I found this gem very late. After reading through the entire thread, I feel that the management is really ethical (which is a huge +ve for me) and they are consistently churning out Sales YoY. What do you feel about the valuation at current levels? What are the next set of growth triggers for TCPL? There was talk about entering into pharma packaging space. Have they started that? Awaiting your thoughts on this counter.

Agree with your assessment of the company. This is a converter business so it will not generate above average ROE. I expect the business to generate between 15 to 20% ROE with some possibility of generating 25% occasionally. Having said that, cashflow of the business will be steady as its customers are FMCG and vice industries. This steady cashflow will allow company to service medium to high debt thereby increasing ROE. Additionally, it has a huge opportunity to reinvest capital at these rates for several years. Company has been prudent not to go on a borrowing binge and raise capacity rapidly and try to outgrow the competition.

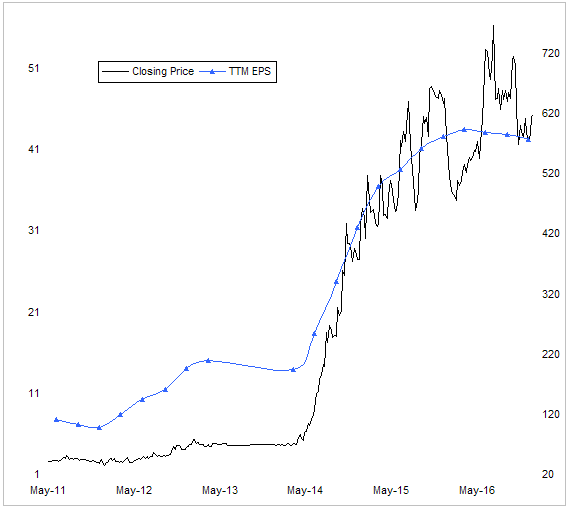

In 2014-15, company revised its depreciation policy as per the provisions of the companies act 2013 and that resulted in lower depreciation (as a % of sales) since then. This has resulted in higher net margin and EPS although EBITDA margins are little changed. However, market appears to have tracked the EPS number so stock price zoomed over the last 2 years. In last few quarters, depreciation is inching up so net margins are inching down. This is coupled with lower volume growth in FMCG industry has resulted in lower top line growth. Net profits have moved sideways and stock has moved sideways as well.

ROE in the last 2 years has gone up mainly due to depreciation policy change. This should revert average over next few quarters. Stock is fairly valued at this price. Its prudent to wait for a pullback since upside is limited. However, this is kind of stock that will not scare a long term investor as its business is stable with huge growth potential.

2 Likes

What % of their revenues come from the Tobacco Business/ Cigarettes, I feel this is very important while assessing their growth projections and the overall investment risk because if huge portion of their revenues come from Cigarettes then its a negative as a large segment is growing at a slower rate and has tremendous risk.

1 Like

I don’t about the total cigarette exposure but Godfrey alone contributes to over 15% of their sales. ITC procures from their own packaging unit. Don’t know about VST but should not be much.

1 Like

And madam can you suggest this information was as on ? And any way i can source for the latest update ?

its in annual reports; look for revenue break down and you will find income from job-work. That is the business from Godfrey Philips. In addition, in director’s report, they also report pro-forma revenue, had they actually worked on sales basis rather than job-work.

Also, while the growth volume might be at risk; cigarettes are a very sticky consumer product; and not too many packaging changes over time… aka a fairly solid revenue base. If you are looking for growth based projections, focus on their upcoming flexible packaging facility/ business.

Disappointing results:

I am going out on a limb and loading up on this one.

Asset turns at a multi year low and the company has just come off a large capex of 70 Cr which has not yielded much yet due to muted Q3 and Q4 environment. Cash profit in excess of 70 Cr at a market cap of 430 Cr and enterprise value of < 700 Cr. Likely to continue under performance in the near term though, not for the faint hearted right now, price down from 700 levels to sub 500 in no time since Q4 results

My reasons for liking this story already articulated in my previous posts here. CMP is hardly discounting a 3-4% earnings growth over the next 5-6 years, asymmetric payoff possible from here in my opinion

8 Likes

Dropping revenue growth for a leveraged business is really disappointing especially when new capacities are coming online. EBITDA margins are lowest in 4 years. This is a business with high operating leverage due to high fixed costs and high financial leverage due to low ROA. For such a business, loss of revenue can be devastating. I think market is not overreacting here but pricing in risks.

