Valuation is resonable, it’s trading around 12 PE in such an expensive market. The risk is not overvaluation, the risk is some day company may default on its debts. Worries of PE contraction should be lot lesser than defaulting on its high debt and going bankrupt altogether.

I think valuation wuth an EPS of Rs 38 for FY17, the stock is trading at trailing P/E of 18.3 times, which to me looks stretched and should correct in times to come.

Besides, I do not know but I have a doubt if the company delays in making payment of interest to lenders. Every year the balance sheet shows interest accrued and due on the liabilities.Have not seen such entries in many of the clean balance sheet. Just wondering why this line item appears. These things are scary along with when valuation stretched. Looking at larges investors with stake in the company, incremental buying is happening. One need to be careful with such heard mentality because large investors have entered at much lower levels and their cost of overall acquisition is pretty low and they are already sitting on multi-fold growth. Any black swan event can make them exit instantaneously without heavy loss of profit.

Hence one need to take a cautious call and approach here. In my belief one should invest in stock specific equities only if we understand the market, business, organization structure, accounting and management philosophy. Else let fund managers do their job to give average return.

In pursuit of multiplying returns over short period of time, let us not blow up things.

These are my personal views. I have still not invested in the stock and will do it only once I get convinced. It does not matter if you lose out on the initial 30 to 40% rally if you are searching for multi bagger in a small and mid cap, because in my belief the comfort is more important which is what is not coming out in TCPL Packaging.

2 Likes

I am in complete agreement with you here. Have stayed away from investing in the company for the same reason despite high growth being reflected on the income statement. The owners earnings have been negative throughout and this sort of growth is of no value. Incremental ROCE has been declining and the company is using debt to pay dividends. I do not understand the need for continuous capex using debt and equity. Lets not forget that D/E will look lower post QIP not because debt has reduced but because equity has increased. The company can do 1100 cr of revenue at full capacity then what justifies a higher capex now?

4 Likes

Does any one have clue about the preferential allotment. I mean who were the investors and what are the objectives. Surprising the company raised barely Rs 24 Cr through preferential route. Just wondering why do they need to dilute equity and if they have to dilute why barely Rs 24 Cr worth of equity raising.

DSP Core Fund - A long only fund on the AIF platform (3 lakh shares), this is sold to HNI’s and Super HNI’s, min investment of 1 Cr needed

VEC investments (1 lakh shares)

4 lakh shares issued on an existing base of 87 lakh shares. Not a large dilution, 24 Cr also ain’t big enough to make a substantial difference to the balance sheet. Shares to be issued at INR 600

The share price got beaten down over the past 2 months on volumes that were not high, the spike this week on the contrary supported by high volumes (more than 30K per day). Looks like the pref allotment has done the trick to the share price already. The last time this company made news was when a PE firm gave an enterprise value of 400 Cr to Parksons packaging in 2014, TCPL was hardly trading at 200 Cr market cap then

Yet to make any conclusions on this yet, am not good at deciphering promoter actions and intent yet. Anyone with inputs on this welcome

1 Like

This is not good though, in first place why promoter would raise equity for barely Rs 24 Cr. And why such preferential treatment would be given to a fund house to buy at nearly 15% lower than the current market price. Besides, DSP no other fund interest was seen in the overall issue. Surprising that entire preferential issue got absorbed majorly by one fund that too which has a lock in of 4 year period (DSP Core is a close ended fund with lock in of 4 years and heavy exit load and target IRR of barely 10% - Are you Serious in such market the fund is selling the objective of barely 10% in such market for over next 4 years - Why someone will invest for barely 10% CAGR when normal open ended mutual fund generate more than 17 - 18%). Not pretty encouraging news as far as the preferential issue is concerned. I was expecting some big ticket fund raising of Rs 100 to Rs 150 Crore which will be used partly to fund capex and reduce debt). But why promoter need to raise barely Rs 24 Cr.

Most AIF funds in the market work this way. They have a fixed management expense of 1.5%, hurdle rate of 10% with high watermark and a 10/15% share of profits after the hurdle rate. MF’s charge you expense ratio irrespective of whether you make money or not, 2% is massive when the funds delivers negative returns in a year. On the other hand the AIF makes 2.5% only if the investor makes 20%, all in all not so bad a deal. HNI’s are lapping up all of these products anyway

At an issue size of 24Cr one fund is more than enough to absorb this. I however agree that the logic of this issue size is not apparent to me as of now, it is just about enough showcase investor interest in this but not enough to make a difference to the balance sheet. I guess this deal would have been driven by the investors approaching the promoters rather than the promoters going in search of investors.

DSP is also doing something interesting - they are shifting some of their high conviction bets in the small cap space to their AIF’s rather than buy this through their normal MF. That however is another discussion

1 Like

![]() The concern of high debt and never ending capex story funded through debt is still a hangover.

