1 Like

Biologicals in india are not a good business. Adalimumab is a low margin business with heavy competition. This will be good if they get into Exports. But then registrations are lot more expensive.

Don’'t think if people in biologicals in India are making big money. Especially MABs

People only start believing the story as soon as the sector/stock starts moving up until then everything remains Uncertain, Risky & Less Rewarding. Usually Bargains are opportunity to buy but unfortunately in stock markets that’s complete opposite, Bizzare. Coming to your point for Adalimumab they have developed High Concentration Adalimumab and it’s 1 of the First company to do so, also Margins are High Double Digits with Huge runway for Growth (TAM), So don’t agree with your point, let time tell.

1 Like

Sure.

I am talking of product, not of company. It may still do well.

Its mostly tender / institutional business (all MABs - except the patented ones of MNCs) sold at heavy discount to MRP.

Agree with following point.

“People only start believing the story as soon as the sector/stock starts moving up until then everything remains Uncertain, Risky & Less Rewarding. Usually Bargains are opportunity to buy but unfortunately in stock markets that’s complete opposite, Bizarre.”

Let me share one point to validate your point. Now, lets see how many rosy pictures are shared.

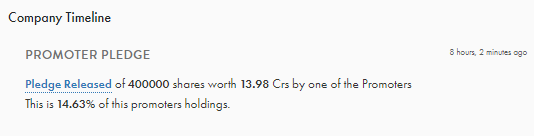

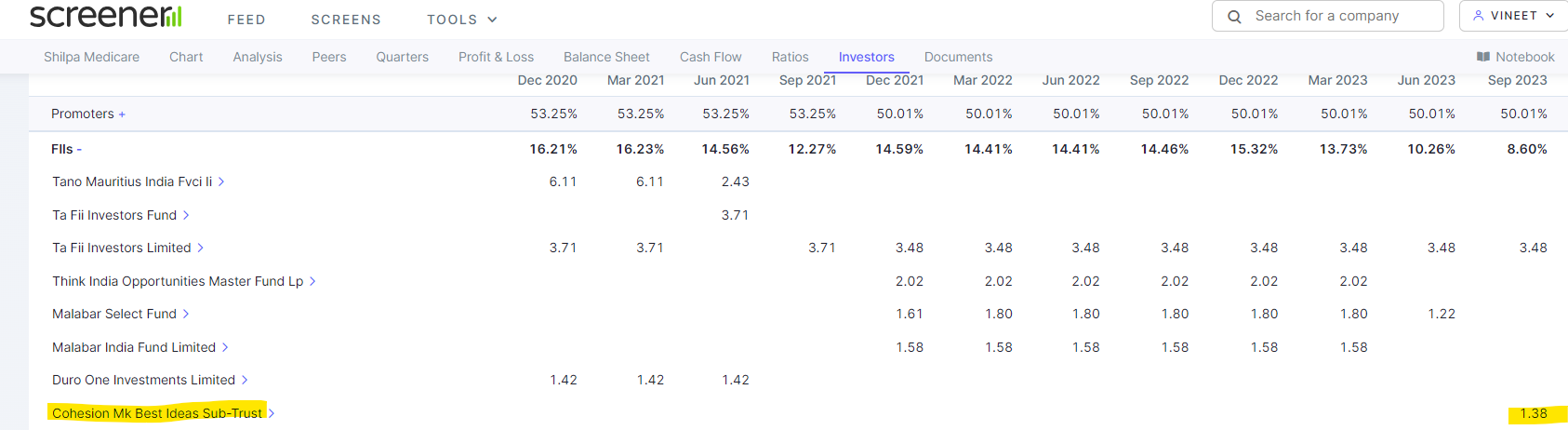

Madhusudhan Kela has bought 1.38% stake in company using its proxy company. Please search in latest FII holding in Sept 2023.

Disc: invested at 240 levels

1 Like

Hey Vineet, Ya saw that in September Holdings earlier MK also invested through QIP at 570-575 levels and now he has added more I believe or just transferred, not sure.

Few Triggers:-

1- USFDA Lifting the Import Alert ban this would result in recovery in their formulations exports in US can bounce back drastically

2- Launch of their Recombinant Albumin Drug in which they have CONFIDENTLY invested also, there is shortage of this drug all over the world with Huge TAM. This product has a 9 billion$ market.

