Hiteshji, Nice observation. It has given almost similar breakout in nov.'15

and again in June ‘16, but failed to sustain. Let us hope this time it

sustains crucial level of 16. It seems if Brazilian restructuring gets

delayed for one reason or other, we might see repetition of Nov’ 15 and

June 16 pattern. If level of 16 is taken it is fairly good indication that

Wilmar’s entry ( allotment price 16), has given instant boost and price

reaction. But long term support is still lacking. Well for long term

investor like me, just interesting event only. Let us hope Brazil

complications are resolved fast. But i guess things are slower in Brazil

even compared to our country. Stay invested on long term basis for multiple

return!

Thanks nirav for the detailed write up.

For the immediate short term 5 Sep remains a crucial date when the bids for the Brazilian co auction open up. If that is delayed or fails, then there could be a lot of disappointment. Two reasons why someone would be interested in buying a big sugar facility in Brazil are, first the upswing in sugar cycle and secondly the recent appreciation of Brazilian currency wrt USD. Plus such firesale might provide assets on the cheap.

Brazilian lenders have agreed to take a haircut of upto 70% as a part of restructuring. (as per Narendra Murkumbi interview). And all the proceeds go to the lenders and the Brazilian operations become debt free.

The other more interesting part of the thesis is of a longer term in nature. With Wilmar putting in a lot of money, post all the restructuring and conversion of instruments, it will end up with 38% stake in the company. If this happens then the company can be viewed in a different light with a very strong promoter at the helm.

The continuation of the upswing in sugar cycle remains an integral part of the thesis.

In the past, change of management has provided good opportunities to pick up winners e.g Spicejet, USL etc. In each case there were a different set of problems faced by the companies but once the managements changed things improved.

And if the whole restructuring suceeds, there can be a few more things which could also fall in place for the co bcos usually when things go wrong, there are multiple things which go wrong and reverse is also true. As per the fy 16 AR, renuka is one of the biggest players globally in sugar sector so if things turn there could be a big swing.

disc: invested as an opportunistic bet.

5 Likes

Hi… Anybody has any idea about auction proceedings…

Hi During current run up of sugar stock is there possibility of shree renuka to turn around. May be ethanol blending can help . Anyone tracking co

@Tejas_Vora Brother, I am one of those who has burnt his fingers in the Shree Renuka Sugars story during years when it was every investor’s darling. This was our tuition fee from the school of stock market. Learn from our mistakes, try and stay away.

Today even if you give me free money, i won’t put it in Shree Renuka Sugars, so Valuepickr may not be the right platform for this question

Read the thread “My mistakes in stock market” for more information"

