TCS, Tata Elxsi to work on Panasonic products in India

Is it a preliminary sign of TCS & Tata Elxsi merger. Also the article mentions order size of 240 crore over 5 years by Panasonic. Not a big game changer as every one has been thinking of.

I would take it as a preliminary sign of merging. If we study Tata’s acquision of state in CMC Limited in the first phase of investment (2001), TCS and CMC started working together immediately, though then CMC was under Tata Sons. New MD was deputed from TCS (2001) and later management control moved from Tata Sons to TCS (i think 2003), later company made a subsidiary of TCS (much later) after making enough synergy and trimming/fine tuning less profit making businesses of CMC Limited. I seen how this works from close quarters as an employee of CMC then.

If go with that, it may be a slow process. But now Chandra being the chairman this can be very fast considering he knows IT industry the best and if he can deliver some good synergry and resultant growth by pursuing the synergy, he will get breathing space from all other stake holders/investors while he figure out more complex Tata group companies over the years.

Panasonic’s tie-ups with Tata Elxsi & TCS appear to be two distinct things. Tata Elxsi’s Offshore Development Unit for Panasonic will work in the areas of AI and Robotics for domestic and global markets. The Elxsi tie up is limited only to Home Appliances business.

The TCS tie up is for an Innovation Centre and will work in the areas of connected community, mobility, energy (Lithium Ion Batteries) and industrial Internet of Things. It will cover a wider gamut including air conditioners, televisions, mobile phones etc.

There is no mention of “joint” work being done by Elxsi & TCS anywhere.

True @Chandragupta but my question is does TCS really have a niche on M2M connectivity front ? It is Tata Elxsi which is having the capability over there. Obviously the umbrella of contract belongs to TCS and no where it is mentioned that they will going for a merger but isn’t the contract is indicative enough ?

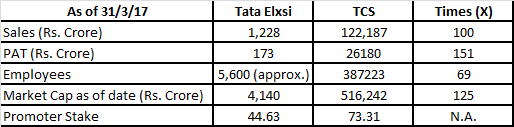

TCS is a hundred times bigger than Tata Elxsi, and more profitable:

Elxsi is growing faster than TCS, but I don’t see TCS financials changing significantly by merging Elxsi into itself. It is like one extra bucket of water in an ocean. On the contrary, if TCS is broken up, a dozen more niche champions suffocating inside will get released. That will create more shareholder value. There is enough evidence that beyond a point, size acts as a disadvantage and brings in diseconomies of scale. TCS may have already crossed that point. Especially when the industry is going through a disruption and you need to re-engineer the company completely rather than make incremental improvements.

Coming to Tata Elxsi, it already sports the Tata brand name and does not need the TCS Balance Sheet to grow. So the merger will not benefit Elxsi either.

Of course, something is inadvisable does not mean it will not happen. The Tatas do not have a great reputation on this count. Independent Directors and institutional investors of Elxsi should oppose any such proposal, if it is ever made. Their past track record elsewhere does not inspire much confidence, but I believe things are changing lately, albeit slowly. This will provide them with an opportunity to show some spine. The Tatas may not want another controversy around the same issue so soon after the Cyrus Mistry fiasco. Let’s wait and see.

(Disclosure: Invested in Elxsi, no exposure to TCS)

I live and work within the industry. So views may be biased -

TCS and the entire IT leadership in India has grown by selling bodies and no disrespect to the doyens of the industry, they are not the intellectual powerhouses that we think them to be. TCS and others are on a cusp currently with fairly large changes in how clients buy technology. There is a visible in-sourcing wave within the industry that may continue for some time … which means that everyone who sells bodies, would struggle despite investments and growth in other areas since base will shrink.

I was tempted to buy TCS 2 years ago but thankfully didn’t and while I’m still evaluating, my guess is that winners in IT would be a different set of companies. And for someone like Tata Elxsi, it is BETTER not to be merged with TCS … culture, size, bureaucracy all would be a factor. Similarly, others like Persistent may be better bets … but my guess is that the industry is being rewritten in US and to participate, one must be on NYSE /NASDAQ.