3- Easing of input costs in their API business which has already showed some signs in last quarter.

4- Launching of their Aflibercept - a complex product in the ophthalmic range. Starting phase-3 trials in India. Trying to develop this particular product for the global market.

5- They have started focusing on Deleveraging which will result in decreasing Interest cost and inflate profits and cash flows.

6- Capex cycle has been already been stopped apart from few small amt of capex left for Albumin.

7- They are also working on developing APIs which are now 100% imported so china+1 can work here.

8- R&D expense will be rationalized without compromising new developments. which will have a positive impact on P&L .

9- Overall company has strong pipeline for for ANDA, NBE which will be soon reflect in numbers.

Invested at 232-235 levels

1 Like

Exactly !!

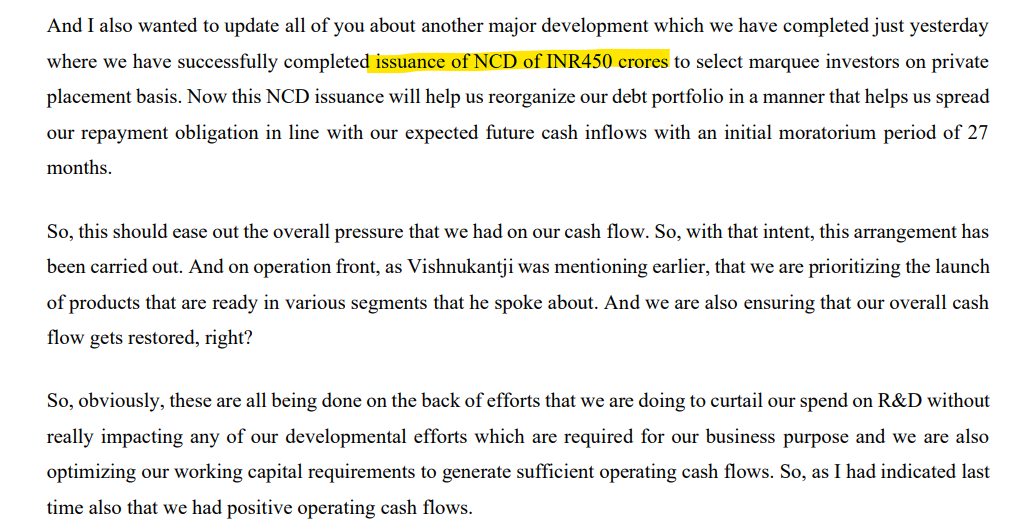

Only thing which was gating company’s turnaround was Debt and Cashflow. With NCD placement, they have resolved for sometime. Lets see how the hypnosis go .

Snippet from Q1 Fy24 call :

2 Likes

Also, Vineet let me know if you any idea on the recent share pledging which has been increased to 90% not sure if promoters has participated in NCD by pledging their shares? is that so or do you know why?

one more point:- Q1-24 Cashflows were 70 crores so that is great start if the same trend continues for next 3 quarters it’ll be somewhere around 220-230 crores in this FY of Operating cash flows i.e. P/OCF was at around 8-9 times at 240-250 levels with market cap of 2100-2200 crores