3 Likes

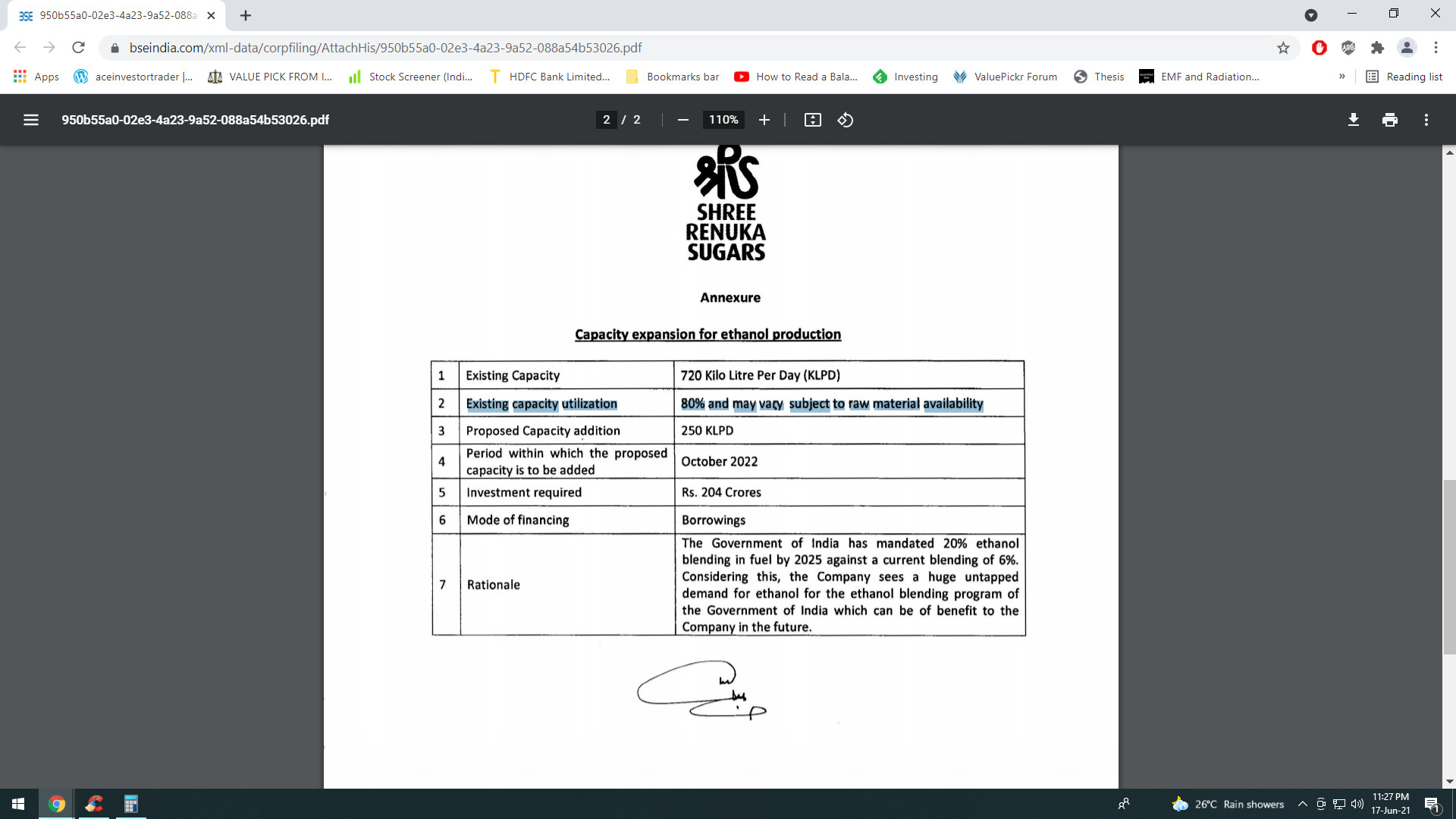

As per an announcement the Ethanol capacity is being used at 80% capacity

Also as per Sep Quarterly results the margins have also improved with capacity utilization. My rough calculation gives me 270Crore as Distillery revenue and PBIT 50 crore for this quarter and can turn this year a net profit year.

One more trigger in this stock is debt reduction the amount of debt reduction will add to Market cap only so only debt reduction by management will be price accretive for investors in this counter.

Disc: Holding

2 Likes

Distillery revenue and profit are as same as my calculation was. Annual results are to be read carefully

Capacity would be the largest or we can atleast 1.5 times of the nearest competitor Globus Spirit though timeline of execution will be key.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/5f3fb5b4-83fd-40e9-b6c2-fb5b074c0e1e.pdf

I will add some more points after reading carefully. Results are in line with expectation and are bound to improve due to strong parentage my only concern would be Equity Dilution from here onwards.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/fddee0f4-a622-49d4-9728-3f28a6490a67.pdf

1 Like

Dear Ravish,

Thanks for this update. Have been a shareholder since 2010 n the wait has been too much i would say. Was down 80% from my price in 2020 but luckily i had faith in new mgmt of Wilmar and inevitable turnaround nad therefore bought more at 9 rs n averaged all my holdings to rs.15. the latest results give an idea that the annual EPS from this quarter should be around 3 atleast considering the improved sugar price and ethnol capacity expansions going into 2022. And now with this sector not being tagged as cyclical and getting more of serious huge funds from MFs n FIIs, my guess is that decent sugar companies should command an avg PE of 20 going forward and this makes a case for SRS to be fairly valued at minimum 50 in 2022 once debt from the new ECBs is also reduced. Whats your opinion, and do you think it makes sense to average more onto at rs.30 level for the longer term story n potential. Thanks!

1 Like

Any idea why the payables are so high?Cash flow statement shows an outflow of payables of 1367 cr. Also, the new borrowings from the parent was at what % and why the need to raise 2241 crs as borrowing? Why is the focus not on repaying debt, as the co will further do an outlay of 400+ cr to increase the ethanol capacity.

1 Like

I can’t tell you what to buy and at what price but I can give pointers about my thesis on Sugar, Ethanol/Distillery and power investment or particularly in Shree Renuka.

- Wilmar as a owner is a big plus and it’s recent action of capex, debt reduction ,helping in manging working capital and other positive steps are commendable. It also shows that how big this opportunity is. Also owner of the biggest respective capacity they will make most of the profit from the pool.

- My concern is their capacity are in Maharashtra and Karnataka as there is issue with water availability and may affect sugarcane output but if we go by mansoon prediction for current year and good rainfall last year , we should be in comfortable position for rest of the season. Also possibility of equity dilution.

- Export subsidy plus high international sugar price will be EPS accertive in future.

- It has sugar mill and sugar refining capacity which can be used at maximum capacity if sugar price go up.

