Great summation and good conclusions…

One conclusion, then operating margin will be lower than 24%. To make 25% , it has depend on Other Incomes including Forex Gain then…that Mr. Dave clearly mentioned also…

Great summation and good conclusions…

One conclusion, then operating margin will be lower than 24%. To make 25% , it has depend on Other Incomes including Forex Gain then…that Mr. Dave clearly mentioned also…

Don’t listen to MOSL (as per them this company is a potential 100 bagger  ) or any other brokerage on price targets. Do your own research and analysis on the stock price (read valuation) and prospects of the company. Brokerages change their opinion in a heartbeat. They will lead you to ruin if you blindly follow them.

) or any other brokerage on price targets. Do your own research and analysis on the stock price (read valuation) and prospects of the company. Brokerages change their opinion in a heartbeat. They will lead you to ruin if you blindly follow them.

I haven’t heard the con-call for the 3rd quarter yet, though having heard con-calls previously, I don’t think anything would have changed drastically in a matter of months. If it helps you can refer to notes put by other boarders above. You’d get a sense of where the company is heading.

Disc: Invested and increasing exposure.

Can anyone throw some light on effect of Tata motors performance on Tata elxsi sales and profits? How much percent of revenue is coming from JLR ?

Around 25% of the Elxsi revenue was from JLR last year, this figure was said to be around 20% in the latest quarter. In the past, management has said that Elxsi’s business depends in JLR’s R & D budget and not on sales. So if JLR is not growing, no problem. In fact, the pressure to R & D more will be higher. But take it with a pinch of salt. I think there will be an adverse impact to the extent that there are overall cost cuts, as we saw in the most recent quarter. In the long run, it will reduce the JLR overhang on company which is not a bad thing.

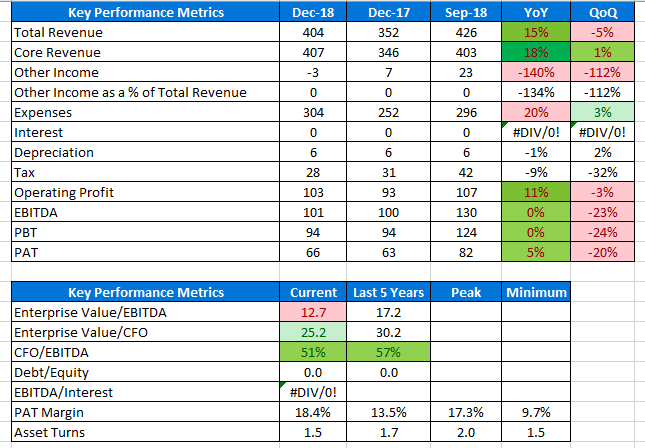

Q3’FY19 Results: Revenue growth was decent. However, two factors as per con call led to a very ordinary result from profit perspective:

Overall, nothing major in con calls and the theme on electronification and autonomization of automotive sector, the design and electronification of OTT in M&E sector continues with healthcare and license revenues yet to be significant. One major point was new focus on long term deals. Contribution of Tata Motors has come down to 20%. Below are some of key points from concall:

No. of working days fewer and billing losses

Exchange rate losses

Automated testing opportunities from OEMs for various automnomous driving car scenarios

Deal pipeline in auto looks good

Lot of traction in chinese market in auto segment but no breakthrough yet. One of largest auto market and expecting opportunities to come

Non-linear revenue is still less than 5%

Two parts to automnomi: Algo which goes inside autonomous cars and validation peace for testing autonomous cars

Opportunity in validation side is higher and there was an announcement with Hyundai

Current hiring ios not yet contributing to revenue and ideally takes 6 months to contribute to revenue. Will be hiring more fresh gradualtes as skills required in cutrrent market are evolving and changing.

Next year fresher hiring headcount is 800 and lateral hiring is as per requirement

26 crore swing between last quarter and this quarter due to currency flctuation

Focusing on long term deals where management has identified key accounts and a personal is dedicated to drive the whole program with a goal to convert projects into long term deals and initial feeds are positive

Disc: Had exited in June’18 but took an entry recently at 950 Rs with 2% allocation. Still, valuations look bit on higher side to take a higher position

Any Idea how No deal in Brexit can effect this company or Entire Brexit Scenario?

