Good results from Shilpa http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/257f5a7a-f45f-40b6-ae1b-8ae012333004.pdf

13.76 EPS for FY 17 vs 13.6 EPS for FY 16 for a stock trading at 50 PE.

Revenue of 786 cr vs 722 cr…yoy less than 10% growth

Very good!

1 Like

The consolidated results were quite disastrous considering the permanent diminution in one of the foreign subsidiaries. I am quite disappointed with the results & have sent a mail to CFO. I have exposure & this is the only stock in my portfolio :(. Standalone was quite decent. This again calls in question on the role of subsidiaries.The valuations for such a results looks quite steep. I believe that top-line growth should see a meteoric rise starting Q1 2018. I am giving this stock one more year to see how performance pans out. I have been holding for the last 3 years.

Did you check the consolidated #s? PAT has gone down - 38.84 cr vs 39.27 cr.

Can anyone provide concall schedule for the Q4?

@whipsaw you are right, I didn’t check the consolidated nos. I posted the link after seeing the standalone nos. I’m sorry about that lapse. We must wait for the concall

1 Like

Why is the stock trading at 50 pe. PE contraction happening in the pharma sector overall. Shilpa may follow them!

I dont think they have a concall scheduled, though I have requested Madhu Reddy (CFO) to hold one.I wrote to Mr. Vishnu Bhutada asking about Q4 results specifically asking about subsidiaries performance. I am given to understand that they are long term investments for medicare. I would be unable to reproduce the exact mail content (not sure If I can or not).The bright spot is that their EBITDA margins have moved higher to 30%,

4 Likes

Thanks @MONK88888 appreciate your initiative

The stock was expected to get re rated around Q3 2017 onwards but USFDA approvals got delayed and the so called growth story petered out and got pushed out to Q1 2018 and beyond. The current PE was running on the hope that Q4 2017 will make up for all the lapses. That not being the case and with pharma getting a stick , Shilpa could drop to PE levels of 35. The question are forward earnings baked in the current price or it is way too expensive . Right now looks like a throw of a coin. The positives are the capex / USFDA and the MD is someone who would not compromise short term gains for long term benefits , which we saw pan out in Q3 2017 results where couple of assembly lines were closed for sample preparation ( India Nivesh report). Also would the FII limit increase support the price .Obviously I am biased . I personally plan to hold longer and maybe buy if we see 575 levels

6 Likes

Sorry meant the MD would not compromise long term gains for short term- he is a visionary from little bit that I understand

Flattish growth in FY17; a consolidation year.

