The company could do much better than this as discussed on this thread…

So so performance

Outlook money has also recommended this share considering that plastic companies margins are expanding.

The debt level of the company has been increasing year on year, which will remain a big negative and will not allow the company to get premium multiples.

there are many more good opportunities available in the market,

not invested and will remain cautious before considering to buy

I find sintex one of the cheapest stocks available in the market which satisfies multiple criteria ;

increasing operating leverage - this year, they are sweating their textile assets and their factories for pre-fabs

improving outlook for their prefabs business - with infra slowly picking up, I see a big downstream deemand for security guard shelters, doors, cabins etc.

improving mix of custom moulded plastic - used in cars, automotobiles - with car demand and LCV demand picking up, sintex will benefit greatly -including from the simonin acquisition

improving textile utilization - with their spindles coming on stream this quarter, they should see an improvement in revenue and overall margins

tailwinds from a rural push/friendly budget and swach bharat abhiyan - I have seen portable urinals being constructed in a few places around the city and again this should benefit pre-fab makers like sintex. Also, the push on affordable housing (which means demand for plastic windows, enclosures, tanks) should benefit

There are governance issues for sure - but at 7 x FY 16 E and probably 5 x FY 17 E, i see little downside here and a multiple optionalities on upside

Since most of the FCCB conversion/Equity dilution is over, now improved profitability would improve EPS, which in turn should help market price, even if the PE ratio remains same. If stock gets rerated, that would be kicker!

What troubles me is their unending desire for more and more debt? They have converted FCCB but have increased debt.

Q4FY15

Long Term Debt = 3182 cr

Short Term Debt = 774 cr

Q2FY16

Long Term Debt = 3947 cr

Short Term Debt = 967 cr

On top of this they have Non-current Investment of 251 cr in q2fy16. Balance sheet has quite some holes.

A company funding its business from borrowings will always have trouble

Read warren buffet letters to shareholders page 6 and 7 for 2007

Very nicely explained

Not invested

Sintex Dec quarter results are out. Sales and EBITDA are up 12%, PAT up 11%. Prefab Building materials and Textile business grew 21% and 38% respectively as compared to Dec 14 quarter. Custom Molding shown degrowth of 1% as compared to Dec 14 qtr. Weaker Euro affected overseas revenues and Chennai flood affected custom molding business for the quarter.

Important to note that finance cost has gone down from 65 Cr to 58 Cr in this quarter on consolidated level. So it will be interesting to find out if the their debt level has gone down or if they have replaced expensive loans by cheaper ones.

As more spinning capacity comes on-line and starts generating revenue (as can be seen from jump in revenue of Textiles), it will provide big jump to revenue and profits in next few quarters.

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=d093b888-ce04-456c-ad7c-0edc9ed298f7

I believe the Finance cost is down because they have converted all FCCB debt into equity which is why in every quarter over the last year even though there has been a good rise in PAT but hasn’t resulted in any EPS growth. However, 6 consecutive quarters of higher PAT (from 10-30%) YoY should not go unnoticed by the market till long.

What worries me about the business is it seems very capital intensive business which means ploughing in large capex YoY leaving behind little free cash flow. Thus, I’m a little skeptical of how quickly the debt can come down.

On the upside, it’s priced at <8 times FY16 earnings which doesn’t leave room for any significant downside given its improving results every quarter.

I’m really confused to be honest!

Invested with more than 10% of portfolio and it’s barely moved the needle for me in more than 1 year of holding period.

Gurjot

It might make sense for you to be patient and wait until june when the revenues from textiles kicks in - that will be margin, ROCE accretive (since the current dead weight FA’s will start sweating).

Said that, the governance lapses (one more this quarter- check the results announcement) keep me a little worried - if they can de-merge the business eventually, this can be a good one.

I would wait to see a little more .

CONFERENCE CALL - from Capital Markets

Sintex Industries

Revised top-line growth and bottom-line growth to 15% in FY16

Sintex Industries held a conference call to discuss the results for the quarter ended December 2015. Following are the key highlights of the call:

Highlights of the call

The consolidated net sales for Q3 FY16 have inclined by 12% to Rs 2044.98 crore. The net profit has increased by 11% to Rs180.10 crore.

