Another good quarter from TCI XPS: -

Q1 FY23.pdf (2.4 MB)

Qualitative inputs from SMIFS: -

SMIFS Aug 2022 TCI-Express-Ltd.pdf (352.1 KB)

Another good quarter from TCI XPS: -

Q1 FY23.pdf (2.4 MB)

Qualitative inputs from SMIFS: -

SMIFS Aug 2022 TCI-Express-Ltd.pdf (352.1 KB)

Logistics sector at 2 year low. And stockedge is showing logistics with highest delivery. Prospects for TCI express, Blue dart ?

Good information on TCI express here. I am no logistics sector expert but TCI seems like a fundamentally strong company with a vision to expand their operations consistently, adding automated sorting facilities, focusing on a very diversified client base (top 25 clients contribute to only 15 per cent of revenue), government initiative to strengthen logistics sector and focus on infrastructure is a tailwind, targeting rev growth of 15% + while maintaining margins. Only question is what valuation is justified? It is trading at 38 PE now (Blue dart is trading at 48) but is at a 52 week low w.r.t price.

Its a paid article so extracting key info and providing it here:

TCI Express has 82 per cent of revenue coming from Surface express while 18 per cent comes from other services (rail express, Air express, C2C express, Pharma Cold chain express). The company reported highest revenue achieved in any quarter till date in March 2023 quarter. This growth was driven by one, strong demand from SME and corporates, and second, higher utilisation of newly developed sorting facilities. The overall utilisation of FY23 was 84.25 per cent.

The key business drivers for the company are automation of the sorting centres, expansion of branches, having a diversified client base of both corporates and SMEs spread across industries and finally the government initiative to strengthen logistics sector and focus on infrastructure to provide seamless connectivity to remote rural areas.

The new sorting centre at Gurgaon was commissioned in March 2022. This centre is fully automated and one of the largest B2B sorting centres in India. The management will continue to implement the automation strategy in other sorting centres to enhance overall operational efficiency and ultimately to drive profitability further. TCI Express has 28 sorting centres and more than 500 express routes across the country.

The company has been continuously adding branches in order to gain business and increase presence. In 2017, it had around 500 branches across the country, now it has more than 950 branches. In FY23 the company opened 35 new branches. The management expects the new branches, although small, to generate good and profitable business. These branches are useful in adding small and SME customers which bodes well in the overall strategy of the company.

