I had done similar work on the price discount between the two. My figures are different as I am calculating how much is the ORG premium over DVR.

Price and Difference Chart since FY09.

Here are the averages of the quartiles in which this difference has historically traded. The current difference is amongst the highest ever.

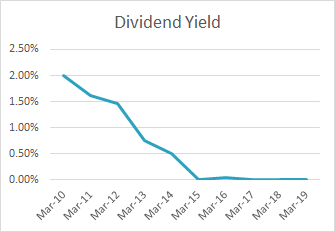

The relationship deteriorated somewhere in FY16 when the dividend policy changed.

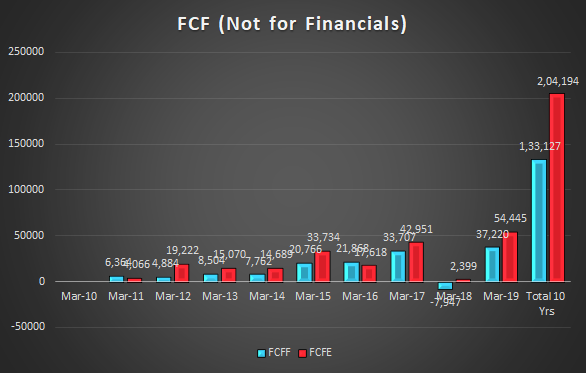

Surprisingly, the PAT & CFO were still positive until recently. Management foresaw the need to cut the dividend with an increase in capital intensity.

I am guessing that the premium/discount/divergence won’t completely vanish until all the parameters of CFO, PAT, FCF and dividend not only show an uptrend but also stabilize. Unfortunately, with the investments needed in the coming decade for EVs, the probability of this happening is low. They could surprise with streamlining the operations, adding efficiencies but it will be a slow change.

Also, interesting to see that from the recent Sep-19 lows the ORG outperformed the DVR in the up move. As long as such sentiment-based moves keep occurring without actual improvement in fundamentals, it is better to play with the ORG than DVR.

Yes, the divergence between the two is amongst the highest ever, and I myself had thought of playing arbitrage between the two when the divergence as per my numbers had crossed 100% back in Feb-19. Unfortunately, such arbitrage trades do not work in stocks with such volatile fundamentals.

So yeah, play the sentiment trade carefully. If fundamentals improve the DVR will be the winner, if they don’t, things could stay status quo, if they deteriorate, the DVR could hurt you more.