Some of the notes I jotted down in today’s call. I couldnt attend the last 15-20mins. Please add/modify. Thanks.

Larger deals with longer engagement durations, brought in such few last qtrs.

Trying to grow automotive business apart from key accounts.

Medical business is continuing to show encouraging growth.

In broadcast - Winning deals and key customer engagements.

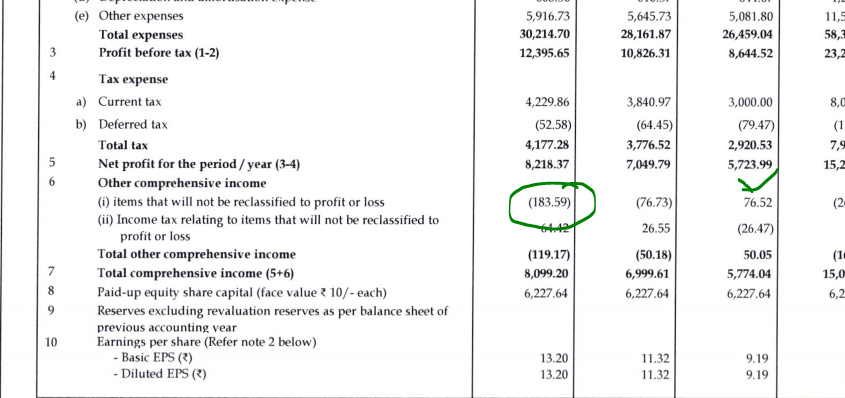

Other income – the component of Fx gain is 14.7 Crs, 9% over preceding qtr and 20% over YoY, in constant currency 3% over last qtr and 10% over YoY.

Design - won no of awards in last qtr for earlier work.

Considerable uncertainty around JLR, not seen significant growth in their engagement yet. Trying to grow business in this segment outside this account and have made progress there in last qtr. A few qtrs. ago 24% business from JLR to 22% last qtr. They are not the largest outsourcing partner for JLR.

Hyundai engagement for autonomous cars more for strategic engagement than for revenue.

Panasonic deal has primary objective to deal with our market and extend technologies to other markets. No change in objectives.

Objective to grow revenue by 10% every quarter sequentially. Categorically saying that this is not a projection. New engagements will be the growth drivers.

24-25% is the objective to maintain margins. Preceding quarters it was higher. (PBT/Sales = margin, including fx gains/loss).

Fx in Q1FY19 was negligible in lakhs.

One autonomous vehicle testing in Europe.

Less than 6k employees in this qtr. Onsite revenues is 40%. 35% of workforce is onsite.

Expect slowdown in ICE engines but have factored in this development.

Interesting implications in renting/leasing cars vs owning cars. Requires tech implementation for pay for use. Not that it will happen immediately but will be a reality in 5 yrs time.

Lot of intricacies involved in making a good quality electric car and refers to complexities involved in making a Tesla eg mechanical structure, drive motor strategy, efficiency, tradeoff between acceleration and battery times etc and in each of these challenges there is an opportunity for Tata Elxsi.

Infotainment will evolve be it android or BlackBerry platform. New opportunities is mostly in electrification of cars on a number of parameters like battery, safety, acceleration etc.