He had joined BJP and may be busy due to it. Now interesting is who will come in his place ? His son who managees Rayal Seema hypos Will come ?

any idea of the upcoming capex plans or they are done with the capex for atleast near future?

They will save around 30 to 40 crs oevery year from above assured supply of electricity at rate cheaper then what they pay presently , which will increase eps by another 3 to 4 rs .

1 Like

CAUSTIC SODA manufacturere increased price today by 3 rs per kg.

Good results even in lock down and Caustic soda price have started going up only since month.

Main thing I like about the company is that even in bad times on 107 cr capital company earns more then 100 cr cash every year (65 cr depreciation+35 cr NP ). Negative is they are not paying any dividend (though they had promised before corona ) and constantly investing in modernisation and expansion.

DISC invested .

Very true. With green shoots emerging in caustic soda and soda ash segment( see share price of Punjab alkalies), profit will rise further, aided by savings in power consumption(see earlier messages). Dividend declaration is certain to act as a catalyst.

price of causitc has started going up. today its 31 at ex factory. just my dealer friend told me that those countrieswho were previouse exporter have stopped and they are importing now . he has good enquiry since last 3 days.

i am waiting for further details . any other member who has any contacts please get it confirmed

3 Likes

caustic price is 40 today at ex factory GACL. price increasing fast as paper indus demand will pick up too

company had more then 1200 cr turnover two years back. last year turnover was low due to bottom price of caustic. since few months cautic price is increasing from 16 to 23 to 40 now. companys turnover from caustic was around 650 cr . and avg rate of caustic was not over 23 last year , we can get exect avg sale rate in AGM on 27 th sept. so if cautic rate stabilise at 40 then its more then 50 % increase in sales approx 250 cr, even if 175 cr translate directly in profit then the resutls will be very good from oct quarter.