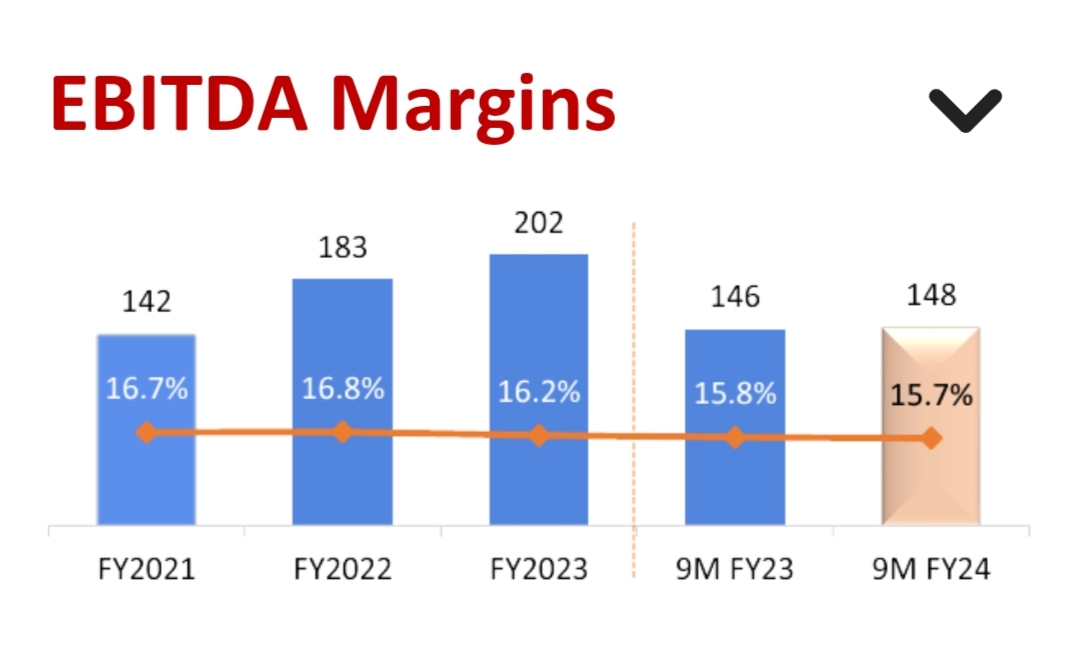

The company has a well-diversified client base of both corporates and SMEs/small customers in the proportion of 50 per cent each. The top 25 clients contribute to only 15 per cent of revenue. Revenue grew 14.7 per cent YoY in FY23 to ₹1,241 crore, EBITDA rose 7.2 per cent YoY to ₹1,95.2 crore in FY23. EBITDA margin during the year was 16.2 per cent against 16.8 per cent in FY22. EPS rose 8.2 per cent to ₹36.2 per share.

The company has given a revenue growth guidance of 15-16 per cent for FY24 and margin expansion of 100 basis points is also targeted. The 100 basis points increase in FY23 could not be achieved as the company did not take a price hike in FY23. However, it has decided to take price hike in FY24.

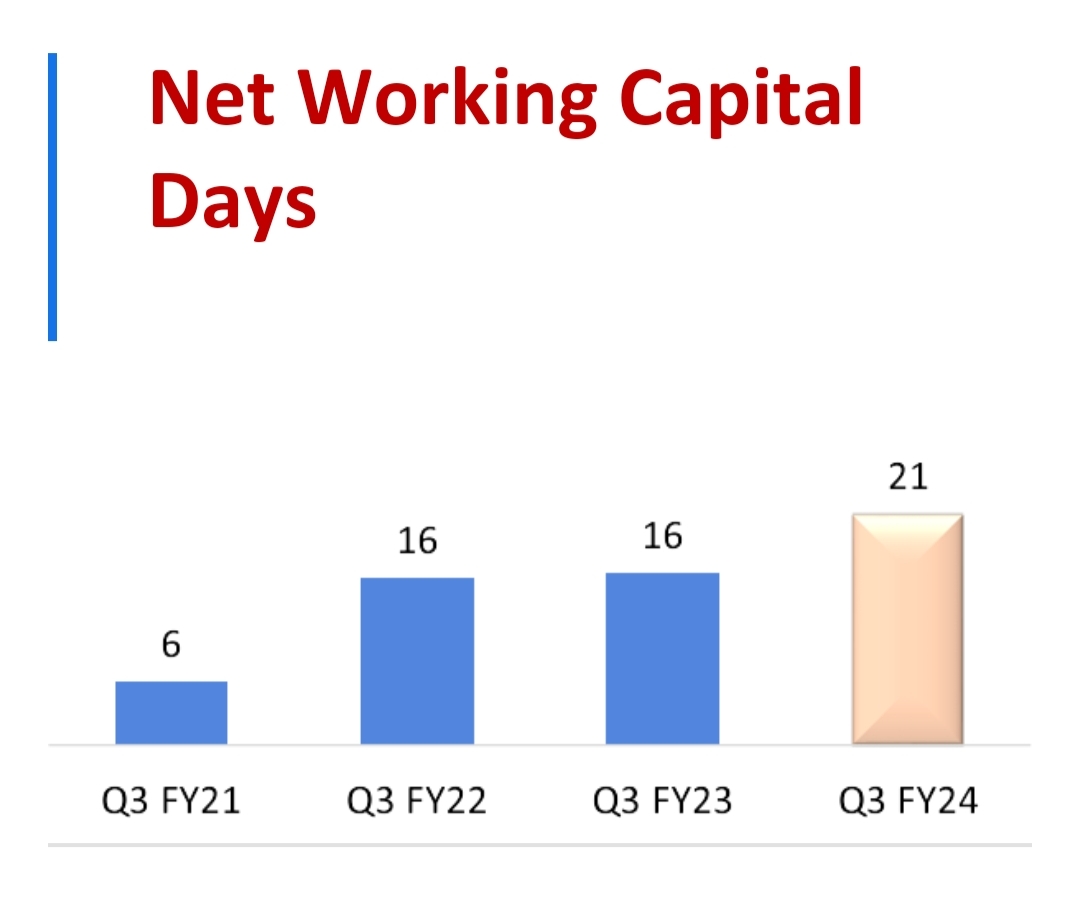

Another flat results with margin slightly going down and net WC days going up.

