SOUTH INDIAN PAPER MILLS LTD(SIPL)

CMP:98.00

MARKET CAP:153 Cr

BSE code:51608

SIPL is kraft paper and box manufacturing company having its plants near Mysore, Karnataka.

It recycles waste paper into various grades of kraft paper and sells it to local vendors who in turn convert them into customised boxes for various companies. Annual capacity of paper mill is 60,000 tons.

SIPL also has its box manufacturing facility near the paper mill which consumes 50% of its paper output to make boxes. Capacity of box manufacturing plant is 30,000 tons/annum.

I will not write much about paper industry as it is very well covered in various threads of paper companies in the forum. Below are a few points which interested me and I have tried to cover them in AGM notes:

1.Mr.Manish Patel, MD of the company is very dynamic and technocraft. The feedback I got from scuttlebutt was that the MD knows about the minute details of each and every machine installed in the company and takes care of them regularly. MD himself works on repair/installation of new machine.(Total promoter holding is 43.2%.Well known investor Anil kumar Goel holds 6%)

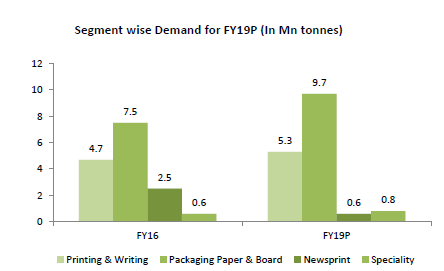

2.With ban on plastic by regulatory agencies, as an alternative I believe the demand for kraft paper and packaging will continue to grow by FMCG/E-commerce. Recent presentation from Ruchira paper ltd estimates demand for packaging paper and board at 9.7Mn tons in FY19.

Indian paper mills association data for demand of various paper segments

3.China’s ban on use of waste paper is creating large opportunity for Indian paper mills in terms of getting raw materials at a lower cost and also export opportunity.

4.During Fy18, SIPL operations were affected by labour strike which got prolonged affecting the company’s performance with revenue dropping to 134Cr from 195cr in fy17. Post resumption of operations they were able to get back all the customers. I have confirmed this during my scuttlebut and seen their products.During H1FY 19 their revenue and profit growth is good and likely to continue.Last few years production/revenue:

| FY | H1FY19 | FY18 | FY17 | FY16 | FY15 | FY14 | FY13 |

|---|---|---|---|---|---|---|---|

| Production of paper/paperboard(T) | 32687 | 52752.0 | 56268.0 | 49058 | 36891 | 49678 | |

| Conversion at box plant(T) | 15522 | 26196.0 | 26659.0 | NA | NA | NA | |

| Conversion% | 47.5 | 49.7 | 47.4 | ||||

| Net sales(Cr) | 122 | 134 | 195.0 | 207.0 | 185 | 143 | 168 |

| Op.profit(Cr) | 16 | 14.3 | 33.0 | 36.0 | 30 | 15 | 27 |

| Op.profit% | 13.1 | 10.7 | 16.9 | 17.4 | 16.2 | 10.5 | 16.1 |

| Net profit(Cr) | 9.5 | 0.9 | 11.9 | 24.0 | 13.5 | 3.8 | 13.6 |

(South India Paper Mills Ltd financial results and price chart - Screener)

I have attended the AGM of SIPL where I could spend a few hrs with MD. Below is the notes I prepared which gives an idea about the present scenario of the paper industry, influence of China factors on it and SIPL business aspects, expansion & future plans. (!There may be a few mistakes from my side while noting down the points)

Q.Update on China ban on importing waste paper for recycling.How does it benefit the Indian paper mills/our company?

China govt has banned import of waste paper except a few higher grades and they are very strict with their policy(they are allowing import of fresh pulp). This has resulted in significant reduction of the cost of waste paper being used for recycling which has greatly benefitted Indian paper mills importing waste paper. Bearing the transportation charges is all that is required to import some of the lower grade waste paper. This has good demand from Indian mills which are importing and converting into paper. After converting, paper is sold either in the domestic market or exported to China. Presently all the mills having good time with China absorbing the output easily. Chinese are in turn using them as raw material /converting these paper into boxes and selling them.(Indian mills importing certain low grade material for 90$ and selling at 380 $ after processing). This trend is seen since last 5 months.

Supply of paper for domestic use has reduced due to better prices with export. Demand for kraft paper by local mills is very high presently due to low availability and increasing demand by end user. We are both selling our kraft paper to local box manufacturers and exporting.