On an avg. commodity price drop by 20% in Q3.

The company has seen large volume in Q3.

The sales of Prefab building systems was Rs 583 crore (up 41%), monolithic was Rs 253 crore, custom molding was Rs 869 crore, and textile was Rs 256 crore.

Executions under CSR for corporate’s and clean India initiatives driven by government spending, significantly boosted Prefab revenues.

Building materials business grew 21%. Government spending has picked up the momentum which will entail smooth flow of orders. While picking up of corporate sector for CSR spending and capex’s in longer term will ensure a robust pipeline for building materials.

Prefab saw large order from lower contribution products like toilet and waste bin, which impacted the margin in Q3. Don’t expect margin to come down future.

The mgmt said Clean India saw large order in Q3 and even positive moment from CSR activities. If volume maintains, the mgmt will think of expansion in pre-fab facility.

Reflecting the festive season and aggressive promotions by automotive manufacturers, the domestic custom molding grew 34%. While a weaker Euro negated overseas revenue impact

The fabrics business grew 38% for the quarter under review with launch of innovative designs and varied product mix.

EBIDTA of Prefab building systems was Rs 121 crore, monolithic was Rs 36 crore, custom molding was Rs 117 crore, and textile was Rs 58 crore

Textile saw 38% growth due to yearn trading business which it started recently

Increase in cost of material because it produces 30% more products.

The company subsidiary has formed JV to manufacture fuel tank for major automobiles players in India

The spinning project is progressing in full swing with 35,000 spindles. Initially, envisaged capacity of 1,00,000 spindles on commercial basis will commence production in near future. Full utilization will take 9 months and optimization of product mix will take 18 months.

The company is going to produce compact yarn. It will be significant player once complete. At present, 1.5 mn spindles is installed capacity of India

The mgmt said that people are switching to compact yarn from older technologies. Compact yarn demand is quite strong. We are producing high value and value added yarn.

For yarn, China is a big customer. Yarn business can be impacted due to slowdown in China. China is largest market; it controls around 36% of world textile market

The mgmt expects Rs 800- 1000 crore revenue from spinning in FY16-17 and Rs 1400 crore in FY17-18. Reduce estimates due to cheaper cotton.

Margin for spinning will be 19% in FY16-17, without incentive.

The company saw increase in net debt by Rs 500 crore vs September 2015 due to spinning biz.

The mgmt has revised topline growth and bottomline growth to 15% in FY16 from earlier guidance of 20% due substantial fall in commodities prices.

Lol,

FY16Q3 eps is less than FY15Q3 even though profits are higher, This is due to equity dilution of more than 20%. With 15% growth guide line next quarters eps will also decrease.

This is pure Trap stock.

Its a Value Trap as stock looks cheaper but its not.

Its a Growth Trap as Profits will grow but not eps

Its a Quality Trap as its business sounds high quality due to its brand name but its actually not.

Disc: Exited few months back at around 100rs level, Hence my views may be biased to Trap

Let me summarize problems pointed out:

Debt : First, cost of debt s very low since 7% is subsidized by the State Government. The increase in debt that you see from Q4FY15 to Q2FY16 is because they are still investing in building up 300,000 spindles. (only 33,000 spindles were installed till end of Q2). Sizable debt reduction will happen once all 333,000 spindles is in operation for at-least 6 months )

Governance problems: It is more a function of perception - currently its stock price is down from 105 levels to 67 so our perception is more negative. Had stock price jumped to 180 no one would be talking about it.

Plastic business not doing well: Yes it is facing headwinds specially price volatility sinc it is a B2B and B2G business predominantly.

I am quite optimistic on this stock. Discl: I have recently added good quantity to my portfolio

I gather from reliable sources that the mgt. plans to de-merge the textile business once the expansion is completed. This could help the balance sheet as a lot of debt too will get transferred to the textile Co. At current valuations, the stock looks attractive, though it can always get even more attractive later!! The mgt quality is perceived as poor, & not without reason!

