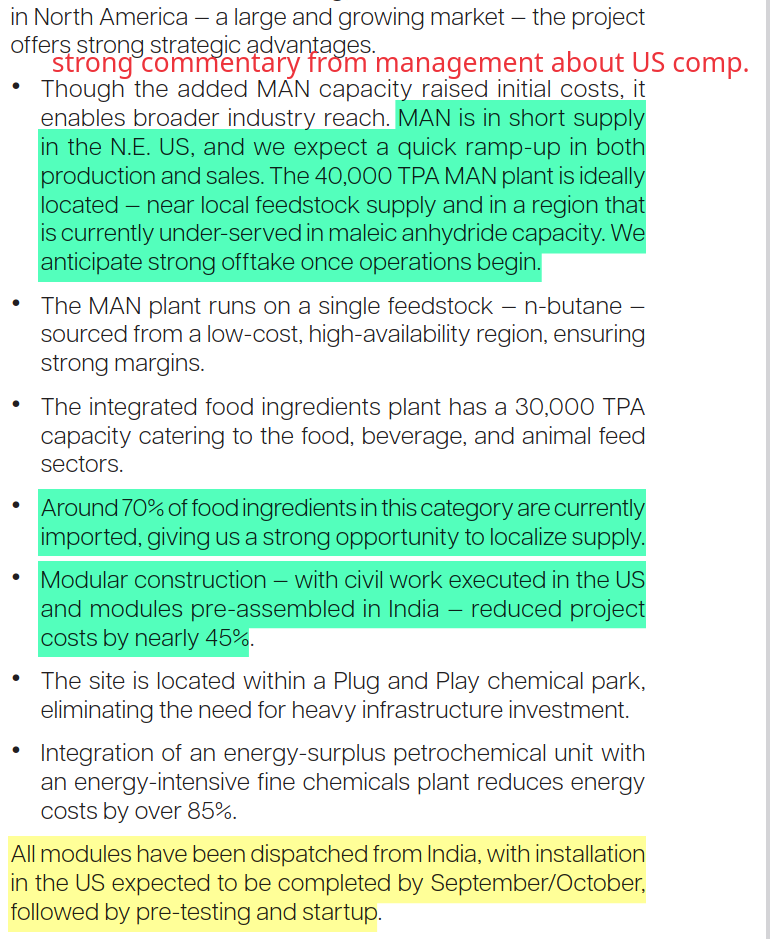

Can any body share details about the US capacity and the products that will be getting manufactured there, Please answer in details.

1 Like