Source: Capitaline

Demonetization could have had an impact on the sales growth in Q4 and destocking in preparation for GST may impact Q1 or even Q2. But again this is a kind of business you get into if you want a stable business that is not sensative to shocks like DeMo so that’s a surprise that investors are pricing in.

A dividend cut is also a sign that this is not a one time speed bump but rather a new normal. Overall I think its better to let the EBITDA margins reach a new normal before taking a call.

4 Likes

The analyst in me agrees, but the investor in me wants to load up on this. The days of 14% vol growth and 5-6% realization growth may not come back soon, I am willing to take a bet that this is a business that can revert to a higher single digits volume growth over the next 2 years.

The selling over the past 2 weeks has been driven by higher volumes than usual which is a sign that the market is pricing in more risks and more pain for the business in the next 1-2 Q’s. I think that a business that sells to stable businesses, does not have a wide range of outcomes, is done with a round of capex that can keep business going for 2 years and is at multi years lows on asset turns can work out pretty well if the CMP is close to discounting the most pessimistic scenario.

I would expect the management to see FY18 as a consolidation year where they use the cash generated to pare down some debt and run a tight ship on operations. Demand environment will eventually get better but I am looking to see what kind of judgement the management exercises between now and Sep 2018. The balance sheet declared in Sep 2018 should tell the story

4 Likes

I have been investing only based on fundamentals over last decade. I am new to this blog and got tempted to reply on tcpl after going through several posts. It is commendable that the company has shown capability to multiply revenue as well as profitability with expansion in margins. This is not really an easy task and management has shown real agility to grow over last 10 years amidst stiff competitive market and served some of the best brands in the tobacco and non tobacco space.

My discomfort factor are limited but holding me back to take any buying decision which are some fundamental doubts.

The company has never generated or barely generated free cashflow. Every year we are expecting the capex cycle to be over and tcpl has build enough capacity to serve for two to three years and hence incremental cash flow will be used to retire debt and pay higher dividends. But every year they are throwing surprises by announcing Rs 50 to 60 crore capex and funding it through debt. FY16 as well this was expected but then incremental capex happened with incremental debt. At least we expected FY17 is the last capex and tcpl will not need any further capex for next two years but today morning again management announced of equity raising through preferential route. If no capex then what is the need for equity raising.

Company is not covering it’s forward contract position and is leaving it open and booking gain and losses without having adequate hedging policy. At least I have not read about that policy in FY16 annual report. They capitalised derivative losses in fixed assets to the extent of nearly 5 cores.

Every year they are showing interest accrued and due but not paid (though the amount is small) which is also a disturbing element. Why interest accrued and due will remain unpaid.

Bad debts are recorded every year but no reasoning is given in the annual report. (Again the value is small).

No forthcoming communication if they are going for expansion every year.

At least some of these fundamental questions remain unanswered which is somewhat disturbing.

Would love to hear the views for boarders here.

4 Likes

[quote=“blueeyedinvestor, post:51, topic:238, full:true”]

The company has never generated or barely generated free cashflow. Every year we are expecting the capex cycle to be over and tcpl has build enough capacity to serve for two to three years and hence incremental cash flow will be used to retire debt and pay higher dividends. But every year they are throwing surprises by announcing Rs 50 to 60 crore capex and funding it through debt. FY16 as well this was expected but then incremental capex happened with incremental debt. At least we expected FY17 is the last capex and tcpl will not need any further capex for next two years but today morning again management announced of equity raising through preferential route. If no capex then what is the need for equity raising.[/quote]

