Current Watchlist

- Prakash Ind

- J Kumar Infra

- Tiger Logistics

- Thangamayil Jewellers

- CESC

- PSP Projects

- Lasa

- Genus Power

- Hawkins

Plan is to deploy cash slowly.

Would appreciate if fellow boarders share their thoughts

Current Watchlist

Plan is to deploy cash slowly.

Would appreciate if fellow boarders share their thoughts

I don’t about the rest. But I have high conviction on Prakash & PSP. I have both of them in my portfolio. Could you add any of the listed in watchlist during past few days?

Have been buying

Am adding these slowly.

Have sold off Camlin Fine Sciences (+30%).

CESC (4%)

Maithan Alloys (4%)

BEPL (3%)- sold half of it

Avanti Feeds (3%)

NCL Industries (3%)

Tiger Logistics (3%)

Sinclair Hotels (3%)

Indian toners (3%)

IIFL(2%)

Motherson Sumi (3%)

Thangamayil Jewellers + PCJ + TBZ (6%)

Spicejet (1.5%)

SPTL (2%)

ZF Steering (3%)

Mirza Int (3%)

Equitas (3%)

Genus Power (2.5%)

Srikalahasthi Pipes (4%)

Reliance Capital (1.5%)

Infra: PSP + Rel Infra + JKIL (6%)

Pharma: Lincoln + Eris (4%)

Hawkins (3%)

23: Construction: Sahyadri + Everest Ind (5%)

24: United Spirits (3%)

25: Housing Finance: Indiabulls Housing + India Home Loans (4%)

(Rest 1% or less)

Would request fellow boarders to kindly give their valuable views and feedback. Even if a sentence. would love to learn.

still working on asset allocation.

Wish to bring stocks to 15 -18.

reduced few cyclicals as previously guided by seniors.

Thanks to all for sharing their knowledge openly.

Removed 8-9 minor laggards which had 1% or less allocation with around 5% loss & moved the funds to Accelya Kale.

Hi Tarun,

A good list of companies you got there. I have a few questions:

Thank you.

hi @dineshssairam

i was reading your thread only sometime back.

i am not from a finance background so i depend on stock selection from advisories/research reports/VP. STill in the reading stage.

after i read the stock selection which always contains valuation calculations usually i read through last 1-2 annual reports briefly to get management view, shareholdings pattern, director reports, view cash flow statement, last few quarter results.

& after this i download the excel from screener based on dr vijay malik website and go through the important raitos and stock history. also sometimes i run few screeners to see if they fall in any of them if any issues i refer to valuation based on websites like marketmojo. the process is still evolving. please suggest if yu can if it can be made better somehow, am all ears.

i want to diversify lesser and this list has been decreased from over 50+ stocks . Am trying & hopefully ill be able to first get it less than 20. i understand this much diversification limits wealth creation but my extreme risk averse nature makes it a bit tough.

3.HMVL was a very early buy and was based on @desaidhwanil ji’s thesis & was a part of the advisory portfolio i had subscribed to, you may like to look at dhwanil jis posts on the same. Now it is neither held by Dhwanil ji or in my advisory. Main issue was nothing was being done with the cash which was there in plenty as far as i remember. not tracking it since long.

regards

Thank you for your remarks.

I asked if you valued your picks because you had so many. Going through the annual reports is a wonderful practice, of course. But you say you use websites like MarketsMojo for Valuation. These websites largely rely on Ratios, which are dubious in my opinion. Ratios do post mortem, when Valuation requires diagnosis. If at all possible, try learning about some kind of Valuation model that involves accounting for Free Cash Flows. If you still want a ‘quickfix’ Valuation took, I’d suggest the one from MoneyChimp. Try not to let it be your only resort for Valuation. It’s dangerous to punch in a few numbers without understanding if they make sense and how.

About HMVL, yes, I’ll read those posts. Indeed, a greedy management can lock up value for a long time. HMVL was on my radar for some months. But their shady activities like starting a ‘Digital Media’ company using their Owners’ cash is disappointing. I don’t track it any longer, so I was curious to understand your conviction.

Best wishes.

Thanks a lot for your input.

removed other small bets and rel infra to move the funds to

purvankara (affordable housing play) (3%), welspun enterprises (road infra play) (3%), Prakash ind (steel cycle and impending demerger) (2%), meghmani organics (3%).

sold united spirits and added HG infra instead.

Removed hawkins and added Hikal.

If I read your thread and its contents over the last three months, I see that you are impatient and repeatedly selling some and buying something new. Sell the ones which you feel are not worth to hold and invest only into your existing holdings until you reach the optimum size of portfolio you are comfortable with. Or decide clearly on which companies are to be exited and which are your new target companies. Do not waver.

Sir how do you manage to track your portfolio of more than 25 stocks?

Tarun, only one advise from me. Take a deep breath and read ‘one hundred baggers’ by Christopher Mayer before going any further. Frequent churning never helps. Only your broker will be going all the way to the bank. I have the same problem. But I am in the middle of reading this book and determined to forget the sell button as long as I can. All the best!

Thanks for suggesting the book, will surely read it soon.

