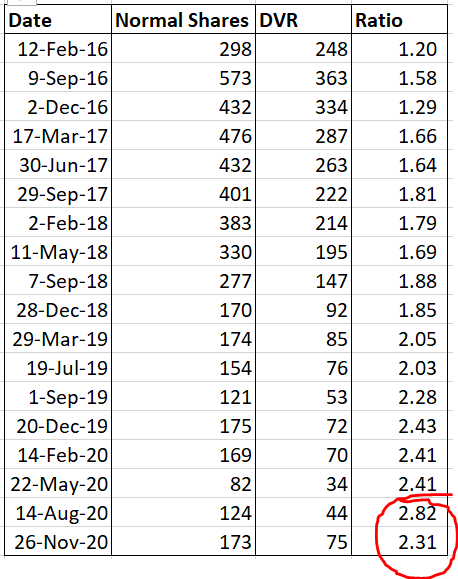

Looks like something interesting is happening here - for the first time in the last 5 years I have noticed the ratio between Tata Motors Normal Shares and DVR converging at a rate faster than ever before - this looks like a clear trend reversal and the velocity of convergence is likely to get accelerated as we move along - see the chart below :

Disclosure: The data above is purely out of academic interest (used random dates and you can do your own research to see if the study holds good) and i have holding in Tata Motors DVR.

Thanks for this data - I dug a little deeper, and the long term average since 2009 is around 1.68. The median is also close to 1.70, this means there is a change of further convergence and a potential arbitrage opportunity. That however hinges on two factors:

Promoter group buying. If you notice the promoter holding in DVR, it went up from 5.3% to 7.24% in September 2020.

Return of dividends. Till dividends were paid, the average ratio of regular share prive to DVR share price was even lower at 1.3.

We really don’t know the debt covenants agreed with the bankers for JLR - the profitability of JLR holds the key for dividends. While Indian PV segment was burning cash over the years, its very likely that this turns profitable by end of this fiscal and be a cash accretive business going forward.

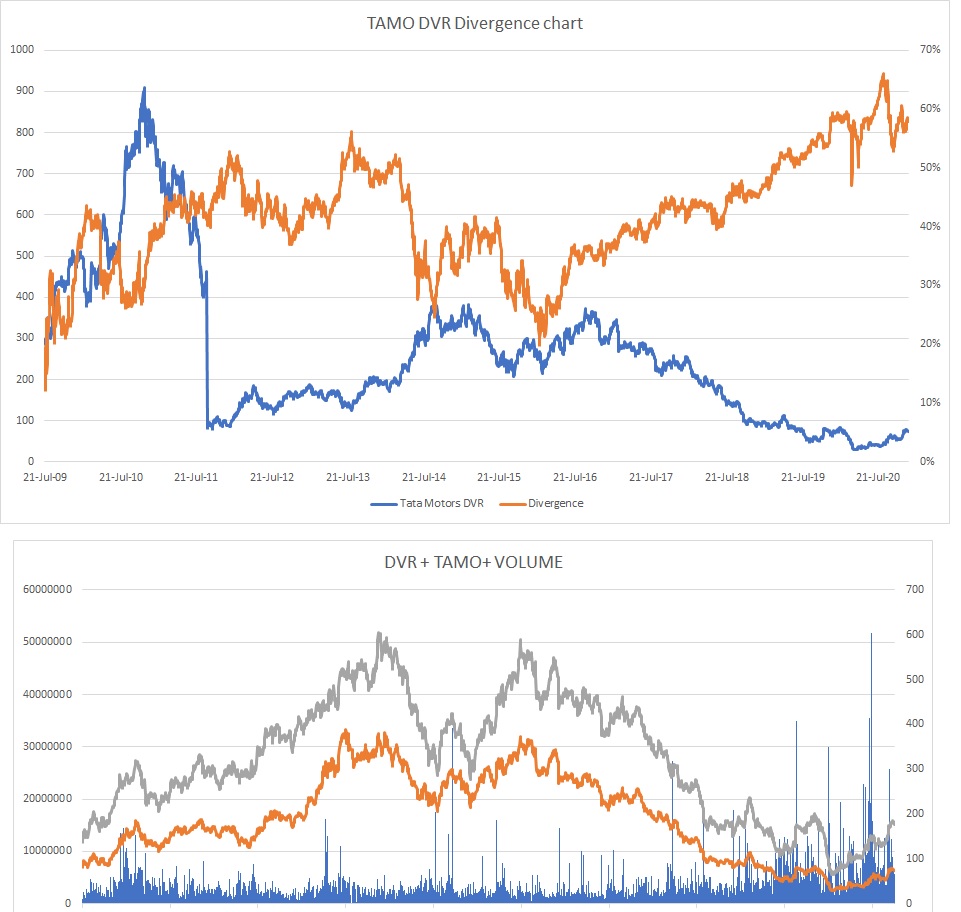

I have plotted the long term DVR and TAMO price/ volume and divergence. Please refer image below. Except for event driven convergence when bulk/ block deals have happened on the DVR. It seems the divergence has been high and rising. Most of the convergence in the stock happened from March to Sep 2020 when Tata Sons increased its stake. However, there has been no more buying since September. Also, some big institutional investors seem to have exited DVR in the period and retail holding has risen.