Things which are not in our hand and even people running businesses and country do not know which way it will go, what would be quantification of cross impacts, no point spending time on that. Still, if any such event takes away piece of mind, I try either to balance that risk through margin of safety or through capital allocation else I just stay away for peace of mind. So, beyond my capability friend and it does not take my peace of mind

just wanted your thoughts on how tata elxsi and LTTS compare, went through their concalls, looks like similar line of work, however LLTS does not seem to be in broadcasting. LTTS seems to be valued more expensively and more eager to grow. Tata Elxsi has a stated aim to grow @ 20%, however a rough calculation assuming they achieve 15% growth over a period of 10 years ,gives me an approx value of 850. Something below that will give comfort for all the uncertainties related to JLR/Brexit.

Frankly, never studied LTTS. However, I remember 2 years back when perception of IT was in doldrums, was exploring these businesses and there was a PE investment done in Tata technologies (unlisted arm of Tata in similar line of business as LTTS) and based on that valuation , LTTS looked quite attractive. However, I think in last 2 years, prices have run a lot. Without reading in detail about LTTS, making any comments won’t add value and only the above info I could add which may help. Regarding , Tata Elxsi valuation, I consider valuation as a range and like to build a staggered position rather than one time (only when either it is at lower band of valuation or have super high conviction or it is decided that will take a very long term position which is again rare in my case). So, currently having a 2% position is agreement to your views. I also don’t find valuation wise that attractive to take bigger plunge. The reason being following:

All said and done, I am more lover of valuations than lover of stock and in past also have made entry as well as exit within 2 year time frame due to under and over valuation (suits my process) and won’t mind repeating based on which side it moves. For next 2 years , key things to watch are

We would like to know about your process of finding undervalued, if u can tell. I had found Tata elxsi to be undervalued at around 1000 considering its yoy growth and numbers. However, it is still expensive as per lot of experts. Hence, your views would help me calibrate valuation in next bet. Thanks

I would just add my thoughts on valuation which is a very rough estimate, @suru27 can add his and you can also pitch in, will help in valuing companies and finding a sweet spot range to buy, i sort of ranged on tata elxsi, based on screener algo for coffee can and finding tata elxsi in the first quadrant for last few years in the freefincal algo. Used the FCF from the freefincal and compounded it for 10 years at 15% and then assume it is sold for 15 times cash flow( this approx comes to 5% perpetual growth). Use npv function @12% to reach the approx value. For a technology company projections further than 10 years would be fraught with risk and even 10 years would there is risk of obsolescence. I feel that’s why a few FMCG companies quote at valuations you cannot reach with any excel model based on historical growth, They quote only for the certainty.

s

In this note, an attempt is made to value Tata Elxsi.

The current valuation as per market is as follows:

| CMP as on 10-Feb-2019 | 904.50 |

|---|---|

| No. of shares (crores) | 6.22764 |

| Market Capitalization (Rs. Crores) | 5,632.90 |

| Free cash as of 30-Sep-2019 (Rs. Crores) | 407.28 |

| Value (Rs. Crores) | 5,225.62 |

The current P/E ratio is 19.49 and Price to Sales is 3.49.

Background:

Though the company operates in the fast changing software sector, the business has not changed much over the years. Even in 2005, company talked about revenues coming from areas such as industrial design, visual computing labs, automotive systems, embedded systems, multimedia etc. – broadly the same areas it operates today. Therefore it is assumed that past numbers can be used as a reasonable basis for valuation. There is no estimate on the size of the opportunity (huge) or company’s market share (miniscule).

Since we are already in February, I have used TTM 12M numbers of revenue and profits for full year FY18-19 and made some estimates for cash flow based on past trends since cash flow statement for the current year is not available. Essentially, I am assuming a YoY flat Q4 FY19. This factors in near term headwinds. I think this is a better approach than using data only upto March 2018 for the analysis.

Based on data from 2004-05 to date, the company has delivered following growth rates on various parameters:

| Parameter | CAGR |

|---|---|

| Revenue from Operations | 16.71% |

| PBT | 15.00% |

| PAT | 18.68% |

| CFO | 12.41% |

| Book Value | 22.30% |

During the period under study, revenue growth was consistent but profitability remained fluctuating and elusive till FY2013. For example, PAT in FY2013 was lower than PAT in FY2005 and PBT was almost the same. From FY2014 onwards however, company has taken off strongly on all parameters with more than 30% CAGR in profits.

