Results …

Results looks bad but silver lining is someone is ready to invest 1500 crore in this loss making company which is huge. Being a largest sugar company it has a drawback of minimum utilization, as many of its running cost would be fixed so above some capacity utilization only it will become profitable. Ethanol sales is encouraging though lets see how it pans out in future.

Some more inputs on this sector as a whole in this interview.

1 Like

Shree Renuka Sugars AR21 summary.

- We are engaged in manufacturing of sugar, generation of power and production of Ethanol and other-potable grade Alcohol

- The company started operations in 1998 with one sugar mill in Karnataka. At present, it operates six sugar mills in India and two world class port-based refineries with a total refining capacity of 1.7 million tons per annum (MTPA).

- We have pioneered the concept of operating sugar manufacturing assets in India on lease and ran power projects at third party mills on BOOT basis. We are also one of the first companies in the Indian sugar industry to have ventured into the business of sugar refining, Renuka Sugars has been at the forefront of driving growth through innovation.

- Plant & Capacity

- 2 Refineries in the state of Gujarat (Kandla) and West Bengal (Haldia).

- 6 State-of the-art sugar plants in the states of Karnataka (4) & Maharashtra (2)

- Refinery 5500 TPD capacity. Kandla 3000 TPD and Haldia 2500 TPD

- Sugar 37500 TCD. Athani 10,000 Munoli 10,000 Havalga 7,500 Panchaganga 6,000 Raibag 2,500 Pathri 1,500

- 3 Distilleries located in states of Karnataka

- Total capacity 720 KLPD. Athani Distillery 300 Munoli Distillery 120 Havalga Distillery 300

- 262 MW Cogeneration power plants located in the states of Karnataka, Maharashtra, Gujarat and West Bengal

- Raibag and Panchaganga sugar plants are leased.

- Ajinkyatara and Panchaganga cogeneration plants are on BOOT basis.

- Sugar

- The revenue from the sugar segment amounted to Rs. 53,137 Mn, accounting to 80.01% share of the total revenue mix in comparison to Rs. 42,223 Mn in the previous year

- Our refinery in Haldia restarted after a gap of 2.5 years.

- Total raw sugar melted at the Kandla refinery stood at 1,201,447 MT and 116,927 MT in our Haldia refinery.

- We initiated supply of consumer products from our Haldia refinery to meet the supply deficit in the North Eastern region of India

- Our consumer pack business registered 29% sales growth owing to shifting consumer preference towards branded sugar

- We occupy 22% market share in the branded sugar segment.

- Our consumer sugar business under the ‘Madhur’ brand has continued on its growth journey during FY 2020-21. We expanded our footprint in the northern and eastern parts of the country during this year.

- The refinery business of Renuka Sugars is an exportoriented business. The company imports raw sugar and exports white sugar to different parts of the world. In the year 2020-21, the company relied on procuring raw sugar from the domestic market to substitute its imports

- Cogeneration

- Through our cogeneration power plants at the mills, we use bagasse (the by-product of sugar manufacturing process) to produce power. A significant percentage of the power generated is captively consumed within our plants while the remaining power is sold to the state electricity grid.

- 262 MW Cogeneration power plants located in the states of Karnataka, Maharashtra, Gujarat and West Bengal

- Munoli 34 Havalga 38 Panchaganga 30 Ajinkyatara 24 Athani 76 Kandla 45 Haldia 15.

- Total 529 million kWh of power generated, out of which 53% was captively consumed and 248Mn kWh was sold to the state electricity grid.

- 77% of our cogeneration process is based on renewable energy ensuring significant reduction in GHG emissions

- The revenue from the segment amounted to Rs. 4,301 Mn, registering 6.4% share in the total revenue mix in comparison to Rs. 3,722 Mn in the previous year

- Ethanol

- We are one of the largest suppliers of ethanol to oil marketing companies in India.

- Through our distilleries, we manufacture 3 grades of Ethanol i.e. Rectified Spirit (RS), Extra Neutral Alcohol (ENA) and Absolute Alcohol (AA) or Ethanol (used for fuel blending).