Management comments :

Pune sorting center is on track for completion by the end of March 2024. This strategic move is expected to significantly reduce downtime, streamlining processes and improve overall operational efficiency.

In short, We may have to wait for more quarters for the stock to move up. Price hikes may not be that easy as competitors like Delhivery is trying to pass on benefits to customers in the form of discounts as they scale their operations. Delhivery posted their first profit with 5000 cr in their balance sheet.

Tci express declared 3 rs per share as second interim dividend

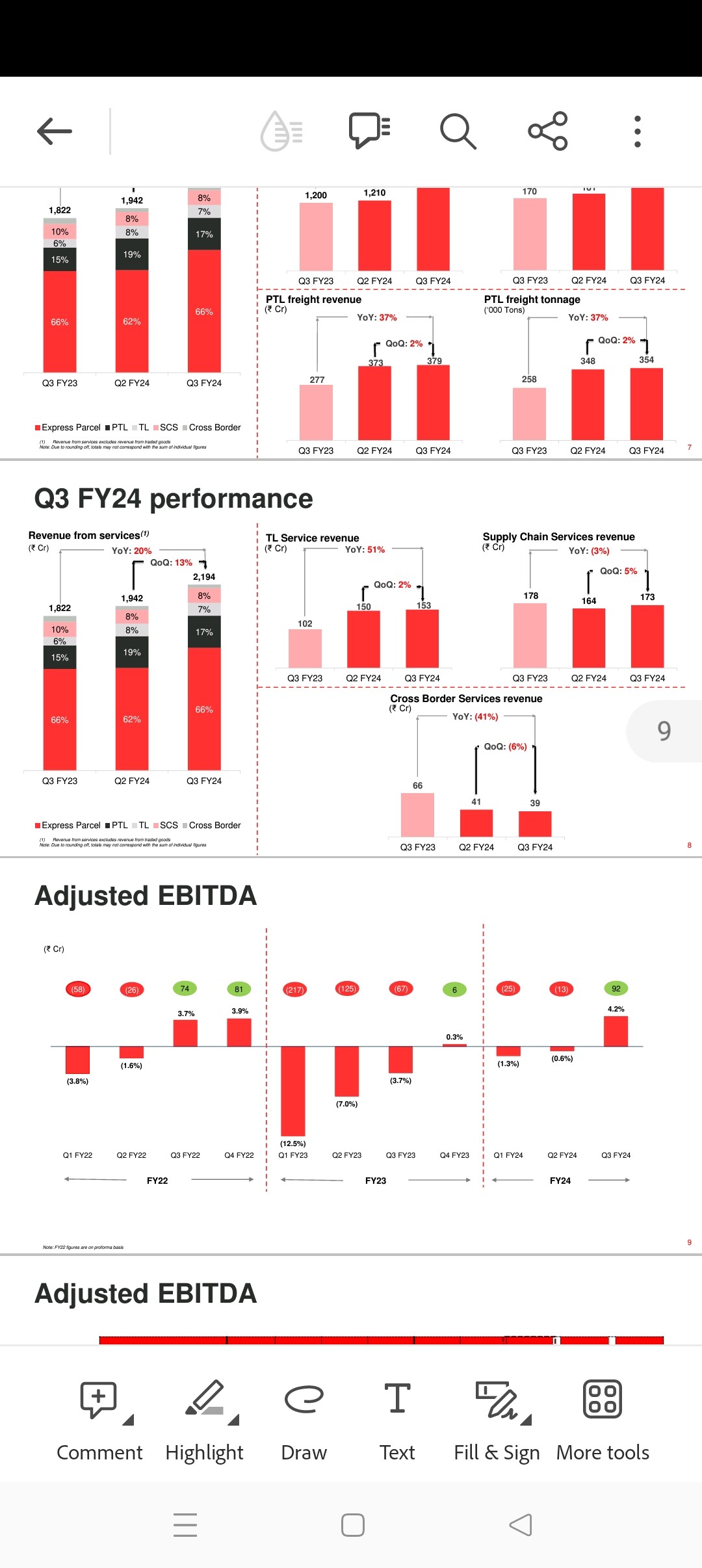

Source for the snaps :q3 fy24 investor presentation.

