Good Numbers

SONATA SOFTWARE Q1FY22:

(QoQ) Performance:

Revenue : 18.45% up

PBT : 4.42% up

(YoY) Performance:

Revenue : 35.7% up

PBT : 73.7% up

EPS:

JUN-20 vs JUN-21

4.8 vs 8.35

EBITDA MARGIN:

JUN-20 vs JUN-21

8.2% vs 7.96%

Good Numbers

SONATA SOFTWARE Q1FY22:

(QoQ) Performance:

Revenue : 18.45% up

PBT : 4.42% up

(YoY) Performance:

Revenue : 35.7% up

PBT : 73.7% up

EPS:

JUN-20 vs JUN-21

4.8 vs 8.35

EBITDA MARGIN:

JUN-20 vs JUN-21

8.2% vs 7.96%

Low operating margin a concern

Mgmt seems bullish for the next couple of years…for the company and the IT services sector as well

Excellent Quarterly Results

Sonata Software

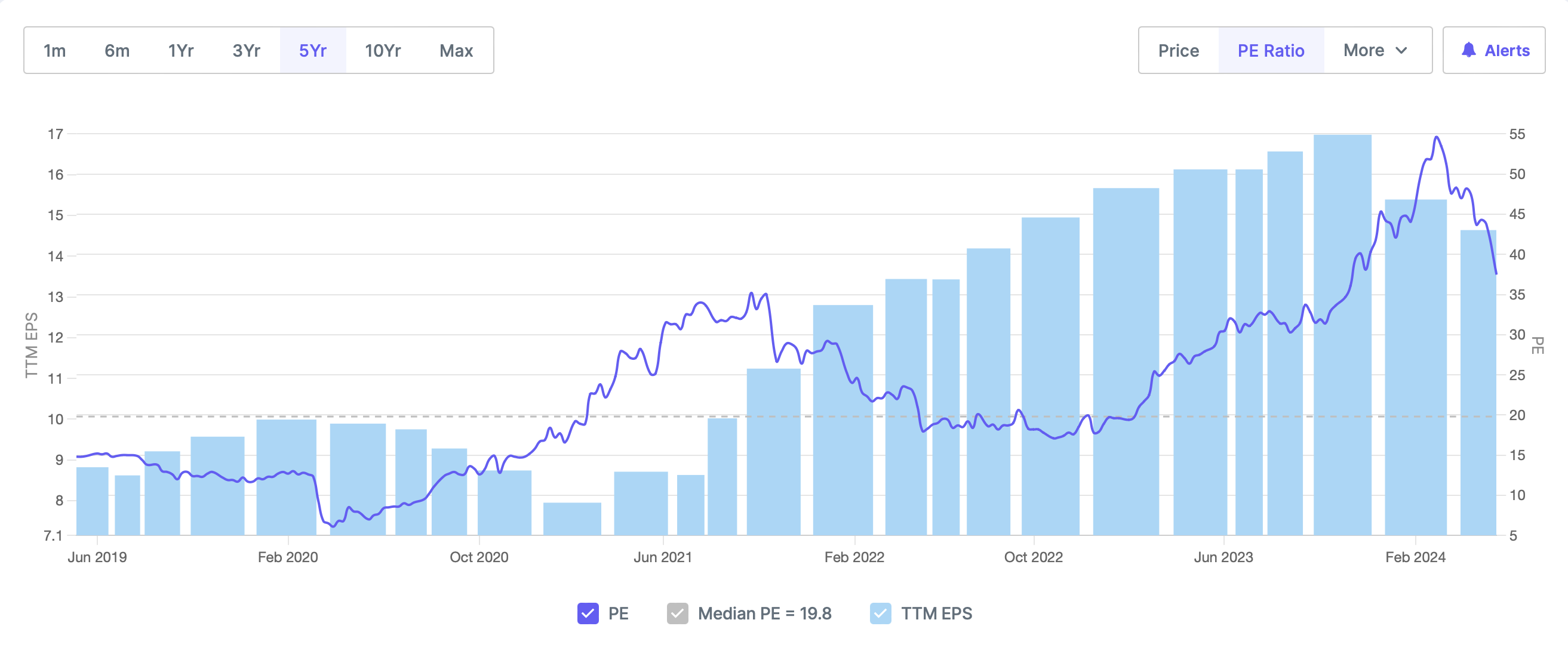

Stock P/E:19.9

ROCE:43.7 %

ROE: 37.2%

Last 10 years’ CAGR is 67%, though for the last 3 years is not so impressive 16%.