1 Like

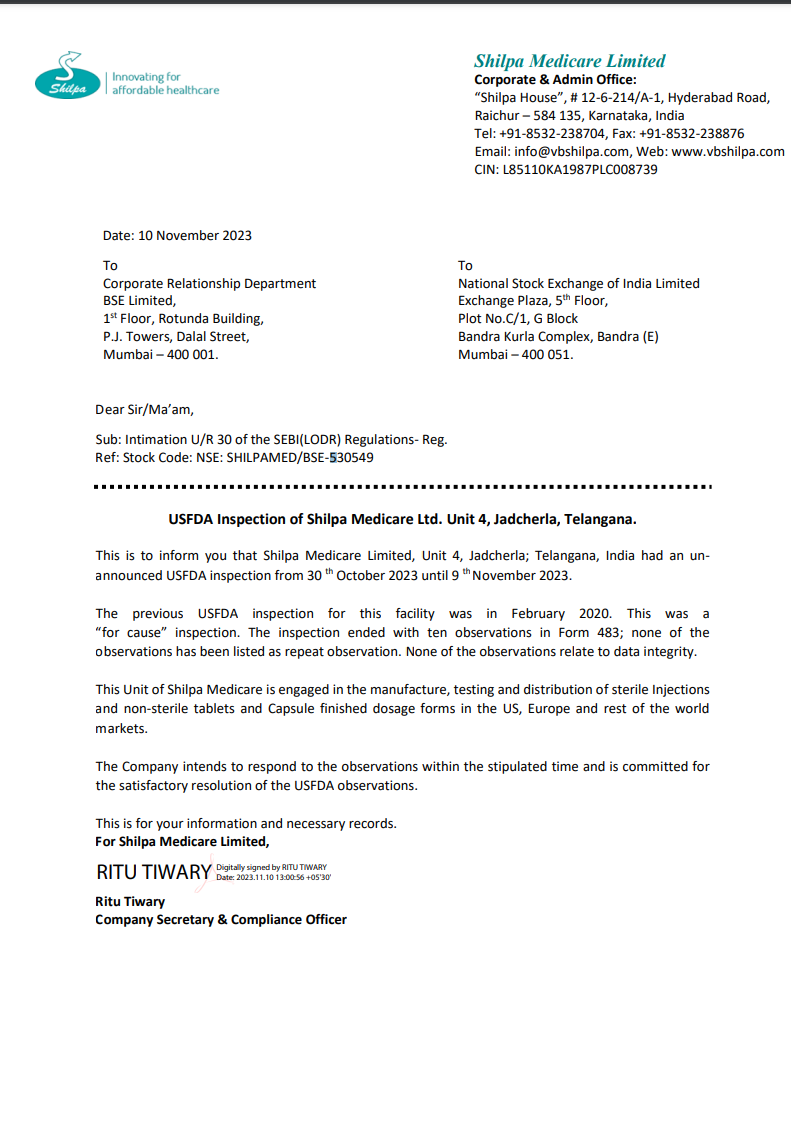

Shilpa Medicare notified about a recent unannounced inspection by the USFDA at their Unit 4 facility in Jadcherla, Telangana. The inspection took place from October 30, 2023, to November 9, 2023. In the previous inspection in February 2020, there were ten observations in Form 483, but none of them were repeated, and none related to data integrity.

I think, Promoters pledged shares to avail NCDs.

In Q1 call, management shared that they pledged share to avail NCDs at 12% interest for 1 year loan. They were confident that they can resolve Cashflow issue within 1 year.

With Q2 result, this statement make sense. Shilpa is one of the few Pharma company which is showing Topline and PAT growth.

1 Like

The Managing Director reports on the company’s recent achievements, which include regulatory approvals for new products and facility inspections with positive outcomes. They emphasize efforts to streamline R&D spending for cost savings without compromising niche product development. Additionally, the company has launched a high-concentration Adalimumab product in India and initiated phase 1 trials for recombinant Albumin, signaling their expansion into biological offerings. The construction of a large-scale fermenting facility is in progress and expected to be completed by March 2024.

Operational Efficiency : The company has been focused on improving operational efficiencies and strengthening its overall business operations. These efforts have been successful, leading to continuous improvements in the company’s performance.

Quality and Compliance : The Jadcherla facility has recently received approvals from various regulatory authorities, including UAE GMP approval, Australia GMP approval, and ANVISA Brazil approval. Importantly, these approvals were granted with no observations, indicating high quality and compliance standards. The USFDA inspection, conducted “for cause,” concluded with 10 observations, but notably, none of these observations relate to ‘data integrity’ or have been listed as ‘repeat observations,’ which is a positive outcome.

API Business : In the API business, they have successfully completed a regulatory audit by PMDA Japan, with no major or critical observations for their API facility. Their Contract Development and Manufacturing Organization (CDMO) business has been well-received by customers and is on a growth trajectory. Furthermore, they are exploring products in the non-oncology API segment that have high growth potential or can serve as import substitutes.

Biological Offerings : On the biological front, the company has launched a high-concentration Adalimumab product in India under the brand name “ORIADALI™.” This product is aimed at enhancing patient comfort in treating Rheumatoid Arthritis. Leveraging the approval and launch in India, the company plans to expand into international markets with this product. They have also initiated phase 1 trials for recombinant Albumin, representing a significant step in this niche opportunity. Additionally, the construction of a large-scale fermenting facility is underway and expected to be completed by March 2024.