Q.How is paper export working for SIPL? How about the margin for the same? how is the feedback from customers?

It is a new business for SIPL, started just a few months ago. We exported a few hundred tons of paper last month. Our paper quality has been better appreciated, received and accepted by customers compared to other Indian exporters. (He showed a mail received from customer appreciating the SIPL paper quality). Exports are happening to China,Bangladesh,Sri Lanka. We get better margins than domestic. We can’t export much, as we need it for our internal consumption to make boxes. We have reduced our paper inventory also. Exchange rate is also helping in export of paper

Q.Current outlook on our box division:

Current demand from customers is good. We have got back all the customers whom we lost during labour strike. Getting revised price hike from fmcg players is difficult. Even though we can sell more paper with price hike, we don’t want to lose our regular customers for boxes(like nestle/Britannia). We are negotiating for price revision from them which should happen now. If not, we may sell more paper directly.

Q.Educate us about reason behind importing raw material. why can’t we use domestic waste paper? Effect of rupee depreciation?

Raw material cost has come down but exchange rate has increased. We import 50% of raw material from outside(?US) and rest is sourced locally. Imported material has lot of virgin content compared to domestic. When we process raw material we get various grades of fibre ranging from long,medium and short length which is classified as M1 to M5. We import DS OCC( double standard) material due to higher content of M1/M2/M3. With M1 to M3 grade fibers, the quality of paper and box will be excellent. With domestic waste paper we get only M3 to M5 grade fibre. Our raw material cost has reduced from 320 $ in April-17 to 220$ presently. It may further go up depending on China demand. We can’t import low grade material, as the waste generated from paper mill has to be disposed by us.

Q.What differentiates you from other paper mills/kraft paper/box manufacturers?

Quality and timely delivery of boxes to customers is most important.We go by quality and that’s what I insist my team to maintain in each batch we produce. If we can maintain superior quality then we can ask for more price as well. Presently quality of the paper / boxes used by many companies/E-commerce players is not good. Our goal is to provide superior quality material at lowest cost possible. Due to our technology(3 ply) we are able to reduce 10% of cost to our customers.

Q.Who are your major customers? how is the business doing?

ITC: Our relation was a bit rough with them initially but of late they are preferring our products due to cost saving and quality.

Nestle: around 230 tons

Asian paints: new plant is starting soon(October) near our factory. We have been working with them from the beginning. We are going to get around 200 tons of business from them once they start production.

GSK and Reckitt benckiser (200 tons) have increased volumes with us.

Others like United breweries (not in constant business with us), few other alcoholic manufactures.( I have noticed a lot of other company boxes manufactured by SIPL during my scuttlebutt)

Q.How is the opportunity for us in growing e-commerce business?

In the past, we submitted our product to them and got approved. Problem with doing business with e commerce players is that, even they won’t be aware of their requirement. They are going to ask for 32 types of boxes of different quantity in single day based on their sales. Correct way to manage business with them is to have a warehouse with different boxes and supply accordingly. Currently their overall requirement is not equal to single brand like Britannia but we cannot ignore e-commerce as its continues to grow rapidly. Amazon has a global policy completely shifting from plastic to paper based packaging. We will meet them with our products and plan.

Q.Update on labour strike/issues affecting our production/agreement with labour union

Actually everything was in place for agreement but few people have spoiled and went on strike. To some extent issue was prolonged by karnataka elections. After a few months, we could come to agreement with slightly higher salary revision than our expectation which is loss for company. But we are to bring certain changes in recruitment of people and time duration of agreement.

Q.Govt has initiated anti dumping duty on paper. Can you give more insights into it? How does it affect SIPL:

The particular Anti-Dumping duty proposed is on writing and printing paper not on our raw material. We are not going to be affected by it. To prove that the actual dumping is happening, will take 1-2 yrs. Asian countries comes under free trade agreement and putting normal duty is not possible. Certain countries ( Taiwan company)used to sell their Kraft paper at low price in India. We also purchased small quantity from them in the past to try their material but realised their quality is low to make boxes and not suitable for us.

Q.What is our capacity in paper and boxes division/ utilisations

Paper capacity is 200 tons /day. Presently we are producing around 180 tons/day. (calculate for 25 days/month),per month it will be 5 to 5.5k tons. Yearly 60,000 tons.