- Through our subsidiary - KBK Chem-Engineering Pvt. Ltd., we provide turnkey distillery, ethanol, certain sugar process equipment and biofuel plant solutions.

- The revenue from the segment amounted to Rs. 7,014 Mn, accounting for 10.56% share of the total revenue mix, as compared to Rs. 4,712 Mn in the previous year

- 136 Mn liters of ethanol produced – highest ever production, as compared to 110 Mn liters in the previous year, registering a growth of 23% YoY.

- The plants are running at 100% capacity utilisation

- We also operated with expanded capacities and used incineration boilers to burn spent wash, enabling us to save a large amount of external fuel.

- Increase in ethanol supply also rose 90 Mn litres to 120 Mn litres, an increase of 34%

- We foresee robust growth opportunity in the Indian Ethanol market going forward, owing to increasing demand and strong policy support.

- Thus, we are investing around Rs. 6,500 Mn to expand our ethanol capacity from 720 KLPD to 1400 KLPD.

- The additional capacity is expected to be added by October 2022.

- We endeavour to become a green energy company with a focus on production of bio-fuel ethanol.

- The expansion will help us become one of the largest ethanol producers in India.

- We employ 1979 employees

- The sugar output in India is estimated to be 30.5 million tonnes during the sugar year starting 1st October 2020 to 30th September 2021, which is an increase of approximately 11% YoY against previous year output. The increase in output was due to improved weather conditions as well as increase in cane acreage in southern and western regions. The domestic consumption for the current year is estimated at 26 million tons along with 6 million tons for export under the Government’s MAEQ program. We expect the carry over of stock of sugar at the end of the current year at around 9 million tons.

- The Government has increased the price of ethanol extracted from sugarcane juice from Rs. 59.48 per litre to Rs.62.65 per litre. The rate for ethanol from C-heavy molasses has been increased from Rs. 43.75 per litre to Rs. 45.69 per litre and that of ethanol from B-heavy from Rs.54.27 per litre to Rs. 57.61 per litre.

- Against LOI quantity of 3,465 Mn litres, the total contracted quantity stands at 3,212 Mn litres. India expects to achieve a blending percentage of 8.5%, with states like Uttar Pradesh, Maharashtra, Karnataka, Uttarakhand, and Bihar achieving even higher blending percentages of up to 10%.

- The ethanol demand has been estimated around 10,160 Mn litres by 2025, based on expected growth in vehicle population. The current ethanol production capacity in India is of 4,500 Mn litres derived from molasses based distilleries, and 2,600 Mn litres from grain based distilleries. The same is proposed to be increased to 7,600 Mn litres from molasses-based distilleries and 7,400 Mn litres from grain based distilleries. This will help to produce 10,160 Mn litres of ethanol which is required for EBP and rest for other uses.

- Financials

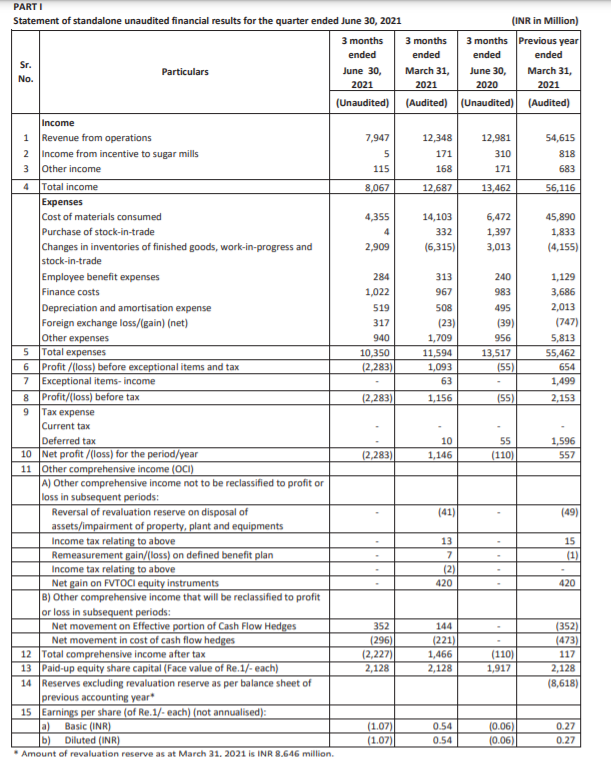

- Our total revenues grew by around 21% to Rs. 56,116 Mn, whereas our EBITDA was recorded at Rs. 5,606 Mn, driven by growth in exports, ethanol and our consumer pack – Madhur.