Margins have remained constant with employee costs as the primary expense head taking up around 50% of revenues throughout the period under study.

In the last 3 years, cash flows have deteriorated a bit with more and more cash locked up in working capital and tax incidence has gone up. It seems company was benefiting from some tax benefits earlier which have expired from FY2016 onwards.

Cash Flow from Operations now hovers around 80% of PAT for the last 3 years. I have assumed this same ratio for FY2019 as well. Capex demands have been minimal throughout, averaging around Rs.25 crore per year.

With the above background, let us now turn to the valuation exercise.

I have done valuation under two scenarios – “normal” scenario and an “ex-JLR”. This latter scenario is a worst case scenario where the company loses entire JLR business, currently 20% of revenues.

I have assumed a 10-year growth phase and after that a perpetuity phase. In the perpetuity phase, company growth rate is assumed to be 6 %. I invite your views on this assumption, since it plays an important role in the final valuation. My perpetuity assumption is based on two factors:

a. World GDP growth rate of 2 % and a long term depreciation of the Rupee of 4 %

b. Even large companies like Infosys, TCS etc. are able to achieve more than 6 % growth

I have used the current Free Cash Flow (CFO minus capex) as the starting point and valued three different growth rates under each scenario – a base case of 6 % growth, 12 % and 18 %.

I have used a discount rate of 13 %. This is the rate I use for a business model I consider “medium risk”.

Based on the above, I get the following values for the company:

| Growth Rates | Normal | Ex-JLR | ||||

|---|---|---|---|---|---|---|

| Growth Phase % | 6 | 12 | 18 | 6 | 12 | 18 |

| Perpetuity % | 6 % p.a. | |||||

| Present Value (Rs. Crores) | 2,938 | 4,519 | 6,963 | 2,351 | 3,414 | 5,570 |

Against the above, the current valuation of the company is Rs.5,225 crore. This approximates to a growth rate of 14 % in the “normal” scenario and 17 % in the “ex-JLR” scenario (for 10 years, and 6 % to perpetuity thereafter). This seems reasonable to me, somewhat on the cheaper side if JLR holds.

Comments and feedback are welcome.

(Disclosure: Invested)

@suru27 thanks for listing down details from the con-call, much appreciated.

@suru27 @biju_john I’ve been adding to my exposure in Elxsi too and I think it is actually attractively priced or at the least fairly valued. I actually don’t find it expensive. Can you please suggest what you reckon is an attractive price?

Here is why I think it’s attractively / fairly priced (well at least this is how I do my valuation analysis / checks).

From a historical PE ratio perspective, its trading at a discount. I’m sure the company has gone through many upheavals in the past and considering the same at the current PE ratio, I think the Brexit / JLR slowdown issues are maybe already factored in?

The PEG ratios across 1 to 5 year periods (not captured in screenshot) are under 1. Even if we look at the recent past performance of the company (both top and bottom line), I think it the stock is looking at the least fairly priced. The earnings growth has easily been higher than the 19 PE. I guess if one were to take out the gains made by exchange rate gains, I think they’ll still be growing the bottom line at least by ~15%.

The earnings yield is 8.31%. Far higher than Bank FDs and the earnings are poised to grow in the future. The dividend yield is decent too. So again, I think it at the least is fairly valued, if not attractive.

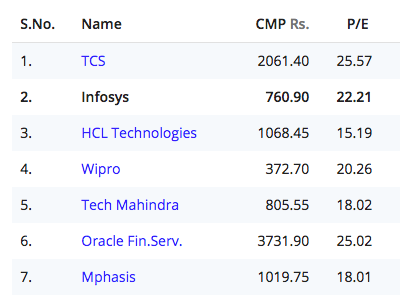

Compared to a lot of its direct and indirect peers / the industry, the stock is quoting in the similar PE range. Considering that the company has robust prospects compared to many of its peers again makes me believe the stock is attractive or at the least fairly priced. In fact, Infy / TCS etc. are quoting at similar PE ratios and their growth is potentially going to be slower than Elxsi’s.