Boxes capacity:100 to 150 tons(115 to 120 tons/day in light wt). presently working in two shifts only, can produce upto 30,000 tons/annum. With three shifts we can reach upto 40,000 tons.

Q.Current selling price per ton of paper/boxes? Any price hike taken recently? What is our additional cost in converting paper to boxes and additional revenue possible by making boxes?

Presently we are selling paper at 34,000 on average ( range from 32k to 44k for prime grade).Paper is sold to local vendors who in turn make them into boxes and sold in market. We have got price increase of around 2000/ton from paper customers.

Box customer our avg selling price is 42,000 per ton.We are pushing for for price increase of 3000 /ton. With box customers its slow to get price increase/decrease.

Margins: when we sell directly to paper customers:at avg price of 34k after deducting direct cost like raw material,chemical,fuel( employee cost not included) we are getting around Rs.6,750/ton.

When we transfer paper for our internal consumption and selling as boxes after converting at avg cost of 42,000k/ton. We are getting 8,000 as my extra benefit.conversion cost from paper to boxes is around Rs. 5,000/per ton.

3,000 is what additional margins we get from box conversion + (6,750 from paper)…totally we get Rs.9,750 to 10,000 per ton of box. From this have to deduct fixed cost/employee cost/interest and overheads).

Q.Outline your capacity expansion plan? Why did we decide to go for paper capacity expansion rather than boxes?funding and additional revenue possibility?

Capacity expansion was delayed from our end, else we would have enjoyed really rosy now. To some extent it is affected by labour strike.

It is important to have good paper manufacturing capacity before starting box division. Before capacity expansion we need to think about how sure about selling / how much and how sure about collecting money. right capability right people.We have excellent team.Technically we are good and we also understand the market

Our new paper capacity expansion is for 350 tons/day but the net addition will be 230 tons/day as existing two line PM1and PM5 with capacity of 85 tons will not be used due to certain issues. The planned expansion is to produce paper in the upper band of segment ie 24BF and above(less than 24BF is common grade produced by everyone)

The capacity expansion will take 1.5 yrs and we will be able to use full capacity in 6 months. With full capacity at present prices our revenue will be doubled to around 450-500Cr

We did lot of search before finalising the machine. Myself went to Europe to finalise it. The core part of machine will be imported from Europe and non critical hardware will be from China. Nobody in India has this particular machine.Its more accurate,technically superior,fast,gives better quality of paper and effective utilisation of power. With increasing capacity we have shift to continuous process rather than present batch process.

Total cost of expansion will be 125 cr+GST.60 cr from internal accrual and remaining 90 cr from debt.Will be having debt once work is done with of interest of 8 cr /Yr

We will plan for box manufacturing capacity somewhere near Pune region or Chennai or acquire some facility but all this is long term not now. Presently we are focused on paper capacity expansion.

Q.What other products are possible from us in future?

With govt banning plastic bags, the paper bags demand is on rise. Technically we can but need to have new line to manufacture paper bags.

Other possible product is to make material for false roofing what is called as gypsum board. It has paper in the middle hardened by calcium phosphate and some other chemical material. With the present machines we can manufacture it but having technical difficulty in contraction process. New machine will solve this problem as well. Presently this material is imported to India .

Land : we have been purchasing land keeping future expansion in mind near the existing factory. It also gives us right to use water from nearby reservoir.

Others points:

Promoter stake sale: they are not actively involved in the company.

Key risks/negatives:

1.China factor: If the china govt reverses its decision on ban of importing waste paper, it can affect the Indian mills severely as the raw materials cost can shoot up and the demand for end product export opportunities may come down.

2.Paper Sector being a cyclical business hasn’t seen much capacity addition in the last few years. Few companies(like Ruchira) have announced significant Capex. When the additional capacity comes online in next 2-3 yrs, then paper mills may suffer a blow

3.Govt imposing anti-dumping duty on import of raw materials(seems like distant possibility)

4.Rupee depreciation can make the imports costlier, affecting the margins

5.Risk of labour union strike: SIPL has faced this issue twice in last 7 yrs affecting company’s performance. It can happen again if the company does not reach an agreement in time with labour union.

6.Not much top line growth may be possible in fy20 until new expansion comes online.

7.Environmental /waste discharge: Waste generated by paper mills has to be disposed properly. Any mismanagement in disposing waste by SIPL can be serious trouble as it is surrounded by agriculture area.

Disclosure: 7% of my portfolio is in paper stocks. SIPL around 4%