3 Likes

The previous USFDA inspection for this facility was in February 2020. This was a

“for cause” inspection. The inspection ended with ten observations in Form 483; none of the

observations has been listed as repeat observation. None of the observations relate to data integrity.

Why the Company is so poor in terms of FDA compliances… Pathetic

1 Like

We had received fifteen 483 observations at the closeout of FDA inspection on February 25, 2020. The Warning Letter received on 10 Oct 2020 had specifically mentioned two citations - (i) inadequate handling of OOS and (ii) inadequate handling of market complaints, including failure to file FAR within stipulated time.

Common reasons for a “for cause” audit include:

- Specific complaints to the FDA

- Concerns about Stakeholders involved in the research process

- Significant issues or termination identified during research activities

- Multiple deviations

- FDA identified events of special interest

“For-cause” inspections can be particularly stressful on all individuals involved, so it is best to take a proactive approach and ensure that you are always prepared for a visit by the FDA. There are several ways to ensure you are prepared for both announced and unannounced inspections, including conducting regular trainings on best practices for staff and staying up to date on the current regulations/guidelines/expectations. Teams should identify key roles and responsibilities for company personnel and establishing a contact tree if an inspector were to arrive at your facility unexpectedly.

Not only should all parties strive for compliance, but also for showing off quality implemented throughout the work. You can do this by maintaining up to date documentation, developing an effective and robust quality management system (QMS) and implementing a thorough inspection readiness program.

A gap analysis is an excellent way to identify gaps and weaknesses in procedures and documentation as well as highlight areas for training. The best way to ensure that your firm is inspection ready at all times is to be proactive in preventing “for-cause” inspections and make the reactive approach the “not to be”.

3 Likes

Got it, thanks and Do you think it’s fair to compare this company with Biocon only if we specifically take their biology business and compare with Biocon, so if you see Biocon being one of the first, well established and well experience player isn’t doing well in their biologic division the business hasn’t done anything since a long time even though they are into this biologic segment and had few launches since last 3 years even though market hasn’t been rewarding it very well or it’s not been well received (I know their fundamentals aren’t improving due to huge investments required upfront and a long gestation period before they could even Monetize them) by market or investors even today investors are shying away from this space even when there is huge potential in the future considering the numbers of expiry of patents, High Margins, TAM, high entry barriers due to patent or high R&D time and expense. why do we think markets will be rewarding SHILPA Medicare well or even better than Biocon given that they are the early movers with many ANDAs in the pipeline.

Is it fair to compare just on their Biologic business or are we being quite optimistic on their growth in their biologic business?

Appreciate your thoughts on this.

Concall notes for Q3FY24

- 1 oncology product to be launched in April

- Import substitute

- Some addition in non-oncology by Dec 2024 – will add revenue addition

- 1 CEP of peptide product filled in Europe

- Very optimistic about API business

- Biologics has been a pain point in last 4-5 qtrs

- +ve ebitda this quarter

- Positively focusing here

- Aflibercept – phase 3 studies to start in April

- 1 yr study

- Rs 4 cr receivable provision

- Rs 146 cr capex of which Rs 117 cr invested in Albumin capacity

- Total investment made in Albumin – Rs 300 cr +

- More 40 cr required

- Phase 2 study to complete by FY25 end

- Polymer revenue in 2-3 yrs –

- This yr 15 cr

- 2-3 yrs 100 cr

- Biologics –

- 1st phase to complete by April ( Value = 6 cr) phase 2 also 6 cr

- Dip in oncology revenue because of remediation reasons

- Transdermal & ODF – Rs 200 cr investment

- Breakevens in fy26

- Biologics : EBITDA + ve next qtr

- Targeting to reduce debt significantly in 2-3 yrs

- They said current capex in Biologics and Transdermal is underutilised

- Not possible to share utilisation numbers as there are several units, doing different products

- For revenue potential of capex – they said its too early to comment. They’ll share numbers when products are near launch

- Albumin will take at least 1.5 yrs from now. Its about to enter phase 2

- The products are in short supply with high demand

Would be better able to analyse the company if get the utilisation numbers and potential of last capex. – the one it did in last 4 years.

Looking forward to your contribution.

12 Likes