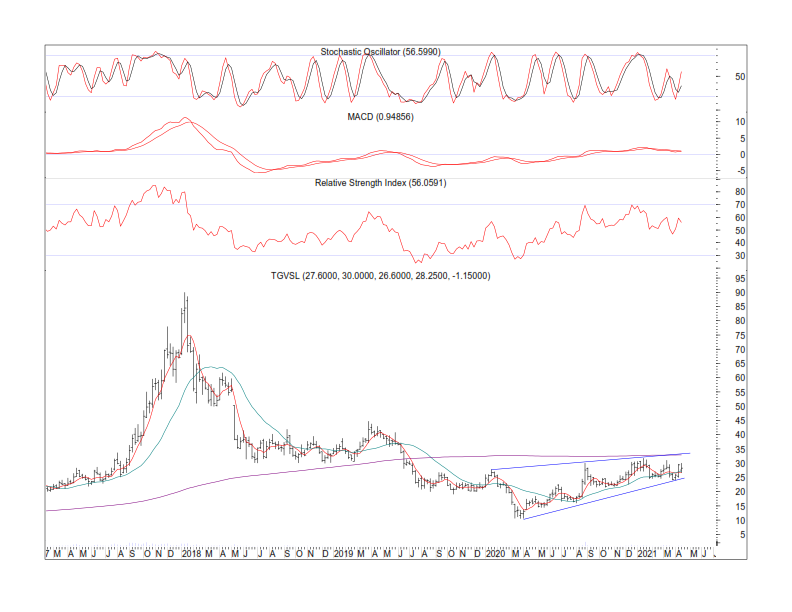

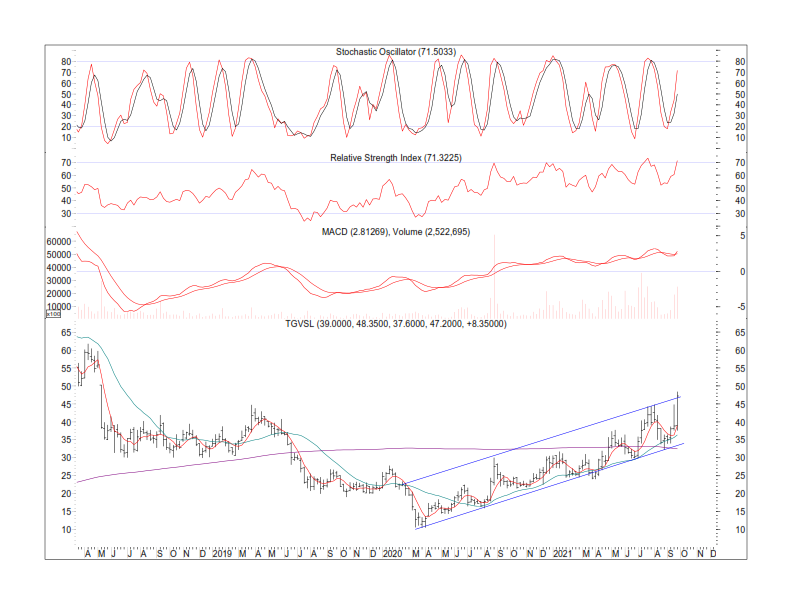

and i think chart also shows that only . after august it has shown constant higher botom after every correction

disc invested in TGVSL and having trading position too.

Excellent results. Caustic soda price was 40 in sept , and now it’s 73 . So real be benefit of price rise will be only in dec quarter. Also chloromethene expansion commercial production will be in Nov .

1 Like

Hi any views on why stock is weak despite good performance? Any headwinds which we are missing?

Biggest culprit is trade to trade segment and 5% circuit. And caustic price also have reacted from 74 top to 63 and should stabilise now at some reasonable rate .

Main thing is next quarter results . Sept end rate had reached 40 on 20 th sept. Full benefit of rate will be in this quarter. Every 1 rupees increase in caustic will bring around 20 cr to bottom line . So even if rate stabilise around 55 then TGVS will have good profit.I think if by any chance tgvs comes down to 35 around then it’s very good investment

20 cr for eyery 1 rs!!!how did you come up with that figure ?,going back to the thread you had mentioned caustic prices at 24/26 back in mar 2020 company posted bottom line of negative 10 cr vs current quarter prices at 30 to 40 gave a bottomline of 15 cr.

Check their AR for their last year production no’s and u can do little homework

1 Like

Here, we must remember that it is a commodity stock. In commodity stock , one can make very good gains if one can time entry and exit, which is very difficult. Having said that, this stock is one of the best in the industry as it has shown profit at worse level. Caustic soda price is on the rise and present Qtr will show highest average price level . Company has done well on power front, which has big impact on price. Given all these tailwinds, this is expected to show good profits.

1 Like

company had produced 206382 mt of caustic and potash in year 20-21.a single rupee increase in price brings extra revenue of 20 cr.their installed capacity is approx 300000 mt and last year plant had operated at around 70 % , that also in worst covid time and lowest price of caustic. also bottom price was 18 but last quarter caustic had started moving up from sept month only and reached 40. so even in dec quarter if average price of caustic remains 45 then also company will be able to show good results. chloromethene price also have gone up and company recently doubled capacity wich was going on stream in nov wich will also add to profits

company has recently taken permission to invest in its pharma company of their group .

https://www.brilliantbiopharma.com/

being commodity company at lower rates its very attarctive .

Ps : Also they have said in agm that now they will move towards speciality chemical , instead of expanding caustic or chloromethene

They already are in speciality chemical by their sister company sh rayalseema hypo. Wich is adjacent to TGVS and managed by his son

disc : have trading as well as investment position

5 Likes

ed293f10-23b7-44e4-b547-404652759de7.pdf (bseindia.com)

chloromethene expansion over and commercial production started .grasim has just started chloromethen plant on 5 th nov its capacity is half of TGVS. grasim expect 400 cr addition in turnover , tgvs has double the capacity of grasim after the expansion . in full year it can easily add 700 cr topline as its previouse capacity was already running at full capacity.

RM of chloromethene is chlorine and its waste products of all caustic company as they many time have to pay for disposal of chlorine when its not in demand. so win situation for caustic manufactureres

1 Like

Excellent results against 10 cr profit last year q32020 this quarter it showed profit of 41.cr add 28 cr one time extra provision and total profit is 69 cr in this quarter.

Stil price of caustic has not gone down and instead it has gone up last week further to 68 due to Ukrainian issue.

This quarter also it will show such supper profits .

Result is good, but better was expected. Other companies in this sector has shown better margins. Power cost has gone up by 50% QoQ. Last year company paid 67 cr to AP Gas Power for regular power supply at lower rate. What happened to that ? Other expenses have doubled QoQ. Price rise is not reflected in bottom line on commensurate basis. Deferred tax shown as 11 cr. Apprehend that management is reluctant to show more profit. And if they will not payback to investors now, then when will they pay?

1 Like

Excellent results as expected due to commodity cycle