The concern of high debt and never ending capex story funded through debt is still a hangover.

This per Capex which Mnagement does they make sure theyhave IRR of 20% . See It is very difficult to do FCF calculations when company is doing capex after capex . Ideally you should look at individual machine level . Like Ambika does EBIDTA per spindle .

Capex is not bad and when company is small there is no other way than raise Debt . Look at these figures and these figures say something .

TCPL PACKAGING LTD SALES GROSS PROFIT EBIT PAT

TCPL PACKAGING LTD SALES GROSS PROFIT EBIT PAT

10 YR CAGR 22% 22% 28% 32%

5 YR CAGR 20% 22% 33% 49%

3 YR CAGR 22% 27% 42% 75%

1 YR GROWTH 19% 26% 25% 19%

RoCE 11.07% 8.67% 11.31% 11.84% 13.09% 12.67% 15.93% 15.19% 20.54% 19.83%

ROIC = EBIT MarginCap Turns(1-Tax rate) 8.93% 7.02% 8.02% 6.68% 8.50% 8.58% 10.58% 9.62% 15.36% 13.74%

And you are right DSP is not fool to invest for 10 % return . They are expecting more than 25 to 30 %

Roe can look optically high due to leverage…capex not just for a small but

also for large company is justified when the utilization levels are

high…the company is just operating at 60% and using debt to fund it’s

capex continuously and does another qip post that…I don’t think this is

prudent capital allocation

It is though not excited. MF bet can horribly go wrong as well, we never know. We have seen what has happen to DSP’s favorite pick in case of Satin Credit. Shaily Engineering has been a big laggard in super exuberant market.

DSP Core is a newly formed fund, formed in January 2017. The networth of the fund is barely Rs 110 Cr with only two stocks so far invested. TCP will be the third investment and the networth will become Rs 130 Cr. The fund as per their mandate need to invest in 15 to 20 stocks. We cannot be sure if all such 15 to 20 stocks will give superb return. As an individual we are taking a call on individual investment but fund will have to showcase overall portfolio performance. Hence just because DSP has invested one should not be upbeat and take purchase decision.

The concern as I said is still looming over. I am restricting myself from the purchase decision. Need more clarity and will await till August 6 to get more clarity in AGM.

On a scale of 10 (with 10 best rating), I will still hold my rating up to 4 because of weird way of capital allocation. There is no need for aggressive capex funded by debt and paying divided out of debt when capacity utilization is barely at 60%. This remains a big concern.

The recent run up was purely because of news that the fund is buying, the management must have agreed for preferential allotment at Rs 600, hence it was not possible for fund to invest at Rs 600 when the market price was ruling below Rs 600. Hence the recent run up in the stock should be analyzed with great caution.

1 Like

AGM is now scheduled for Aug 9th in Worli.

For those of you yet to flip through the Annual report, its available at http://linkintime.co.in/website/gogreen/2017/AGM/TCPL/TCPL_Annual_Report.pdf

Interesting to see that Dolly Khanna now figures in the top 10 shareholders with 0.66% stake as at Mar 31, 2017. Anil Goel has increased his stake in Fy17 marginally upto 9.27%.

Disclosure: Been invested for a while - waiting patiently for operational leverage to kick in from all the capex spends these last few years

Annual Report at least provide some commentary. It is not so prudent to rely on management commentary always as you most of the times get swayed by management words and emotions take control over your mind and intellectuality. At least I am giving a little benefit of doubt to management for maintaining that they are not going to go for any incremental capex. This will remain a key monitorable. Now numbers have to do the talk. I don’t think Q1 will be quite upbeat because of gst destocking…but Q2 onwards it should be good provided they do the deleveraging and do not deviate from their guidance and spend capex taking debt.

3 Likes

I’m invested in TCPL - it’s one of my largest holdings. Here’s why I think its a great stock, despite the -ve FCF:

TLDR; you are forgoing FCF for growth. When growth stops, you’ll have boatloads of FCF. Here’s why:

Imagine if you had a commodity in a perfectly liquid market, which you needed to buy a machine to produce. This machine costs Rs. 100, and creates Rs. 27 for you in eternity (27% Pre Tax RoCE). Of this 27, you need to spend Rs. ~7.5 each year to keep the machine running, and a 30% tax on the remainder, leaving you with Rs. 14 for every 100 that you invest, for eternity (the unlevered post tax RoE TCPL would have if it were funded purely by equity). You realize however, that since the demand for your commodity isn’t likely to decrease (FMCG products - by extension, their packaging), you use a much lower cost of funds (debt - at 9.5-10%) to fund this investment. This brings your RoE to 27%. As long as your EBITDA is large enough to support your interest coverage, you will be able to refinance - lenders like giving loans because it makes them money (NIM), so unless there is a compelling reason not to, they will give you money. Heck, its in your banker’s interest to ‘evergreen’ your loan as long as you remain a moderately creditowrthy borrower, so their loan book remains the same, and even so if you are not, so they don’t have to show you as an NPA (…although this has problems, r.e. the current NPA problem) if they hope you can someday become solvent.