Working on it. I feel we all know the correct way but our biases & emotions make or break the investments.

Its a test for me personally as well to be steadfast and less sensitive.

Over Diversification is directly proportional to lack of knowledge and i admit it.

Trying to build a better one and learn better.

Very apt observation sir.

Sometimes we need to listen it from a fellow being despite knowing it.

Appreciate it a lot.

Working on it.

Regards

Finally sold all the holdings in BEPL as i think opportunity gap is reducing and it will be a compounder now. Being a cyclical couldnt hold it forever.

Has been the best performer since i started investing with extremely humble amounts around 2 years back

Sold it just around holding for an year.

Thanks to everyone on the forum.

Yu r unsung heroes whom i follow, copy , learn from on a daily basis.

Thank yu so much for sharing honestly from ur heart always.

This is one of the achievements of my life which has finally made me happy from within.

My dad is very risk averse & was extremely against me on even opening a private bank account when i opened one in kotak and one in indusind 2 years ago for savings & investments respectively.

My mom permitted me to open a demat account and told me she ll give me a lil amount to try.

Today my dad told me he wants to open his demat account.

Regards.

Stay humble & shine on

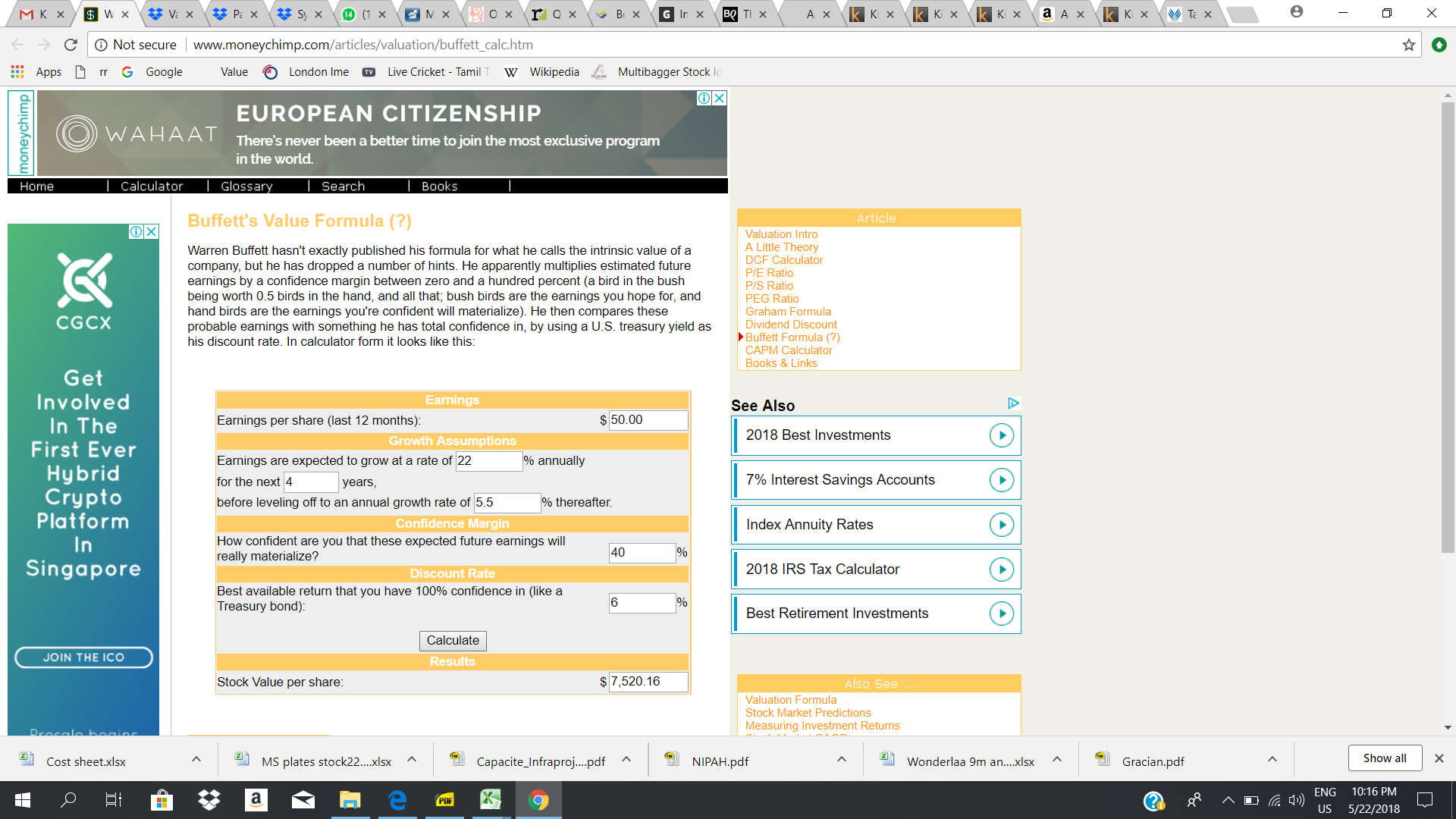

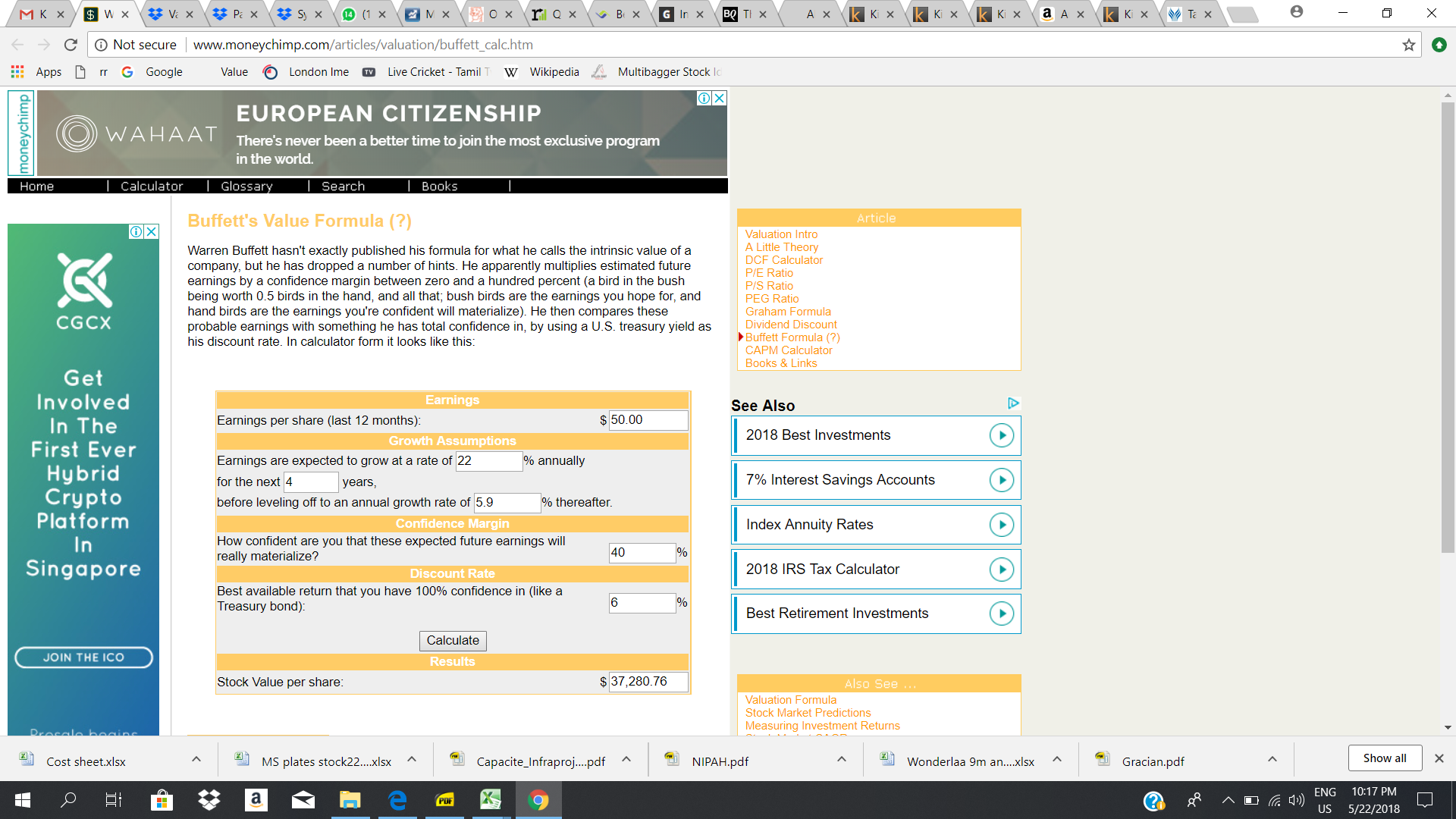

Hi DINESH ,