- Revenue growth was mainly driven by increased sugar sale of Rs. 7,157 Mn with a value growth rate of 18% and increased ethanol sales of Rs. 2,302 mn with a value growth of 49% over last year.

- After consecutive seven years of negative PAT, the Company recorded a positive PAT of Rs. 556 Mn for the year, driven mainly by improved operational performance and savings in interest costs.

- Our standalone borrowings, as on 31st March 2021, and stood at Rs. 37,859 Mn vis-à-vis Rs. 21,912 Mn the previous year. The Company raised external commercial borrowings from the promoters to restructure its NPA classified financial instruments, term loans and working capital facilities, loan for ethanol expansion and fresh working capital facilities.

- Consolidated debt is Rs. 4600cr out of which 2155 cr is from promoters.

- Inventories increased by 42% from Rs. 16,544 Mn in FY 2019-20 to Rs. 23,544 Mn in FY 2020-21, mainly due to increase in refinery stocks.

- During the year company issued 21,16,70,481 shares at Rs. 8.74 per share and raised Rs. 185 cr from promoters.

- Company redeemed 4,28,08,858 0.01% Optionally Convertible Preference Shares (OCPS) of 100 each and 7,43,88,207 0.01% Redeemable Preference Shares (RPS) of 100 each which were allotted to the lenders pursuant to debt restructuring exercise undertaken by the Company, by converting the part of the loans facilities availed by the Company from the lenders.

4 Likes

@harshitgoel How do you look at recent development in this stock?

Also attaching latest Rating update from India Rating for latest updates and a must read for everyone. I think it is adding a lot of info to the latest AReport.

https://www.indiaratings.co.in/PressRelease?pressReleaseID=55918

AR 2021

AR 2020

Any idea what happened to Khopoli based distelleries?

No one mentioned this from latest AR. They have already expnaded 30% in two of their Distilleries. We have to di deeper to look at these triggers to activate in future.

3 Likes

Investor Presentation (after a long time!). Also investors are meeting the comapny over a course of 4 days from 22nd Novemeber onwards. There’s got to be something happening!

3 Likes

A good view in to sugar sector and may be particular to Renuka Sugar. There would be a huge boost to Gross margin going forward and also Ethanol plants would be run for 270-300 days. Also Renuka is now operating AT 900 KLPD capacity which is huge in terms of revenue realization. Lets have our fingers crossed for bumper recovery in earnings and secularity in Sugar sector as a whole.

Disc: Investec in Renuka Sugar so may be biased

2 Likes

Where can I check what is the SRS daily/monthly/annual Ethanol Capacity now and what would it be after Capex?

Thanks

Its is in above Interview itself Bloomberg one.

Last year Capacity was 720 KLPD

Current operational 900 KLPD

Next year Oct-22 planned 1500 KLPD

(all figure are approximate)

Also going forward Ethanol production can be done for full year due to change in Tech.

2 Likes

Courtesy: Timesnownews.com

- Petrol demand on rise. Ethanol blending current level 10 and would go to 20% by 2025.

Ethanol is blended along with petrol. - Next crushing season, the ethanol capex played out would be commissioned.

- Sugar prices remained stable unlike other commodities which rocketed. Hence downside

is not much.

2 Likes

Renuka Sugars Ethanol Update

3 Likes

Shree Renuka Sugars has announced that it has commenced commercial production of ethanol from the expanded capacity [Athani (from 300 KLPD to 450 KLPD) and at Munoli (from 120 KLPD to 500 KLPD) plants]. -Announcement dated 29th March 2023

The Roadmap for Ethanol Blending in India 2020-25,prepared by an inter-Ministerial Committee, estimated ethanol requirement of 1016 crore litres to achieve 20% blending targets in ESY 2025-26. The current ethanol production capacity is 1364 crore litre.

1 Like