Disclosure : Invested

Thanks for sharing. Are’nt TCI Express and Delhivery’s customer base different? Correct me if I am wrong - TCI Express is more B to B and Delhivery B to C. TCI Express with its sticky customer base and per mgt commentary post Q2 results, margins were to improve in the second half year from the achieved margins of 15.8% in Q2. Mr. Agarwal further mentioned that Q3 and Q4 FY2024, will have higher growth and committed volumes would be achieved. The Margins and revenues though seemed to be flat in Q3.

Again during Q2 concalls - festive season and resilient domestic demand were expected to be favorable for Q3 results due to higher utilization but the mgt perspective post Q3 results mention of continued headwinds on account of muted festive demand and long holiday season during the quarter. Mgt in its Q2 con call did not acknowledge the heightened competition in the industry as a bearing on its results. Revenue and volume guidance for FY 24 from prior concalls were to be 14 to 15% and 13% on volume. This would mean a last qtr revenue of approx 485 crores to stick to their guidance. Not sure if this is possible from its current quarterly average.

Clear case of mgt over promising and under delivering. Hope to see some expected gains in margins due to the Pune automation center.

Disclosure: Invested from slightly higher levels.

They have been consistently under delivering after overpromising over the last few quarters. I feel the management tries to sugar coat instead of conveying challenges and measures being taken to address them. I would have expected them to grow at GDP+5%, but they are unable to do so. I had entered at much lower levels and exited today after seeing multiple quarters of business underperformance.

I believe it’s more of an industry issue. All the logisitcs companies (VRL, Navkar, Allcargo, Mahindra Logistics etc) have come up with bad numbers, much worse than TCI express. But I can’t figure out what and where the issue is in indian logistics industry. I thought with uptick in economic activity, logistics sector should have a natural tailwind.