Source: Screener

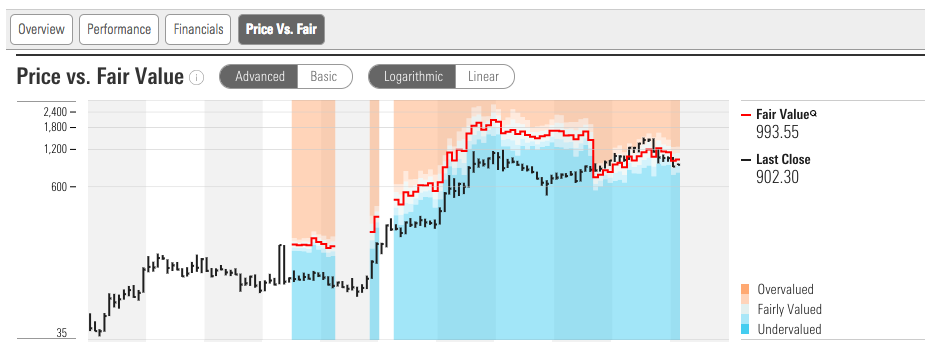

Last check DCF, again seems attractively / fairly priced.

Source: Morning Star

Now, one can argue that valuations are not in a no-brainer zone. But imho, I think its not expensive.

Disc: Invested and increasing exposure. Top 3 holding.

It has decent cash on the books and can potentially get a similar tech profile xompany under its umbrella to add. Also notable factor is medical equipment is a fast growing and again in transitionary phase …It can add significantly and beat automobile segment in coming years. Potential is huge in telecom & IOT segment. Witj aggressive hiring plans it seems to be positioning itself rightfully to demands…Rest depends on how things play out…Runway is huge in all segments it operates.Geographical expansion as indicated by management seems a good step in derisking the business model and TATA brand will help in that direction. I feel favourable towards TE in short and long term. Gold to hod.

Why is no one talking about the merger risk with TCS? How probable is this? While TCS is a great company, Years of high growth need to be built in to Elxsi to justify the price premium which will be difficult if merged with TCS besides the risk of unfavourable valuation as TCS is the big brother. This is the main reason keeping me out of this stock at the moment.

TElexsi is not a product company but eventually has to move in direction of pure product company. Either they buy a company or invest more in IP that takes it to next level. TCS is a full grown service company …they also need to adopt once the business in that direction is crashing which is not the case though the business lines will be redifined as per my thinking and will keep them engaged. As of now directionally TCS does not seem to be right fit for TE…but eventually it is managements call .

Very good point. In the past, I have suffered by buying smaller high growth high margin company in the large group, only to find it getting merged in large slow moving low margin(relatively speaking) company and thereby destroying shareholder value for the minority shareholders of the smaller entity. For eg. Astec merging in Godrej Agrovet.

Hence I decided to stay away from companies like Tata Metaliks (possible merger in Tata Steel), Tata Elxsi ( TCS) etc. I am sure there would be many more companies falling in this category…

It is a fair question to ask and something that may or may not happen. So far there is only media speculation and nothing concrete stated by the management themselves. But one can’t rule it out. It also depends on how the Tata Group have treated minority shareholders (I don’t have a historical perspective on this personally). If they’ve been fair earlier, the probability of them being fair going forward will be higher (again no certainty). Also, I think one is aware of this risk while entering Elxsi.

Regarding valuations, everybody has their own yardstick to judge the value of the company. For me the stock at the moment is absolutely fairly valued…if not under valued. Can you please advise what you reckon would be a fair price in your assessment as you find buying the stock at these levels would mean paying a premium? (again I’m no stickler for valuations, just want to understand your perspective on this)

You know similar dark clouds of Brexit and the JLR account suffering due to this had occurred in 2016. There was speculation on Elxsi being merged with TCS. The stock was quoting at a similar PE range then. Circa 2019 it all seems like Deja Vu to me.

Cheers!

I am no stickler for valuation either. But I would be happy to buy a high cash flow high growth company with growth certainty at around 15PE. While the valuation seems alright at the moment, this stock had been only an average performer not long before. And on top of it, there is the problem of high reliance on related party which is not performing well, brexit woes and on top being in a cyclical auto sector where the spending pattern will depend upon the financial health of the auto industry. Some time back I would have bought at this valuation, but with much deeper values emerging elsewhere this looks expensive at the moment. I will stick with 15PE for this stock.

TCS - with a P/ E of 25+ and M/Cap to Sales above 5 is valued higher than Elxsi. Hence, merger is not a threat from valuation perspective though the actual gain or loss will depend on the swap ratio.