How is the deleveraging story in TAMO expected to play out. Are cash flows truly sufficient to reduce leverage to NIL from 110000 cr in 3 years? Or should we expect sale of some business.

Are the current in India numbers a result of pent up demand or a secular change in past trends?

How is the China JLR business expected to fare, given the India - China tensions

Lastly, where would DVR lie within Tata Sons priority list, presuming resource requirements to pay off the Mistry family, increasing stake in voting shares in group companies and deleveraging effort all across the group? Does the group have enough resources for all the demands to continue increasing the stake in DVR.?

Thanks. Looking forward to building a fundamental view over the chart.

Tata Motors offers its third VRS scheme in four years as part of its ongoing cost restructuring exercise Tata Motors, India’s largest automobile company in terms of revenues on Friday offered a voluntary retirement scheme to its employees across offices and factories in an effort to further reduce costs and consolidate gains accruing from its four-year running turnaround plan. The VRS scheme will be the third round of VRS offered by the company in four years.

Tata motors said sales in China were up 19.1% on the year and up 20.2% sequentially.said that 53% of its retail sales for the quarter were of electrified vehicles, lifting the share of electrification to 43.3% of total sales for 2020.

Tata Motors - successful turnaround visible happening

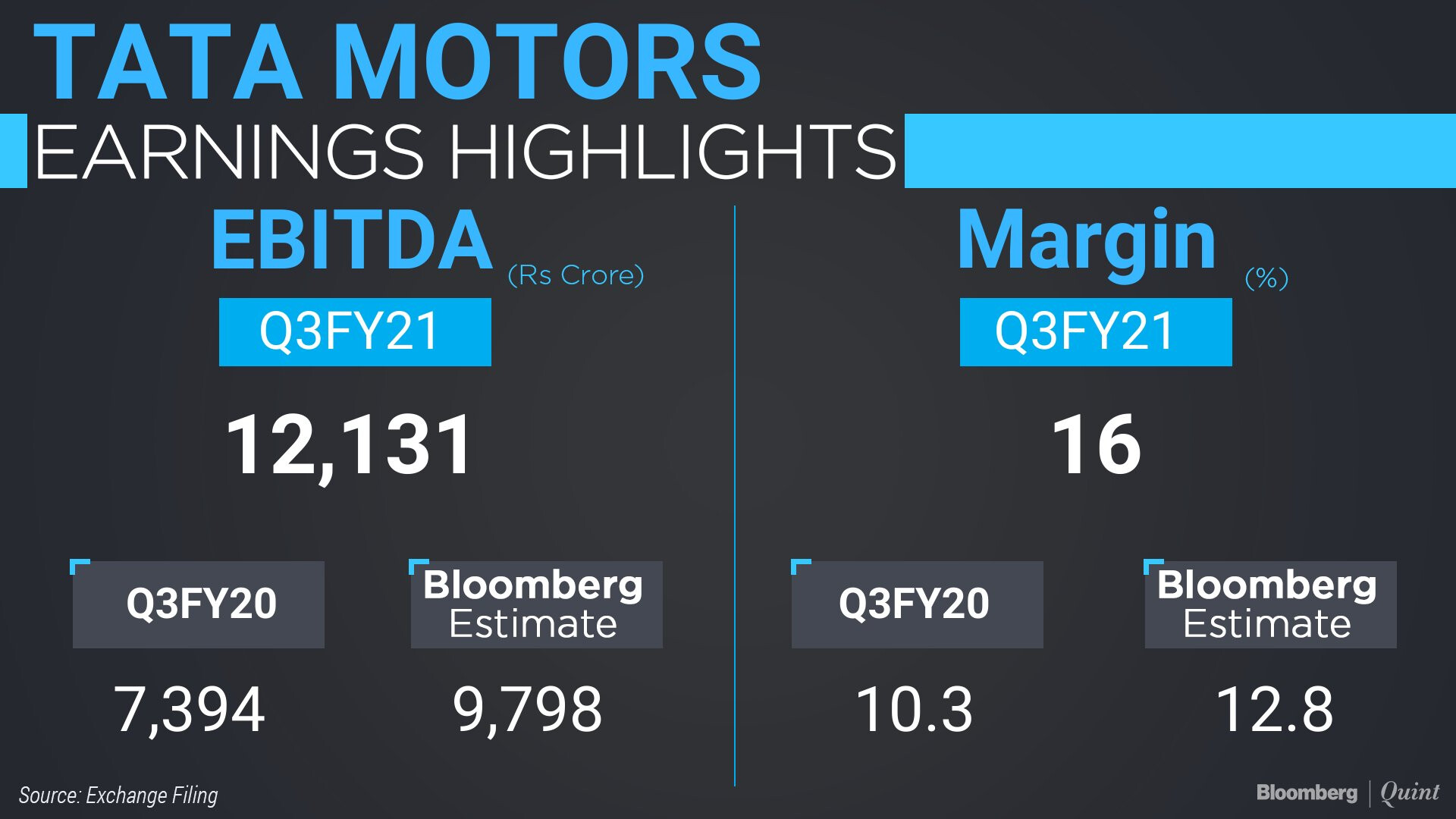

Q3 results are heartening and confirming the journey towards overall profitable operations. Few points to be highlighted -