I have a tracking position here, that was entered at higher levels. Since I do not average on the down side, the position has become even smaller! A year from now, things could look radically different though, with fall in crude helping, business getting re-structured, the Govt focus on swach Bharat etc., etc.

Can you please elaborate little on why this is Quality trap. Thanks.

See How equity has been diluted during last 10 years.

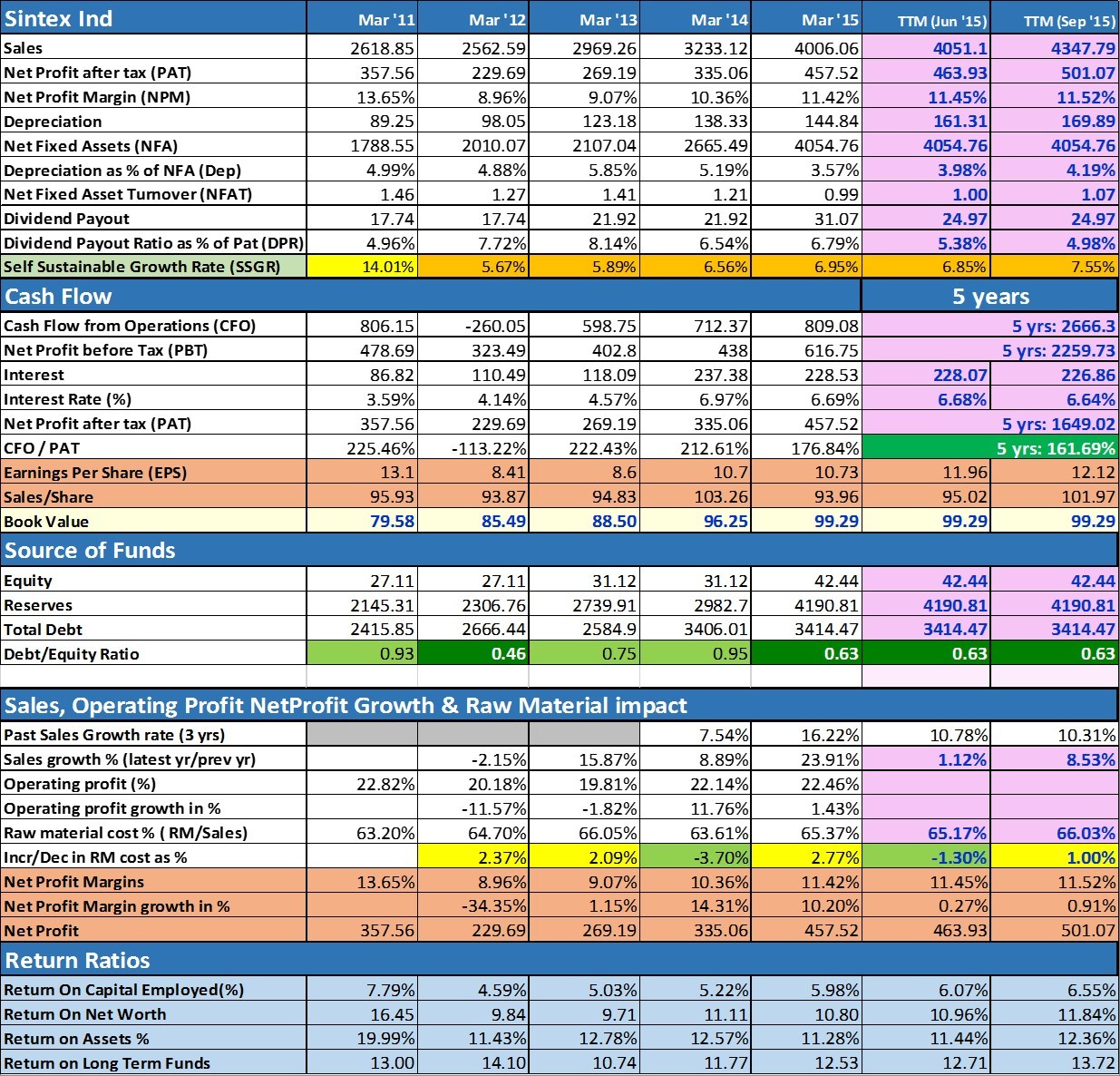

Mar 2005 Mar 2006 Mar 2007 Mar 2008 Mar 2009 Mar 2010 Mar 2011 Mar 2012 Mar 2013 Mar 2014 Mar 2015