Now you realize, oh, every rupee I invest I get a 27% return, if I lever my marginal investment. Why would you instead pay down debt (and get a return of 10%), rather than expand and get 27% on your marginal investment?

This is a company that will continue its ~1.5x gearing and -FCFEs till the marginal RoCE falls to Cost of Debt, at which point it will start unlevering, although even then I’d support a combination of buybacks and debt payents to maintain current gearing.

On another note; given the structure of the packaging industry (huge share of unorganized) as well as GST (no tax arb for smaller players, and input tax credit) means that a lot of business will find its way in the hands of organised players with economies of scale like TCPL

I’m extremely bullish on this stock. As far as valuations go, even after the recent run up, 9x EV/EBITDA is absurdly cheap for a 27% RoE (stable state, excluding FY17) business.

P.S. Debt should be viewed in light of earnings power, not in absolute terms. Even the most conservative banker would be fine with a 5x interest coverage ratio

9 Likes

Agree. Provided they walk the talk now. This will be the real testing time.

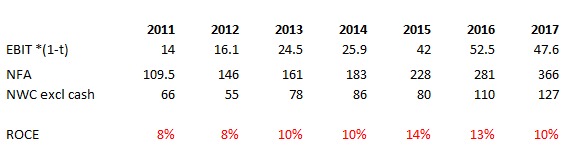

Why is everyone going gung ho about their ROCE? ROCE should be calculated post tax and below are my workings. What am I missing?

Since cost of debt is a pre-tax cost (interest is deducted before tax), and this is one of those businesses where the stability in earnings makes high gearing reasonable, it makes sense to look at Pre-Tax RoCE. Few powerplants/utilities/telecom companies would be feasible/attract private capital if we only looked at post tax RoCE.

You’re right on your observation that - if - this business could not use much debt - if it had too much variability in earnings then the post tax RoCE is quite bad, making this is a mediocre business. But TCPL is similar to how power-plants/telecom companies in say the US use debt to increase RoE of otherwise unattractive projects. I think leverage is a huge part of why this is an attractive growth business. Unlike a software company or an FMCG company, this company needs capex to grow, and without large returns to retained earnings (equity) which are only made possible by the judicious use of leverage, this company could not have increased its fixed assets this quickly, thus growing top and bottom lines.

I think TCPL is like a Power Grid Corporation, except with much better economics

4 Likes

In a commodity based business, it is difficult to maintain a ROCE of 15% plus. Good businesses bring competition and kill margin if there no so called moat or whatever we call as the special factor to hold margins. So, it is important to know what will keep ROCE alive. Could there be a situation where due to intensified competition , the assumptions while taking loan changed in future. I am just trying to think possible risks of debt in an industry which is growing and has potential to throw free cash flow. It may or may not happen but are we factoring such possibilities in our valuation metric, let us say the worst case scenario.There could be possibility that economies of scale and capex be so high that not many players enter but i m not aware and have not done such deep analysis on this industry.

However, overall despite of high debt, this was one of few stocks i had courage to enter based on factors beautifully highlighted by you. Must confess that I am not a trader by nature but has been in this stock. It was always on watchlist . Felt worth taking a plunge at 500 levels but did not find worth holding for long term at 700 due to relative opportunities(it was more of a pricing opportunities for me personally).It was more of point of time based relative opportunity attractiveness and dislike towards debt. no positions now.

I agree with your assessment of a commodity business, but this is in the long run. If we look at the current packaging market in India, apart from the 3 large packaging companies (one of which is TCPL, which imho has one of the most aggressive management I have seen in listed Indian companies), most of the market share is with unorganised players. This is a very unglamorous in which you need 1) large scale (which TCPL has in abundance) and 2) major focus on costs to succeed.

TCPL’s scale and focus on value added packaging (the rotogravure and UV printing and other value added stuff) requires very heavy capex out of the league of smaller competitors, while TCPL’s high stock price as a listed company allows it to raise large equity capital at 3x BV as well as lever that up with debt, giving it large access to funds. Yes, this is not something that will happen for 100 years, but if TCPL grows at 25% for that long, it’d be larger than india’s economy  (point being that 25% growth for even 5-10 years is huge and has insane upside…)

(point being that 25% growth for even 5-10 years is huge and has insane upside…)

2 Likes