Another negative is that it has risen by about ₹90 in the last one month.

Not invested.

Sonata Software to consider bonus on 25Oct, also good quarter expected.

Good Sets of Results from Sonata Sofware in a tough environment.

The company is making key bets, especially in the AI and generative AI space. Sonata aims to lead the AI wave from the front with its AI power solutions of Harmoni.AI and we expect that to be a 25% of our revenue in two to three years’ time from now.

Vision of the company:

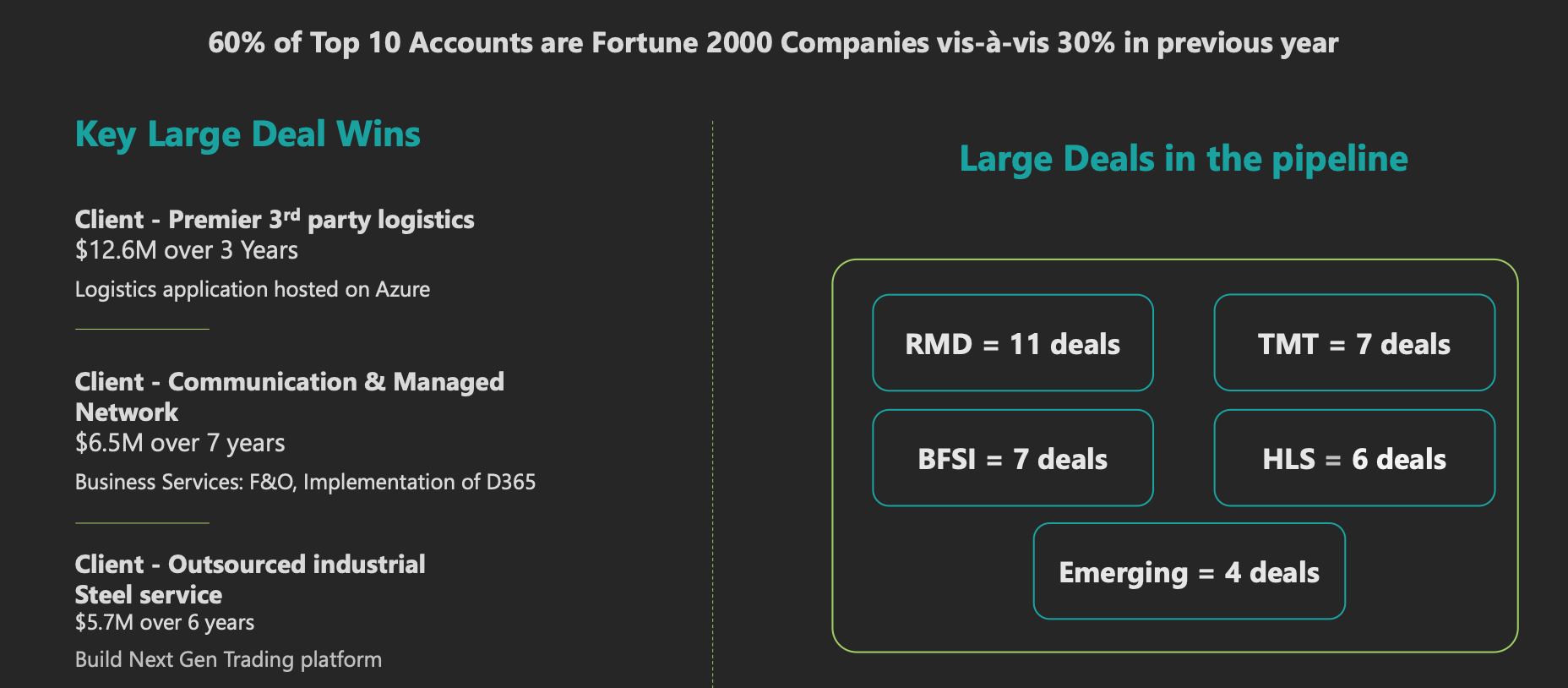

Deals in Pipeline:

Hi, any idea on what is the record date for the bonus issue?

Answering my own question, record date is fixed at 12th December [Explains the surge in share price yesterday, even though announcement came later]

Hi, it’s been an year. Did you choose to invest in Sonata Software? The revenue increase has been as per management guidance, and Sonata’s 20% profit comes up from BFSI. I am positive about it’s upcoming result.

The market is highly rewarding good result in IT (OFSS), and punishing bad results (LTIM)

Anticipating good results based on management commentary during Q2 earnings call and also in late December. Invested.