Gonna wait for who the beneficiary of the preferential route is going to be before commenting on this. If equity is being brought in here a good chunk of it will logically need to go towards retiring some debt. I do not think TCPL can be a free cash flow company anytime soon, the incremental asset turns won’t be high enough to turn the cycle. However if the absolute level of debt can be kept where it is while the business keeps growing, effectively funding future capex from cash flows, that by itself is sufficient to positively impact the balance sheet. That said, who gets the preferential allotment is a key thing I am monitoring

My opinion is that companies of this size and finance capability are better off staying unhedged. At most margins will compress in some years rather than the management doing some hedging nonsense they do not understand that can hurt them badly. Export revenue anyway will exceed capex going by the trend so this is something I am willing to overlook.

Agree they can do a far better job here. But again for a 500 Cr market cap company with 60% held by promoters this is not surprising at all. The management has been declaring the volume of paperboard they have been converting every year, something they aren’t mandated to declare. So I see some positives as well.

The issue of regular capex has concerned me no doubt, more from the point of view of checking if promoters are siphoning off money. What has helped tip the scales in the management’s favour on this is the fact the KBA, Bobst and Heidelberg (OEM’s who they buy machinery from) have always been open about who they are selling to in India - one can verify this from announcements in printweek.

Some of the other points I am equally clueless but I am comfortable taking a judgement call on this one given the limited information I have access to.

Disclaimer - I am invested and this is my biggest holding at cost, I am obviously biased in favor of this story.

3 Likes

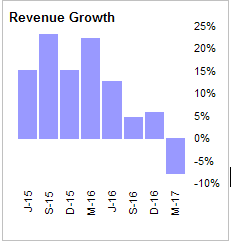

under no circumstances the current run up is justified. These are my personal views. FY17 has been a bad year and expectation were breached in terms of earnings performance. All are justifying the muted earnings because of demonisation which happened in Q3 and partially in Q4. But one need to carefully look at Q1 and Q2 FY17 numbers as well which were lower to flat than Q1 and Q2 FY16. Hence the correction happened. Q1 and Q2 of FY18 as well is expected to be bad quarter for fmcg players and TCPL performance would be no different. We can always justify rally with any rational but fundamentally the concerns and earrings growth still remain a concern and that is the reason why the stock is still trading at 16 to 17 time trailing earnings (even after recent run up) whereas peers are available at considerable premium given the performance they displayed.

under no circumstances the current run up is justified. These are my personal views. FY17 has been a bad year and expectation were breached in terms of earnings performance. All are justifying the muted earnings because of demonisation which happened in Q3 and partially in Q4. But one need to carefully look at Q1 and Q2 FY17 numbers as well which were lower to flat than Q1 and Q2 FY16. Hence the correction happened. Q1 and Q2 of FY18 as well is expected to be bad quarter for fmcg players and TCPL performance would be no different. We can always justify rally with any rational but fundamentally the concerns and earrings growth still remain a concern and that is the reason why the stock is still trading at 16 to 17 time trailing earnings (even after recent run up) whereas peers are available at considerable premium given the performance they displayed.

My take is I am going to remain cautious and will wait for some more clarity before getting a dip into it.

Are there any directly comparable peers in the listed space?

There are global players whom you can refer to for comparing TCPL. Converters will need to keep doing capex as their is endless volumes /marker share to capture. In fact PWC did study and it is know to expand your EBIDTA you need to keep doing capex ( new machines etc ). It is called capex spread

Given they have so much market to capture now especially with GST and tax regime getting tight small time converters will need to increase price if they want to survive . Packaging is very important for any brand and with shift towards private labels you would see paper packing increasing (rigid hard paperboard types ).

I suspect TCPL need to to raise equity to keep borrowing more money to launch bigger factories but point to note that they have very stable margins ( price formula with manufacturers ). If you see thier EBIDTA will rise as fixed cost gets spread over large volumes.

But yes this will never be FCF business atleast in near future but they can keep gowing revenues and proftis for more than 20% for very long time.

Hope owners keep thier financial discipline and maintain IRR of 20% for any new capex they do .

