What is the source of information?

Even Reliance Nippon acquires 3L stocks

Tejas Networks Ltd - Disclosures under Reg. 29(2) of SEBI (SAST) Regulations, 2011

https://www.bseindia.com/stockinfo/annpdfopen.aspx?pname=c5e6d2af_efbe_4bc7_8dff_d2f159b9e051_160459.pdf

But SBI LifeInsurance has also sold a large chunck at 90 on Friday.

Source: Stockedge

Looks like there is lot of selling pressure in the stock which is providing very attractive entry points. But noone knows for how long the pain will continue.

It will require some good quarterly results to change the sentiments. I am surprised why insiders are not buying at these attractive levels.

Disclosure: Invested, accumulating with the falls

Those ESOPs are hardly worth anything … ~1Cr and I guess it is good that they are giving it as they need to retain ppl … In campus even 10 yrs back they used to have a pretty good brand name for compensating employees well + learning was good for core E&C engineers

1 Like

Anyone knows any information on the ~250 Cr outstanding dues pending from BSNL? As per last Q&A, they were saying they should try to get it in September.

[If they get it, the cash position itself will be ~500 Cr while the Current m-cap is 720 Cr]

The company seems to have a pretty active FB page. Check this out - https://www.facebook.com/TejasNetworksOfficial/

Looks like the CEO was recently pitching in Rwanda & now the CTO is in Mexico. They seem to be at least trying their best to improve international sales

Hi Sarthak,

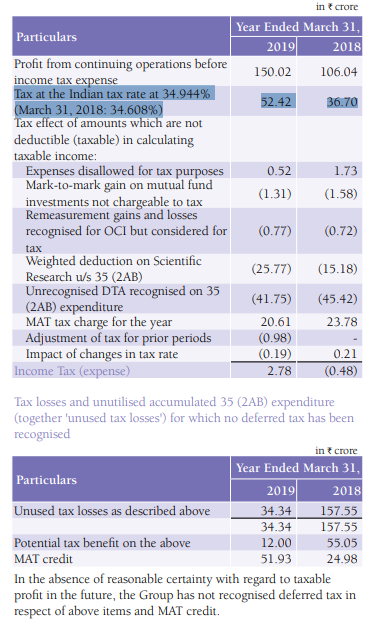

I am no expert on taxation. But my understanding for the low taxes is due to 2 reasons:

- Company is paying MAT

- Deferred Tax Assets accumulating from R&D Expenditure and Previous Year losses (FY15 and earlier)

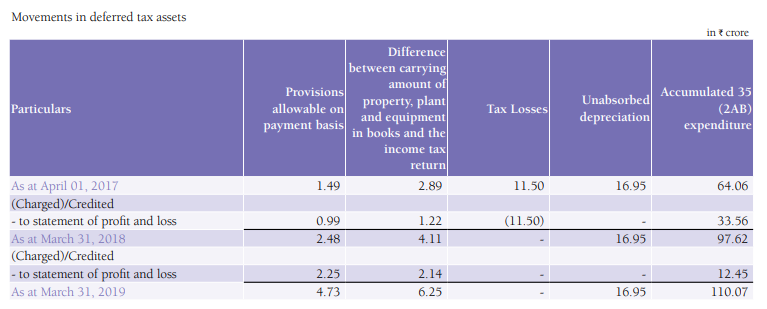

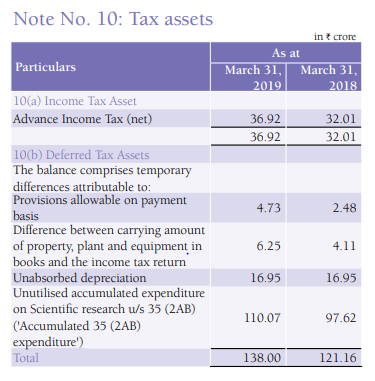

Attaching excerpts from FY19 AR

The Group has recognised deferred tax assets on brought forward depreciation losses and accumulated 35 (2AB) expenditure. The Group has estimated that the deferred tax assets will be recoverable using the estimated future taxable profits. The unabsorbed depreciation and accumulated 35 (2AB) expenditure can be carried forward indefinitely as per Income tax law and the Group expects to recover these through future taxable profits

Despite the P&L showing negligible taxes, they have accounted a reasonable cash outflow for it on the Cash Flow Statement:

3 Likes

Hello,

Just wanted to understand the investment case for Tejas Networks.