Share Capital 18.48 19.73 22.19 27.10 27.10 27.10 27.11 27.11 31.12 31.12 42.44

Share capital went from 18.48 Cr. to 42.44 Cr. ( with out any bonus) that means they have diluted equity to more than double.

Apart from this debt has increased 10 times in last 10 years.

By hearing the name “Sintex” we first remember the brand name Sintex tanks. But company seems to have no pricing power otherwise how could this happens to branded business.

You may argue that, this all because of textile business. But even if you exclude textiles, plastic business also not self sustainable enough.

Have been tracking this stock for some time due to its cheapness. Not invested in it for below reasons yet.

For Sintex big elephant in the room is rising debt. How they plan to reduce it going forward? Can we trust promoters to put our faith in them? At the moment there seems to be adequate cashflows to cover the interest payments but the debt is still on a higher side. On top of it there are promoter quality concerns as people have mentioned. Having said that there is some value for even a crap in this country…provided you recognize it as such. If some one wants to play this then they can look at it from equity stub kind perspective. Where you invest in heavily indebted companies at very low price. Any decrease in debt boosts the equity in non-linear manner. And so are your stock returns. This is really an option valuation. if you win you win big else may lose part of your capital also. Hence Return/risk rewards of at least 5 to 1 is demanded. Not sure we have that kind of reward/risk proposition in this stock at CMP. Without such deal I think you will be taking too much risk for a reward not commensurate with this risk…especially when there are other attractive opportunities around.

One more huge equity dilution through FCCB.

Disc: Exited few months back at around 100rs level, Hence my views may be biased

Yes agreed - management has a horrific record of capital allocation and they just keep on piling more debt on their balance sheet.

But the new FCCB terms and conditions are fine for now - Minimum Conversion Price of 93 and no equity dilution can take place before at least 2 years (2018) - although another 15-18% equity dilution may take it to more than 51-52 crores by 2022.

Sintex has reported higher YoY PAT for 6 consecutive quarters now and even with the 40% equity dilution over 14-15 - it has still reported EPS growth for FY16.

At M.Cap/Sales - <.5 and P/E of 5.5 - market is taking the mickey out of this company/promoters.

Recently re-read the famous line which seems perfect for Sintex based on its current business outlook + financial position - ‘Markets can stay irrational longer than you can remain solvent’ - let me also see how long markets can keep ignoring higher earnings YoY.

Btw - in no way am I implying that this is a huge wealth creator or has maginificent prospects - but in my view even with it’s high debt and very average capital allocation skills of promoter - this should easily deserve a 8-10 P/E or it should start reporting no growth PAT for the next few quarters…then I will re-evaluate my decision)

Disc - Invested for more than 2 years and views are completely biased and based on holding period. I’m personally offended at Mr.Market’s behaviour (yes - they say we should not take things to ego/personally when dealing with the stock market - but I know the amount of capital I’ve invested is reasonably low compared to my earnings ability over my career (and yes I know it compounds YoY and etc etc…), so I’m fine with suffering for some more time - let’s see how irrational this market is)

Value investors shouldnt even look at this stock. If you wish to find out about the quality of management, try to dig a little into related party transactions and where all they have put companies money?

Companies appetite of debt is never ending. As soon as FCCB conversion is over you find their long-term debt has increased.

Not investing. Not even looking.

Completely agree - I have no buy transactions in the last 1 year. Neither am I recommending getting into bed with this business/management - in fact it’s a very poor business which requires high capital expenditure and generates average return on capital employed.

But I believe ‘stock prices are slaves of earnings’ - and the stock price is showing the complete opposite of that - unless of course the earnings are not real (dividend should put that to rest) or markets can already foresee very poor returns from it’s new textile expansion/business.