excerpt from the disclosure submitted to the exchanges.

However, in spite of making continuous efforts, the profitability of the Company is affected due to lower revenue. reported during the quarter 1. At this moment, we anticipate that Covid-19 could have an impact on the Company’s performance at least in first quarter of financial year 2020-21.

There was hardly any business for the month of April 2020. Even for the month of May 2020, the business volume was very low. Though, the Company’s liquidity position was strong. The Company reported surplus fund of Rs41 Crores alongwith unutilized cash credit limit of Rs45 Crores as on March 31, 2020.

The Company does not have any outstanding loans and hence do not envisage any default in debt repayment. We are in well position to manage our cash flow and to meet financial commitments timely.

Further, the Managing Director has voluntarily opted to forego his salary for the period of 3 Months to mitigate the financial impact from the disruption caused by the ongoing Covid-19 pandemic, however, the Company ensured that the employees emoluments have been paid in full alongwith related statutory payments such as PF,ESIetc. in a timely manner.

Notes from AR 2020

Company Introduction:

-

Company is express logistic provider which provides fast, reliable, on demand, integrated, door to door movement of shipments

-

Came in existence through demerger of TCI XPS from transport corporation of India limited.

-

Provides integrated logistics solutions to customers covering 708 districts, 800 branches, 28 sorting centers, 40000+ pickup and delivery points, 500 express routes, 2500 feeder routes and 5000+ containerized vehicles

-

Hub and spoke distribution model

-

Services offered are domestic surface express, domestic air express, international air express, reverse express and e-commerce express

-

Present in sectors like automotive, pharma, IT hardware, textile, retail and e-commerce

-

Technology involves barcoding and RFID, hand held transmission, app-based service offering and GPS enabled vehicles

-

Diversified customer base across corporates and SMEs with none of customers contributing more than 3% of receivables

-

Asset light business model with strong balance sheet (does not own any vehicles)

-

Revenue up from Rs 663 crore to Rs 1036 crore in 5 years and PAT up from Rs 28 crore to Rs 90 crore in 5 years with PAT margin improving from 4.29% to 8.6%

-

Return on capital consistently around 40%

Key business updates and annual review:

-

Business process includes collection, transportation and distribution. Collection includes shipper, pick up, warehousing, collection.

-

3.5 lakh square feet of new sorting capacity added in Gurgaon and Pune

-

Company moved towards 100% paperless supply chain bringing in more efficiency

-

Implemented centralized vendor management system

-

Company has been recognized as a “Great place to work”

-

70 new branches opened in 2019-20

-

Digital booking replaced manual booking

Financial Performance:

-

Topline growth of 0.8% YoY at Rs 1033 crore sales and Rs 89 crore PAT growth at 22% YoY

-

Stable margin profile is attributed to higher capacity utilization, operational efficiency and efficient working capital management

-

Rs 80 crore of cashflow from operations generated and Rs 32 crore of capex deployed towards increasing automation and adding more sorting centers

-

Rs 4 rs per share of dividend to be given

-

Employee cost increased by 10% to attract top talent and retain existing performers

-

Despite of high growth in salary expense, company could maintain margins by effective control on other operating expenses

Market Trends:

-

Technology adoption is likely to create and accelerate new opportunities in transportation, warehousing and freight forwarding segments

-

Logistic sector is expected to grow at 10% CAGR in next 5 years which is currently at $215 billion industry

-

Indian express logistics industry is 2% of worldwide express logistic industry and expected to grow at 17% till 2023

-

Challenges are lack of infrastructure, integrated logistic network, slow adoption of technology and lack of skilled man power

-

Currently, logistic cost is 13-14% of GDP which is high relative to 8-10% in advance economies

-

National logistic policy and multimodal logistic park policy to fuel growth in long term

-

In 2019, air cargo traffic turned negative for the first time since 2012 with 3.3% decline which is steepest since 2009

Guidance:

-

Will continue to occur meaningful capital expenditure towards sorting centers to drive operational efficiencies and reduce turnaround time

-

FY20-21, at least Q1 is going to be impacted due to covid

Other Points:

-

67% shares held by promoter, 6.7% by MFIs, 2.7% by FPIs and 15% by retail. MFIs share increased from 3.1% to 6.7% where as FPIs and retail reduced.

-

Management remuneration has good share of variable commission though remuneration is on the high side being 11%

-

15.5% employee salary growth, 17.6% managerial salary growth

-

Total 2905 employees

-

Company maintains good risk management practices by identifying receivables in various risk buckets and negligible amount in moderate risk bucket

-

No single customer accounted for more than 3% of receivables

Risks and Open Questions:

-

Why cash balance is low if company has been good cash profit generator. Need to study historical cash utilization of company

-

Freight expense constitutes 70% of expense and it is very important to have control over this cost to maintain margins

-

Rent is other higher cost item apart from freight and employee expenses

Thankx

any update on impact of Covid

Q1 earnings released. Slightly disappointed with the numbers as EPS is almost NIL as I was of the impression that the logistics sector was not impacted too much due to COVID. Apart from client concentration risk which TCI has addressed, industry concentration risk is another important factor that must be addressed soon to avoid negative surprises in the future.

Disclosure: No holdings as valuations are expensive

Having tracked this company for a good time now, one thing that i have learned is that the management’s guidance is always on the higher end- atleast in case of topline growth. They have always missed topline growth guidance. Here the play is only on the margins improvement, something which management has been delivering on.

One should not expect some high revenue growth here, without growth in economy.