tHE below is the snapshot tof a trial valuation I did for bajaj finance :

why is there such a huge difference between the " levelled growth rate : " of 5.5 % and 5.9 %

The below snap shot shows 5.9 % " levelled growth rate "

The levelled growth rate essentially says that the company will grow at that rate forever. Well, at least until the denominator, the discounting rate becomes substantially higher than the numerator (Which is EPS * (1+growth)).

So when you change the levelled growth rate, you’re simply seeing the compounded effect of that 0.4% change for a long long time (Say 80 years).

A few suggestions:

Growth rate should be the long term compounded growth rate. Short term bursts of growth doesn’t mean that the company will grow at that rate going forward.

Length of high growth (Before levelling off) could be anywhere between 10-20 years, depending on the type of company. Really excellent companies, with huge moats and superior pricing power can growth at a decent pace for more 20 years. But exercise caution.

The discounting rate should be higher than the Risk free Rate (Which is 7.5% in India now). Ideally though, feel free to use 12-15%. This is what you would earn on investing in the NIFTY or the SENSEX for a really long time.

In the end, like I already mentioned, finding out the Value of a company with 2-3 numbers and the click of a button is too simple. It’s a better starting point than a P/E Valuation, but it’s not the be all and end all of Value. This is what I use to Value prospective equity investments: