Disc: invested

Tejas is part of my Indian IT 2.0 thesis. The thesis is that Indian IT is going to move from simply being a cheaper destination to a true technological destination. To that effect I have already invested in KPIT, and now would like to discuss Tejas.

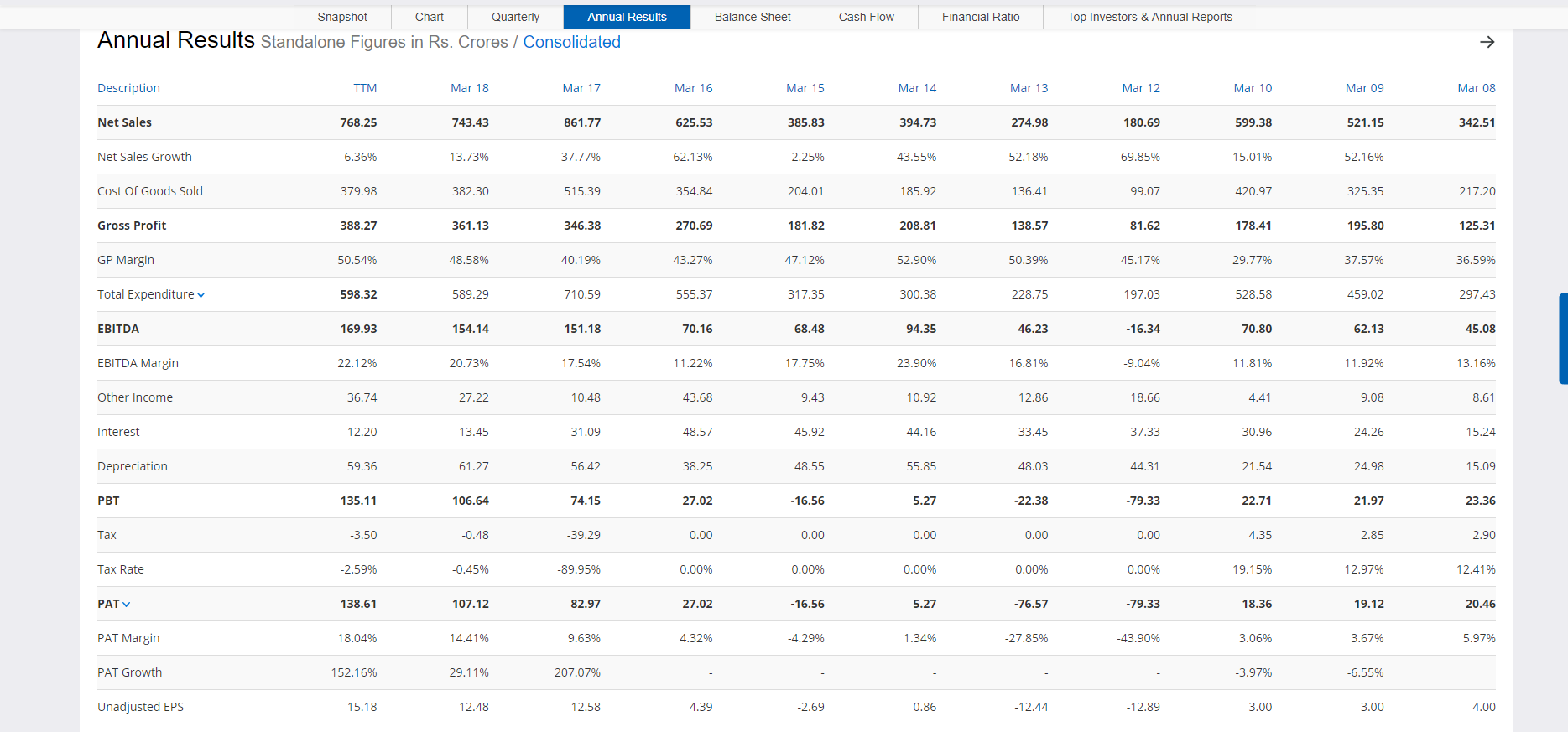

Tejas is ~Rs2000cr market capitalization optical equipment company with a TTM revenue of Rs775crore, and Rs138cr PAT. It is a virtually zero debt company, with cash on books accounting for almost 23% of its market capitalization. Tejas has a deep technology focused (340+ patents, 10-12% of revenues spent on R&D) asset-light model, with over 50% of its staff employed in R&D. Its unique “software defined hardware” architecture offers a scalable, re-programmable, customizable product to its customers that is 30-50% cheaper to operate.

I believe, like with most true technology companies, incremental growth will come at very small addition to cost (high operating leverage). If my investment thesis pans out, Tejas can become a disproportionately powerful cash generating engine even if revenues track a secular growth of 20-25%.

Business:

Telecom large capex is broadly divided into three categories:

- Mobile Infrastructure – Eriksson, Nokia, Huawei etc

- Routers and Switches – Cisco, Juniper etc

- Optical transmission – Tejas, Cienna, ECI, Adva etc

Even within the optical segment, there are two kinds of players, the passive equipment players (Sterlite tech) and Active Equipment players (like Tejas).

The overall optical transmission market is about US$18bn, and this has been forecasted to grow to US$22bn by 2021-22. But Tejas’ addressable market is about US$9bn, if you look at just the areas that the Company targets. The company is not there in Europe or China, for instance.

The active optical equipment space can be further classified as:

Access – lower speed network

Aggregation – higher speed, where Tejas is focused

Core – Tejas will commercialize its Core products in the next year

The Indian market is very small, about US$700-750mn, but it is expected to be one of the fastest growing markets due to low optical fiber penetration. Only 20-25% of Indian cell towers are fiberized (vs. 70-80% level in other large countries), with the balance using microwave technology based backhaul. With 4G already in vogue in India and 5G on the way, there is going to be a need to shift to fiberized towers to handle the massive data load. The microwave based wireless transfer simply will not be enough. Tejas currently has about 10% share of this market, because it has focused on the urban sectors data aggregation equipment.

Once Tejas becomes a true end to end player (Access to Core), their market share will rise. Tejas is planning to expand into this space, because for international bidding being an end-to-end player is preferred. Notably, Tejas has focused on an asset-light model where it invests only in the R&D and not in the manufacturing of equipment. So the transition to an end-to-end player is unlikely to result in significant Capex. They partner with companies like Cyient, Samena etc, who do the capex investment for manufacturing, while Tejas does the design of PCBs and the relevant software and algos.

Tejas business model:

The company has a unique business model in the sense that its products are what it calls “software defined hardware”. What I understand is that the Company uses mass market blank silicon chips that have diverse applications (they are used in telecom, defence, aerospace, consumer electronics, automobiles etc) and then puts a layer of its IP/ software on these chips to convert them into optical products. This has two advantages, i.e. since these chips are on the mass market, the suppliers cannot squeeze Tejas on the hardware front. Additionally, this makes the chips re-programmable and scalable allowing new technologies and requirements to be programmed onto them without replacing the hardware (these updates are required when a new standard comes to market or say when 4G is changed to 5G). Apparently, the Company expects that the overall cost of technology for Telcos using Tejas products is about 30-50% cheaper than using traditional alternative optical products. Tejas is able to implement changes faster and has time to market advantage for its telco client.

The moat to this business is Tejas as a strong headstart in this “software defined hardware” area for optical applications. They have built up a huge IPR library in this space (340+ patents, 250+ silicon IPs, 3 million lines of embedded code). None of their large competitors have even started on this technology at all. It is not that large players cannot do this, but it would require a big re-engineering of their product philosophy. They are already committed to their traditional model because of the scale advantages it offered them. They are used to buying “fixed function silicon chips”. So when a new standard comes in, the larger players order these new chips and implement them on their networks. Because of the scale of their orders, they are able to get very good price points from their vendors. Had Tejas used this same strategy, they would not have been competitive as the same cheap price points would not be available to Tejas due to its smaller order size.

Tejas’ value proposition for its customers

This is typically a sticky business where telcos tend to stay with their tried and tested vendors. The industry is very standards driven, so strictly on this count there is no differentiability between one product versus another.

However Tejas’s chip being a re-programmable and scalable chip allows them to customize it for the needs of each customer . For example, Tejas can help its customers to leap frog technology generations. Usually traditional vendors will move with tech cycles. So when 2G was in vogue, they built products for 2G, then when 3G came and industry shifted to 3G, they started building products for 3G. Tejas generic chips can be used across these technology cycles, due to their programmability. The same product can be used across generations. Especially in markets like India where 3G came very late in 2010 vs. developed markets where it had come in mid 2000s, then suddenly 4G came in 2014. This reduces capex for these rapid changes, as new technology requirements will be incorporated into the existing product itself.

Although Tejas products may have comparable pricing with its competitors the nature of the product means that one should look at the total cost of ownership (TCO) over a period of time. Tejas has demonstrated through internal case studies etc. that the TCO of their products is lower by 30-50% vs. its competitors (across its geographies).

Growth drivers for Tejas

Biggest growth driver is the increasing data consumption that we see In India and around the world. All major operators in India use Tejas products in their networks. The Government flagship BharatNet scheme which aims to connect 250,000 gram panchayats is also a key demand driver for Tejas, especially in the context of the “Make in India”.

Apart from organic demand, there will also be replacement demand from those Telcos that are using competitive products as they strive to cut costs. As mentioned earlier, the TCO of Tejas’ products is 30-50% cheaper than traditional systems. Tejas will, I believe, be able to sustain this cost advantage due to its asset-light strategy, reliance on generic chips, and its low cost base in India.

Management quality:

Tejas has excellent management pedigree that includes Gururaj Deshpande (ex Sycamore, Coral networks etc), V Balakrishnan (ex CFO of Infosys), and Ms. Leela Ponappa (ex Ambassador) on its Board. The senior engineers and technology architects have been with Tejas for a decade plus. Tejas hires fresh graduates from premier institutes and develops strong in house talent.

Key financials:

3Y revenue Cagr (FY15 to FY18) -> 25% (Co. has guided for a 20% Revenue Cagr over next three years)

3Y Ebitda Cagr -> 30% (Co. makes gross margin of ~40%, near the industry best and may have upward bias going forward)

3Y PAT -> Rose from loss of Rs18cr in FY15, to profit of Rs107cr in FY18.

Operational efficiency:

ROCE rose from 3-4% level in FY15 to 10-11% level in FY18

In the same period, Fixed asset turnover has risen from ~3x to 6x. Given its asset light model I will not be surprised to see rapid acceleration in ROCE, as revenues increase.

Debtor days fell from over 200 in FY15 to 160 days in FY18

Cash generation:

CFO-> FY15 Rs76cr to FY18 Rs239cr

FCF -> FY15 Rs37cr to FY18 167cr (FCF yield of over 8%!)

Tax:

The P&L impact of tax on Tejas’ books is currently zero. I assume that it because of the benefit it gets in tax computation for its R&D expense. The MAT that it pays is reported in the balance sheet assets side as it expects to get credit for the same when tax liability starts materializing.

Overall I think this may be great business for me to be invested in, available at reasonable valuations.