Has the company taken advantag of video AGM? Can someone who attended the AGM enlighten us? MD’s remuneration stands at 7.7cr as against Net Profit of 72cr which is 10.69%. Attached is snap from FY20 Annual Report

The management remuneration has always been high here if one looks in terms of % of profits.

But one also has to consider that if someone is running a company with a topline of ~1000 crores, a salary of Rs10 crores is not a big deal.

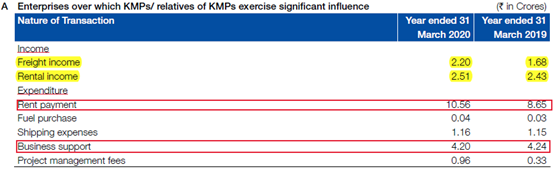

The point here is that Companies has defined a certain % of profits as remuneration. The current remuneration is double of the ceiling limit which has gotten approval through special resolution. Besides, 30% of Co.'s rent expenses are going to related parties (The names of the parties not disclosed) and another 5-6% of profits is being paid to related parties as ‘business support’

You are right. There are many drivers which can result into operating leverage to play and can create margin expansion.

-

Realisation/kg is increasing vs. overall transportation cost/kg remaining broadly flat

-

Efficiency from capex on sorting centres is good enabler

-

Recent regulations around tonnage capacity (due to fleet height) boosts some more tonnage to be carried

-

Feeder network is another trigger in this direction

Also, company is putting efforts in right direction for scaling the business as an asset light platform - investing on sorting centres, branch expansion, customer service and technology efficiency.

The overall business model helps in maintaining cost structure in such bad phase (like Covid) and at the same time expand rapidly when needed.

While other peers are bleeding with debt or high working capital requirement, TCI Express enjoys almost debt free status thanks to it’s asset light model.

Ofcourse competition from PE/VC funded startups and slump in overall business environment is key risk.

Disclosure: Tracking. Only for educational purpose, please do your own due diligence.

Regulation changes around the tonnage capacity will most likely not affect them, because the entire fleet is containerized, so the capacity of the vehicles would most likely be constant.

The play here is entirely on managing better utilization of fleet capacity, as the cost is on per kilometer basis, irrespective of full load or half load. Management has stressed that the reason for having a split of 50:50 between large customers and SME customers is to manage the fleet usage. SME customers give good pricing, while large customers gives good volumes- which helps in managing the utilization levels.

Thanks Ankush. Interesting point.

Interesting pointers from recent credit rating report.

https://www.icra.in/Rationale/ShowRationaleReport/?Id=99379

Company on track for it’s upcoming capex plans. This will be mainly into company owned and operated sorting centers. This will be funded internally and almost ~90% of yearly operating cashflows will be reinvested back into the business (of course the RoIC will be very high due to asset light nature of the business model).

Thanks for sharing Mr Vivek. Useful info and it is timely. thanks

Have gone through the thread and basic fundamental analysis (yet to go through AR). I had two doubts:

- The MD seems like a clown . Printing his own interviews and his whole compensation saga. He seems like a person not to be taken seriously although his business has been quite successful. ( I don’t trust his actions of foregoing 3 months salary because I believe he will recover it later ).

- Huge risks due to startups like Delhivery, Blackbuck etc. They receive huge…huge… PE fundings . As we have seen these kinds of funds can significantly send any business to the top . Will this impact TCI express’s business in the long term ?

Views invited.

Disc: Not invested

TCI Express is avoiding online retail delivery , sounds diffrent segments.

I have flagged the Related party transactions and the blatant circumventing of the Companies Act ceiling limit regarding Promoter Salaries. No one here seems to be even slightly bothered about it.

As for startups, yes the threat is there. But currently the startups are focusing on B2C and C2C business, a space which TCI Exp has smartly stayed out of. 50% of its business is contract business from established clientele. Remaining 50% is MSME where you could probably be right in assuming a threat to its business.

You are wrong no one is bothered about it ![]() , that is the first thing i check

, that is the first thing i check ![]()

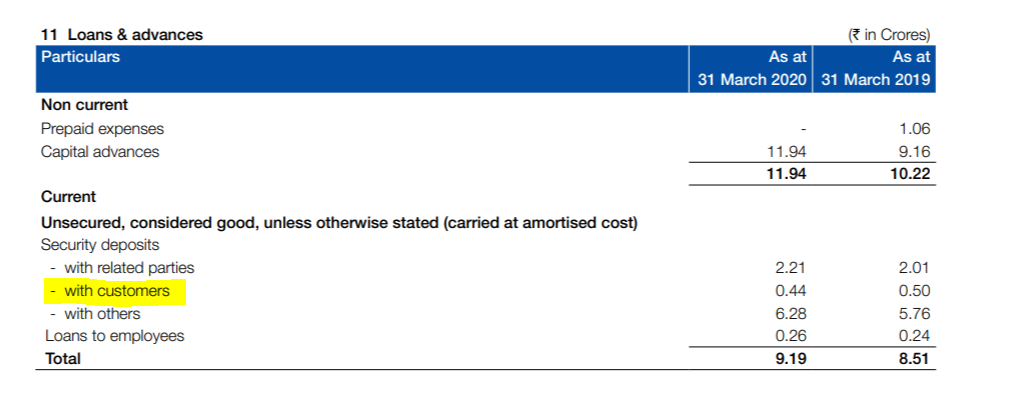

here is another red flag from AR

Growing loan to customers is strange who these customers are ?

Bhavesh,

These are just short term advances to various stakeholders. And almost negligible in quantum for company with balance sheet size of 450+ crores in my personal view.