Well to some extent it is true TCS and other IT companies have been benefiting from cost arbitrage.It was the low hanging fruit of globalization. But over a period of time they are entrenched in the Global IT with long term contracts. It is changing but the delta of change is going to increase every year but these companies being cash rich ar 20% margin, low to no cost or asset light model can transition easily. Automation is going to be a big kicker but with being at the bottom of IT pit and global presence they still stand to be positive for nest 10 years… Tata elxsi is in sweet spot and with embedded software which is going to be key in be it smart cities, Industrial automation, Self driving cars, Smart homes. Just name any device and it is ready for Embedded software. Only problem is the companies mindset is to by second grade R&D partner for MNC’s which is good for gaining knowledge. But if you have to take the company to next level you have to create Intellectual property license it to others and spread your risk. You have to learn from global experience and spread it in local market. The management is smart but Tata group is slow to react and till date though fare have not been dynamic enough. It is a company which can by a great company but if merged with TCS will loose its edge.

Can we dig a bit more into it if anyone here has IR contacts. the contact provided in the link and on the website didn’t help much, will try email too

What is $mm size? is it a recurring revenue? Is the revenue subject to milestones / royalty / bullet payment annually? Additional expenses/costs/headcount that Elxsi maybe required for this win (if the deal size is large).

Also, fundamental qtn to guys covering this stock in detail - how much of overall revenues does Elxsi generate from this idea, if someone can please share?

Just speculating, can it be JLR? (is it one of the top 5 OEM?) and do they have such R&D program? And if it is not JLR but some ‘external’ OEM, then upside can be even higher if this relation is successful.

Interesting development. Will wait and see how it progresses further, as at the moment it is only for OEMs R&D purpose.

“Bangalore: June 5, 2017- Tata Elxsi, a global design and technology services company and a leader for automotive electronics and software development, announced the licensing of its advanced autonomous vehicle middleware platform “AUTONOMAI” to one of the world’s top 5 automotive OEMs for their driverless car R&D.”

One , their projects are 6 to 9 months in nature, may be a year at max. So, till project is delivered successfully, staggered payment is not that important. Second, I believe this is a platform which could be replicated to other OEMs interested in driver less cars and hence at framework level, could be replicable (i may be wrong). third, I feel this might be GM as GM is one of top 5 OEM by revenue and they look ahead on driveless cars compared to other 4.

Recently I saw this blog that had listed some 250 odd startups around driver less cars. Will search and send…but the point is that it is extremely hard at this stage to figure out the winners and just because someone is playing doesn’t mean they will win

So to clear what the opportunity actually is, I read through the DRHP of LTTS which is into similar businesses. These are my key takeaways.

For starters, would it wrong If I compared the size of this opportunity to the once Infy and TCS had in terms of the labour arbitrage. I havemt come across major EPD players on a large scale globally as gthe market itself is developing. With Indian companies like LTTS, Sasken , Elxsi and Persistent developing domian expertise in areas like EPD, IC Design et al, could this usher in the ITeS 2.0? Product Engineering .docx (444.3 KB)

Tata branding and key segments in which Tata Elxsi is present makes it a prominent first mover player creating a unique opportunity. The margins is a pain point but that will change once it entrenches itself in Global R&D outsourcing. Labour arbitrage with no H1b visa headwinds. My guess it will see significant heights in next 10 years. One problem as per management commentary it gets short term projects 6- 18 months which is offset by deep client relationship short tenured low value projects blinds the growth trajectory which is a bottleneck Core holding

However the other impact of margins is retention rate of employees once they cross 2-3 years of experience from freshers. Attracting best of talent n retaining high performing talent needs lot of margin advantage . That’s how product companies retain best of talent . Don’t see that happening in this in near future but may be slowly if structurally they evolve. Disc : 4 % of portfolio