- Ethanol as a theme is gaining momentum and industry related to it is in all time high confidence pls watch video

Is Ethanol A Big Money Making Opportunity? | Bazaar Open Exchange | CNBC-TV18 - YouTube

Experts Discuss The Need For Ethanol Blending In India | Commodity Champions | CNBC Tv18 - YouTube - Hurdles to implement Ethanol blending targets are being removed by Govt. proactively.

- Even when price of crude went down last year the price of ethanol was not touched a strong statement to be made.

- It’s a win win situation for Farmers, Sugar Producers, Ethanol plant manufacturers, Government and to Taxpayers.

- I usually don’t invest in Govt regulated biz but in recent past wherever the Govt intervened by creating new policy likes of DBT , Nal se jal, Solar pump’ KUSUM scheme, Home Finance Subsidy, PLI schemes for industry and many more have not faltered much and gave outstanding returns.

- If we look at this story the margins are very high and payback period of investment is low. So the cashflow can come to us very fast.

- Whole sector is under owned by FIIs and DIIs.

- Sugar refining is negative working capital which is a huge positive to earnings.

- As per the credit rating report the support of 300MUSD is payable in 2025.

4 Likes

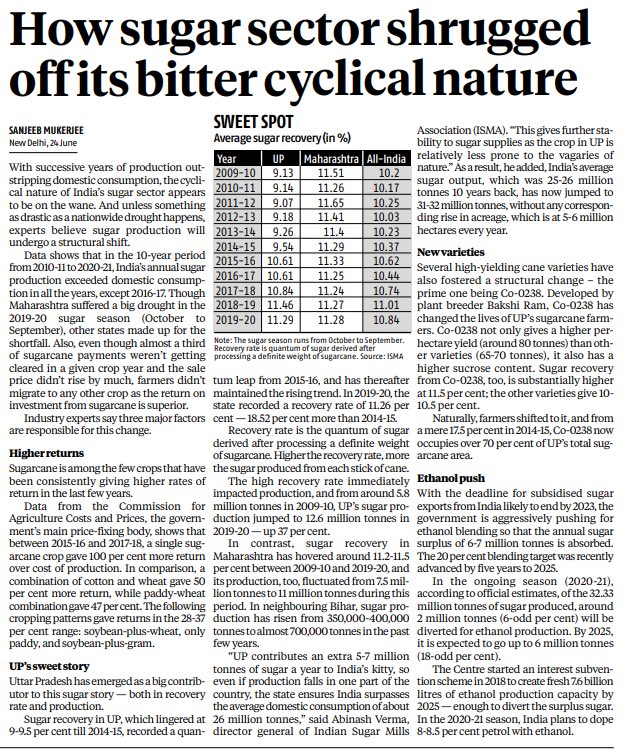

Nice article on how Sugar industry is going thru a structural change .

Discl : Invested in Shree Renuka Sugar and also Balrampur Chini

1 Like

Dear ravishji,

My congratulations for Excellent coverage and comprehensive analysis of what and where Shree renuka Sugar stands today and where it might go.

If i summarize all your 13 points, it is pointing toward one conclusion and that is Shree renuka Sugar has tremendous scope of growth in short, medium as well as long term. Worst is behind us with full credit to Wilmar in shelving out substantial amount of debt and turning out this great company.

As far as portfolio is concerned, it is time to build long position as stock is still available at throw away price. Just take the position before re-rating starts and as you have rightly noticed whole sector is under owned by FII/DII.

With the unstoppable bull run they will be short of good stock and it is time they will be looking for strong long term player like Shree renuka.

Debashishji, Nice article. Thanks for sharing

Dear Mehnazji,

It is long long time interacting with you. Awaiting you valuable comments. Ongoing bull run in my favorite stock has re-kindled my confidence in technicals being more powerful indicator than fundamentals. I am extremely joyous with the way Shree renukaji is batting in full form.

Awaiting eagerly for your views.

Thanks a lot dear Ravish for a brilliant point to point analysis. Really appreciated!

Thanks @ravish ji for explaining the story of shree renuka sugars. I have been holding this from 2010 when sugar as a household item was quoting on high price and similarly sugar stocks were in sky. I was very naive at the time but have learnt many things about market and industries from that time on now, still naive though.

Coming ot SRSIL, I felt disappointed with Murukumbi but only stuck due to Wilmar remaining and then taking over the company. Now It looks like the old days are over and SRSIL might be on to new orbit, just have to follow the results and keep the conviction.

Thanks

Disclosure - Invested since a decade and planning to hold for atleast another decade now.

1 Like

QIP will be a booster to Shree Renuka Sugars image. I m positive for long term. People may be skeptical about Ethanol theme at large due to Electric Vehicle but They must consider that EV need a huge infra for meaning full impact on fuel demand.

1 Like

Result Out…Bad Result QoQ and YoY

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=f1cce0bb-3625-4473-9cf0-342619ffe3e1

Fund Utilization Statement

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=242a9a61-fbf3-425f-bd30-de37a36e98fd