So the basic premise is that the government receivables are safe but long delayed and the international business will progressively replace most of the Bharatnet business. Is my understanding correct?

How long would you be willing to wait before the receivables start becoming iffy.

Thanks

Tejas has entered South Africa in a JV with Tsiko Africa to provide rural connectivity. Looks like its a similar project like Bharatnet.

2 Likes

Thanks for the link @nityanandparab

On a lighter note, I was amused by following statement in article.

“SA’s ambitions broadband connectivity project – SA Connect – aims to deliver widespread broadband access to 90% of the country’s population by 2020, and 100% by 2030.”

I wonder why it would take only until 2020 to reach 90% and another 10 YEARS to reach 100%. Nevertheless, its good to see Tejas partnering with local companies in various countries. What is disappointing is that Tejas has not been doing well domestically apart from PSU based projects.

While Ciena, the biggest competitor of Tejas doubled its India revenue in last one year, Tejas did not show much growth. What it indicates is that products of Tejas are not being favored over Cienna and the later has not only been able to tape the Telecom infrastructure growth in India but also take market share from players like Tejas.

Following document talks about market share of telecom equipment companies in India. It’s a year old report, not sure about the current statistics.

Following document mentions that growth is expected to be more focused on WDM where Cienna is the leader while Tejas is leader in aggregation.

@sarthakkumar19_ Like you said, investment thesis for me is more based on growth expectations from USA and other countries. I still would like to understand more about why Tejas is not doing well in private sector domestically. What keeps me invested is the large addressable and growing market for Tejas and the fact that Tejas has just started working on Sales in many countries and for the kind of business they are in, it takes time for such efforts to show results. In USA, they have moved from being an OEM for some company to selling under their own brand name, this also takes time and might be very beneficial in future if executed well.

Disc:

Invested

8 Likes

Since the South Africa project is somewhat similar to BharatNet, is it possible that they end up having receivables like BharatNet

Easy to achieve it in urban and sem-urban densely populated areas where 90% population lives. For 10% needs vast geographic coverage and large investments.

1 Like

Great technology and all is good but at the end of the day, its whether you can sell your products.

1 Like

Products of Huawei and others are far superior to tejas. Also, they are available at no additional cost. So tejas has to always compromise on margins unless it is government tenders where there are other ways to cut cost.

Can you please elaborate on product comparison more? I would like to understand why Huwaei is better than tejas in terms of product quality. If that is the case then thats really important part for analysis.

Thanks.

1 Like

What I understand from these kind of products, every company products has to match standard specifications. So there will be ‘X’ features every company product meets specs and no differentiation around that.

On top of product spec, every company has the freedom to add specific features and promote the benefits of those. Huwaei and all claim, they have some latest features, higher density, future ready and less upgrade required etc but not many customers really buy in to those.

Finally it all comes to the cost. Can Tejas sell at below the cost of Huwaei matching all the features required by customers? If no cost advantage, what is other intangible benefits Tejas brings to customers which Huwaei can’t give.

I am hopeful Tejas provides better customer support, technical know how than the Huawai engineers. Question, are they able to sell this to customers effectively, to command higher price, we don’t know.

Guys, there is a big difference. Below is what I have understood (Disc: I am not an expert. But am an E&C engineer so have some context)

Tejas works with software defined hardware architecture. What this means is they just use standard Xilinx FPGA (Field programmable gate arrays) and program it using a language like Verilog. This makes them very flexible. Huawei and other big players actually use custom chips. They cater to huge volumes so they can afford it. So, Tejas will most likely never directly compete with Huawei for the same specifications and win. But where Tejas can win will be places where there are non-mainstream requirements. So, Huawei will not be at an advantage in these cases. And once Tejas gets into an account, they can continue to milk it due to their nature of model. When specifications change, many times they can just reprogram the hardware without the need to replace it and this will be cheaper for customers than replacing the hardware. Hence, imo Tejas will find it really hard to win new accounts but whatever they win, their retention should be sky high as their model itself is a competitive moat.

10 Likes

One must not rule out the fact that there is heavy competition in this area.Even if they use Xilinx FPGA or a super computer at the end of the day it is the price that matters to the customer, if cisco or huawei can lower the cost to get a deal mean Tejas does not get it and it will be a loss for Tejas as reflected in their sales.

1 Like