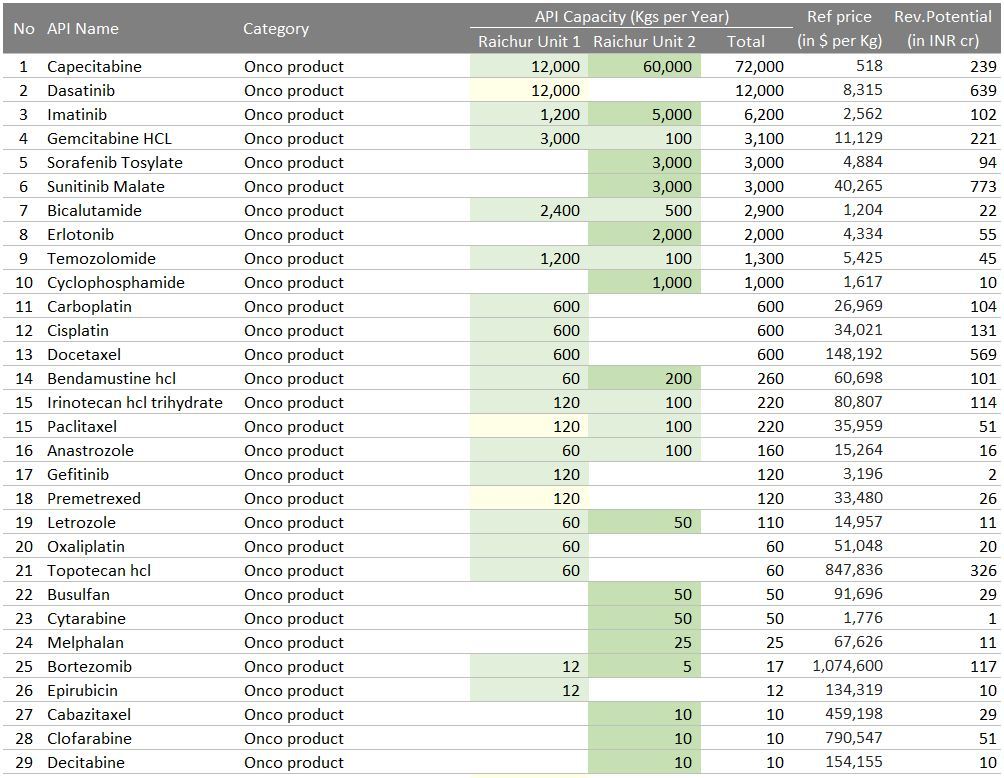

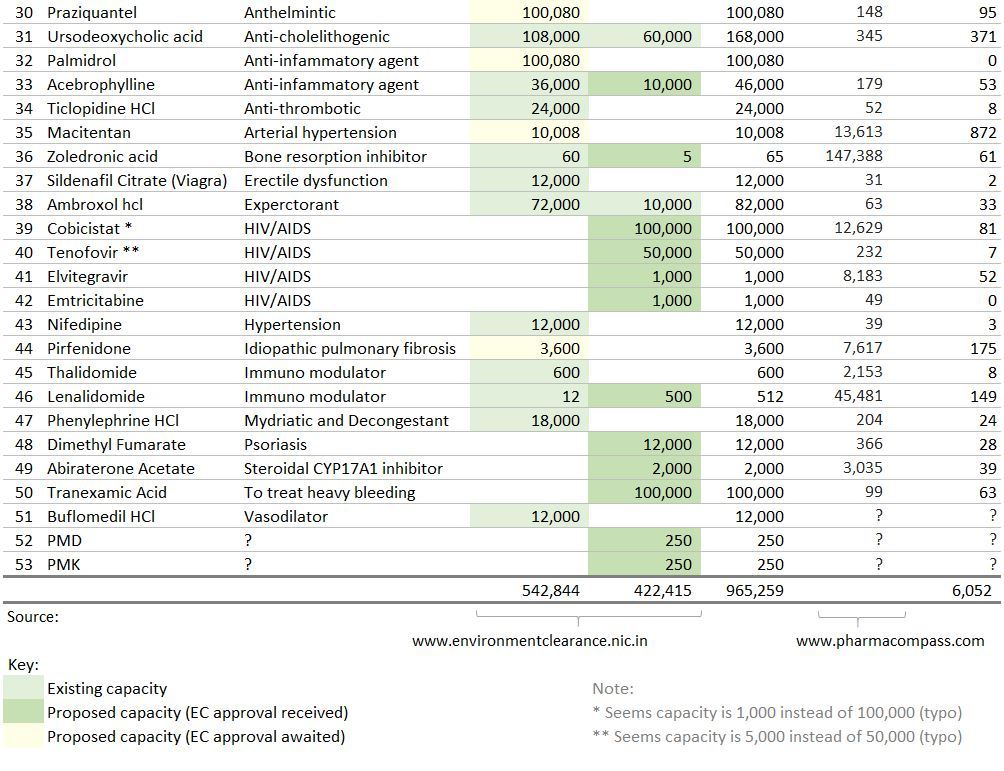

Shilpa Medicare - API Capabilities and Capacity. Some data to chew…

Shilpa API v2.pdf (207.5 KB)

Per Mr Bhutada’s CNBC Tv18 interview (Making IT Big Season 7, Episode 6)

- Oncology: 44 products are in R&D to come in next 3-4 years

- Non-oncology: 14 products are in R&D to come in next 3-4 years

- Plan to file 8 to 10 ANDAs every year

- Around 32 ANDAs are under pipeline

17 Likes

An important trend line comes around 626-628. A break there could take the scrip lower to 550-565 for further consolidation. Such a situation is comatose for the scrip & could take time to recover.Tried to post the chart

Disc: Invested

sme.pdf (89.9 KB)

1 Like

Unlikely that this stock is going to trend lower - I think investors have learnt their lessons from the way Natco got rerated (it was trading at ridiculous valuation multiples for so long until the Tamiflu revenues started showing up). Shilpa will remain at the current valuation multiples unless we see the Biosimilar dream implode.

2 Likes

Yes similar thoughts & personally dont want to let go. I see enormous potential in Drug Delivery systems & Nano technology (anyway Onco story we are aware off). I feel biosimilar would require heavy investments & changing cost landscapes is not going to help. The chart was an indication of a path it could take, if those levels break.

2 Likes

Yes, very true. What worries me is that Biocon was also stagnant for almost 5 years before they started monetizing their Biosimilars portfolio. Another issue is the absolute lack of transparency on the part of Mr. Bhutada on how much time to commercialization it will take. It is a complete black box and one of the worst examples of corporate governance where the retail investors know very little.

1 Like

Why do they struggle with printing the correct results. This is the third time (that I remember) that they have issued a modification.

“We herewith submit Modified Consolidated Financial Results for the quarter ended 31st March, 2017 as there were typographical error in the submitted financial results. We further submit that there would be no change in the profits due to said modification as the modification relating to the grossing up of excise duty in total income and charging as expense.”

1 Like

India Nivesh report on Shilpa medicare -as usual a good read-they are quite thorough . EPS 2018 projection of 20.6 & 30.4 for FY 2019. They have a 731 px target

The report can be accessed here - page 23 to 25. Thanks to IndiaNivesh for making it available in public domain.

1 Like

Excellent work. I had it via Bloomberg but was not sure if I could post it publicly