Revenue recovery to pre-covid level and exepcted to gain more

EBIDTA margin improvement is heartening and good to see it at 14.8%. Charge+ good results

BREXIT hangover is behind now with fair deal

Reduced “Pure Diesel” vehicle share in revenue is remarkable thing to seee as it was going-concern - JLR its at 16% and TaMo (PV) at 17%

53% of overall JLR sales is EV (BEV + Hybrid EV)

Manageable debt levels and improvement expected with increasing positive FCF

Increasing market share for TaMo PV in India and expect to contribute more in overall revenue. Both JLR and TaMo looks well placed with new launches. CV sales expected to pickup for TaMo now with economy receovering - particularly I am more hopeful on electric buses going further

Increasing parents (Tata Sons) ownership shall bode well in decision making further and I look it positive that parents has used market turmoil opportunity to increase thier share into company. Overall Remarks - Q3 results confirms journey towards profiateble operations from loss making history. Disclosure: Invested 20% of portfolio around 140 levels. Views may be baised. Contra opinions welcome.

“Tata Motors is seeking shareholder approval to transfer its PV business to TML Business Analytics Services, which would be later renamed to Tata Motors Passenger Vehicles (TMPVL), subject to regulatory approvals. The net worth of TMPVL, where Tata Motors will hold nearly 100 percent shares after the hive off, will stand reduced to Rs 8,589 crore.”

How do we understand what it means for the company? I am interested in PV segment because it would retain the EV segment of vehicles as well.

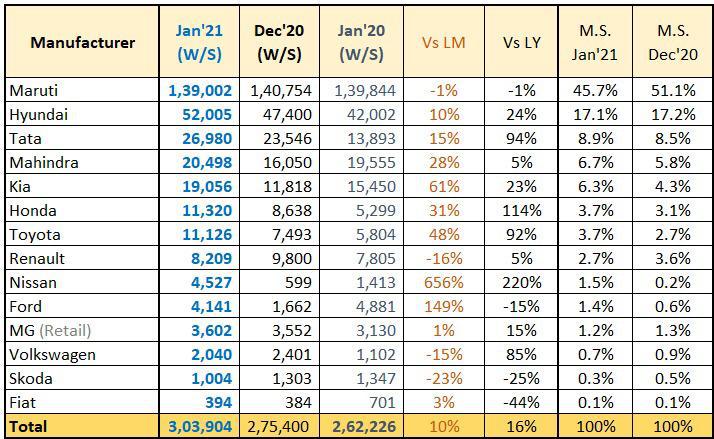

Brilliant Set of Numbers by Tata motors in March. Wondering why did the share price not react to it. I believe that the market had already priced the sales number in the stock. I have attached the BSE link below.

The Promoters are consistently increasing their share below are the figures for June - Sep & Dec.

Any one tracking figures in last 3-4 years in a excel or PDF so that the current figures can be compared with March 19 and March 18 figures as well. Or is there a site which gives ready reference.

Attached company update on the Q4FY21 TaMo wholesale update.pdf (457.2 KB) global wholesale number. 43% higher unit sales is heartening number to see. While any auto company in India is enjoying Mcap to sales ratio of over 1, TaMo is still lagging behind below 0.5. Maruti has 2.5, Ashok leyland 1.5 and M&M above 1. Considering reducing debt levels, overall profitable operations and quite larger and deiversified (PV, CV and EV) play coupled with strong growth numbers I assume minimum 100% upside for stock price to come to normal level of comparison with peers. Some triggers like demerger of domestic PV business hopefully will add to this vlaue unloacking.

JLR FY22 outlook: Volume growth is expected to be over 20%. EBIT target of 4% is on the conservative side owing to volume uncertainty, led by the semiconductor shortage. It expects to break even at the FCF level post investment of GBP2.5b and restructuring costs of GBP0.5b. EBIT may be negative in 1QFY22 due to the impact of weaker volumes on account of the semiconductor shortage.

JLR has an order book of ~0.1m units (~60% of orders are from Europe and the UK). Defender’s order book stands at over 22,000 units. PHEVs have a very high waiting period of up to 12 months.

Volumes in India in 1QFY22 TD have been severely impacted by the lockdown as almost 80% of dealerships are shut. Sales in Apr’21 fell ~50% and is worse in May’21. It is targeting an EBIT margin of over 2.5%, with positive free cash flow in FY22.

Fund raising was more of an enabling resolution across instruments, keeping in mind the second COVID wave. Raising funds via the equity route remains the last option for the company. The board has deferred the fund raising decision to the next meeting (AGM).