Packaging industry is filled with companies who not suceeded and returns ratios are never good except food paper packaging ( Starbuck paper cups etc ).

Need to study more about industry.

Disc : Invested 3 % of Portfolio on cost basis but usually never biased welcome opposing views

2 Likes

Interesting. Every year they need to pay around 35 to 40 cr debt. Besides service interest which is around 22 cr (including inye rest capitalized)

Overall 62 cr of annual payment obligation on current book. Plus incremental debt for new CapeX. So this outflow will continue to be at these level with upward trend.

20% IRR required free cash flow of substantial amount. I wonder with negligible to negative free cash flow how somebody can generate 20% IRR.

Incremental cashflow will continue to get sucked by repayment obligation. And what I unserstand from basic financial management also from investment principle perspective, the organizational earningso only to make good their debt is a lethal weapon and can be considerable value destructive. As I said I look at things from very simple model perspective. The real money or wealth gets generated when you use leverage or debt to multiply returns for investors. Here that is a big hangover as company is not able to generate free cash flows even though multiplied their profitability by 16 times over last decade.

I liked the company. But these elements are restricting my decisions. Would love to get convinced to buy it.

1 Like

What do you mean by IRR, to break even (pay debt) it has to generate 20% ROE ?

Look at this. Guys, including management has been talking and upbeat about justifying incremental capex with better asset utilisation or asset turnover. Asset turnover for the company over last two year has been continuously declining. RoE and RoCE both also showing declining trend last two years. Inventories rising with average inventories days risen from 68 odd days in FY15 to 71 days in FY16 and further by 91 days in FY17. The same is going to further go up because of GST transition over next two quarters at least. This will further stretch their working capital requirement since they do not have surplus cash.

D/E ratio is more than 1 and is going to remain at elevated levels, unless we see real repayments with no further addition in debt to fund capex which are not value accretive (both RoE and RoCE have been declining over last two years). Current assets vs. Current Liabilities measured by current ratio has seriously deteriorated over last decade which is at 0.9 times vs. over 2 times before 2 times.

Capex as % of sales is on continuous rise which used to be around 8.6% in FY13 vs. 14% FY17.

Rolling 5-Yr or rolling 3-Yr revenue or profitability is showing declining trend. This also raise flag, if TCPL is going to maintain similar growth in future what they have been doing in the past. One can always argue that incremental growth will be taken care by incremental capex. But past capex has not been able to maintain high growth in sales and profitability and hence future capex cannot be a guarantee that higher growth will be reported in future.

Lastly higher debt repayment and rising interest cost has always put pressure on dividend payout which has declined considerably in last decade for reason 1) to service new capex and 2) to service debt obligations, even though the per share dividend has gone up, which can be a distraction.

Would love if some one has any other views.

You can check the financial performance here:

http://www.morningstar.in/stocks/0p0000brzw/bse-tcpl-packaging-ltd/financials-key-ratios.aspx

1 Like

I can see most people have high D/E as a concern, but the company historically always had a D/E between 1 and 2 for two decades. and has given big returns when it contracted from 2 towards 1. People who applied trading kind of strategy on this stock with entering around D/E ~ 2 and exited around D/E ~ 1 have made great returns. The company has been living riskily for last two decades yet never stumbled. It would be interesting to discuss when they will be able to pull themselve out when D/E reaches 2 or collapse. Now the D/E is on higher side for sure but still safer than before.

Really wondering how fundamental reason fro picking the stock is translating into trading reason. No doubt the company never stumbled over last two decades. But the growth stumbled and the same is a matter of concern. In pursuit of ever rising capex to expand capacity, the growth has been compromised and hence the same should get reflected in valuation as well. Look at what has happened in IT sector, companies in the sector are stumbling with declining growth and hence also the valuation corrected. Here as well in case of TCPL, it is the growth which is compromised over last few years and hence the valuation should also stumble. Going by mean reversion concept, valuation gets aligned to fundamentals when dust settles. I am keeping my fingers crossed. Would love to be proven wrong especially in this case with facts and figures.

1 Like