Hi @banjobaj,

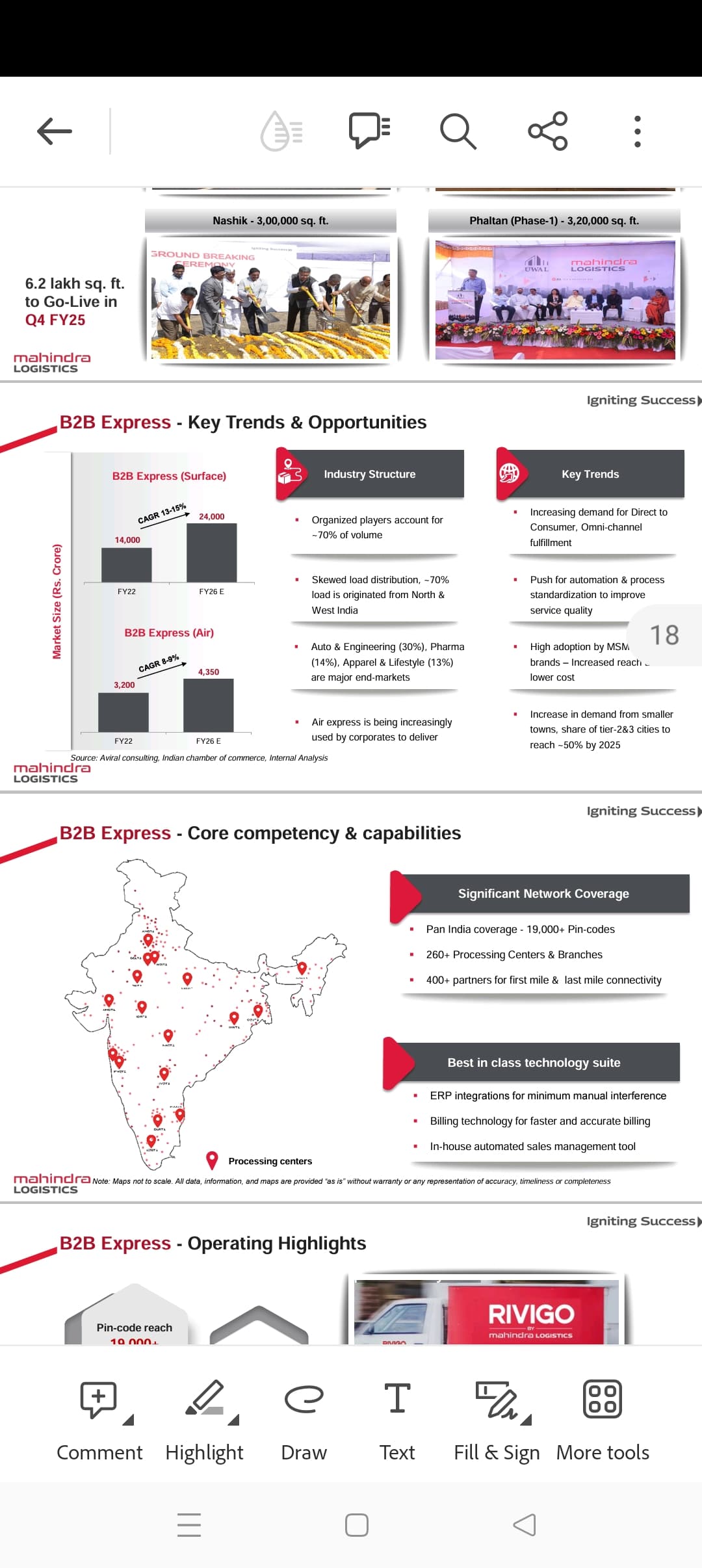

Delhivery’s part truckload (PTL) segment is the one into B-B express which has grown from 273 cr to 373 cr y-y in their q3 this year which is 17% of their revenue. (Check the screenshot-1 from their q3 presentation)Mahindra logistics also has B-B express (from Rivgo ). Both of them have aggressive expansion plans like our TCI express capex plan of 500 crores for fy-23 to 28. Please check this delhivery interview in CNBC for quick reference.https://youtu.be/MKDFzktOLP8?si=xNMAuyFl_oqZ58Nt

Delhivery is putting in 7% of their revenue as capex until Fy27 and 4% later on, with focus in PTL segment as that is the bigger opportunity. I am attaching here yearly growth guidance in Mahindra for their B-B express for your reference.

Overall PTL B-B express works like a niche space where service differentiation like delivery speed, service quality etc let the players enjoy a premium pricing than regular . Service offerings mix also varies among different players.New service offerings such as rail express, pharma cold chain express in TCI express is expected to grow faster. Business models also varies like PTL in Delhivery doesnt follow traditional hub and spoke, bit something different called Mesh. TCI is the most asset light one in my understanding as they dont own trucks. Competition is expected to intensify with aggressive capex plans to grab market share from unorganized and many of the peers will enjoy economies of scale and operational efficiency etc in coming years.The main worry for me is as with TCI express 's adamant stance on not giving away a bit of margin, will they be left far behind.?Delihivery reporting their first PAT was a surprise for me last quarter.

Those with deeper industry knowledge can comment better in comparing competitive advantages and who could potentially gain the most in coming years.

Comparison given by @Pchandrapal is the right comparison (apple to apple) among the logistic players.

Delhivery management seems determined to improve their share in standard PTL space. They intend to stay the least cost operator by absorbing the impact of general inflation, leveraging the exceptional incremental gross margin of the network.

Thanks - extremely useful. Was talking to someone in the industry and his view was that Delhivery’s aggressive pricing strategy to grab mkt share may face profitability challenges going forward in a highly competitive environment. Maybe - this makes sense for TCI Express to not dilute its margins. One stat that would be interested to track though (although TCI Express just talks only about volumes, revenue and margins) is the gain/loss of B2B customers.