Good results but overall loss in quarter due to Quant Systems acquisition.

Also company had to pay extra 17 Crore extra due to change in valuation of Quant.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/5eb750c4-25fb-4697-a1cf-6e5ab404e50f.pdf

Sonata Software (SONATSOFTW) Q4 FY24 Earnings Call Highlights

Financial Performance:

Operational Performance:

Future Outlook:

Concerns:

Other Important Points:

The recent correction makes the stock a very compelling buy.

The company is operating in an industry which has severe headwinds where the large players are taking a beat.

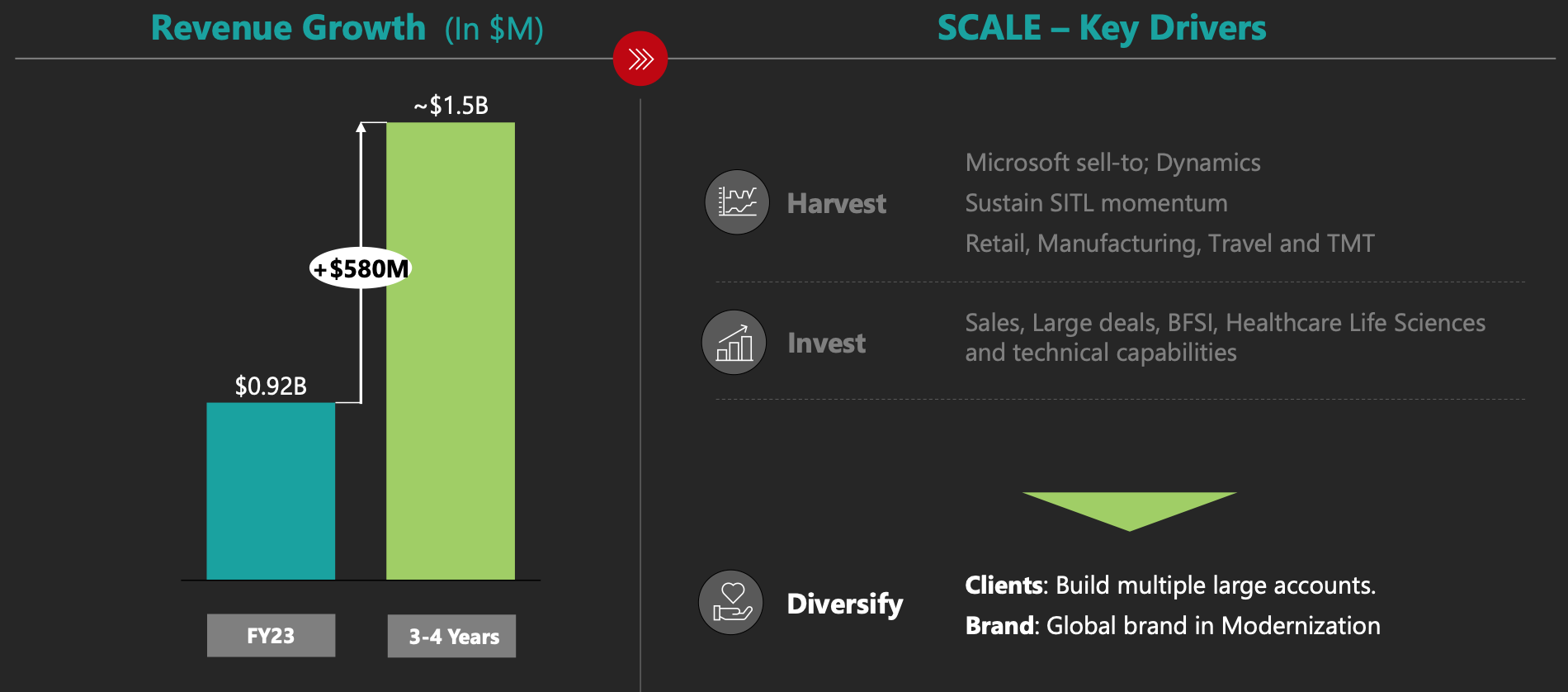

However, the bet is extremely favourable (imo) as it operates in very lucrative and growth industries like * Healthcare, Life Sciences, BFSI, Retail Manufacturing, and TMT across key geographies. Aiming to reach $1.5 Billion revenue by FY26.

Valuations are coming down and increasing the Risk Reward Ratio

So do you think that the current falling trend in share price is due to the one-off bad quarter and this might revert in future?

never buy a falling stock, the market knows better than us, avoid buying now and only buy once it starts going up