Q4’19 numbers are not encouraging, especially on the revenue front…

Indeed not encouraging.

Traditional media was a bit disappointing.

What’s more interesting to me is their balance sheet in the presentation.

The management said they would be in monetisation phase from FY18 and decrease their debt using the cashflows generated, however I see a rise in short-term debt. Though it is a small rise of 11 crores compared to 900 crores market cap, my expectation was that it would decrease!

Another point is rise in inventories by 80 crores. This shouldn’t happen if the management has moved from investment phase to monetisation phase.

Disclosure: Invested and forms 10% of portfolio. Waiting for Q4FY19 Conf Call Transcript to be uploaded. Hopefully someone asked these questions.

How serious is this? @Donald @dd1474 @suru27

The article says Shemaroo owns negative copies of films which are being illegally hosted in sites like Voot. Am I correct in understanding that the major accusation is against sites like Voot, who have illegally hosted the content without hosting permissions or did Shemaroo have prior knowledge too?

Also, what’s the law on owning vs hosting? Is it legally binding on Shemaroo to check if the content hosts they supply to already have hosting permissions?

Thank you.

The Digital distribution of films has started in India some where after 2000. Find enclosed article providing more information on same.

So early 2000, the rights of movies were sold by only negative rights.

When I read this news, I realise that movie was released in 2000. It is my presumption (and not claiming it to be correct) that Shemaroo would acquired distribution rights perpetually for the movie. During 2000, there was no digital distrubution concept. Most of distribution was by CD/ViHS tapes/DVD/ Cable/ Telecast over channels. So not sure how contract between film distributor and Shemaroo.

From Shemaroo IPO Documents, I find that they categorise rights in two broad segment: Aggegate (Limited) Rights and Perpetual Rights. In case of perpetual they replace the producers and have rights across the medium, territory for remaining period of life (Generally right are 60 years from creation). In aggreage rights, they have limited period, territory or distribution medium and do not own all right.

So point of dispute could be whether “Jung” movie right is perpetual or Limited/(aggregate). With no information about contract, it would be unfair to arrive at conclusion at this stage with given news article. However, being in business for more than 5 decades, it would be reasonable to assume that Shemaroo management and legal team would have done all needful due diligence and documentation before acquiring the rights and distributing same.

Since the complaint is already filed with Police, we shall expect way forward leading to litigation.

In nutshell, while I do not have any insight in the specific case in news, In general, I belive that management would have taken due care while acquiring and distributing the movie. If subsequent development show otherwise, then that would be major development for me to re-evaluate my investment thesis.

Discl: Shemaroo among my Top 10 holding and my view may be biased due to my investment, no investment action in last 3 months, Investor shall consult their investment advisor before making any investment.

Find enclosed Shemaroo Reply on the matter submitted to BSE. As per Shemaroo Management, they have not authorised/assigned “Voot” to streaming movie “Jung”.

https://www.bseindia.com/corporates/AnnDet_new.aspx?newsid=A8418562-9CE0-4FF7-865F-BF3AE7551DF0

Hi, have any of the long timers on this stock carried out any analyses on valuation ratios over the years ? EV / EBITDA, EV / Sales vs RoE ?

At current levels, seems very attractive - thoughts / analyses would be much appreciated. Thanks

This is a difficult company to value, at least for me.

One way is to estimate the value of 1) current library, and 2) future rights acquisition separately, and then add them up. Both will have a wide range, depending on one’s assumptions.

For 1), should one assume that the economic value of the perpetual rights will appreciate by double digits every year, as it has in the (recent?) past, and as has been guided by management? Or should one assume that the relevance will reduce over time, and hence it is a depreciating asset, which will produce reducing cash flows over time, even though there may be spikes in monetization because of periodic tailwinds like Jio? I would lean towards the latter. In any case, rights appreciating by 10-15% per year over the medium to long term (till copyrights expire) seems too good to be true.

For 2), it could be a positive or a negative value, depending on how one views the management’s acumen to ‘trade’ the rights smartly. I would assign a positive value to this at the moment.

Tons of other variables too, of course, but just thought these are interesting points to think about.

Disc: Tracking for now.

Towards the end of it, it says Shemaroo’s planning to launch devotional content on Bluetooth speakers.

They are selling on Amazon:

- https://www.amazon.in/Shemaroo-Shrimad-Bhagavad-Gita-Speaker/dp/B07PS2Y6HY/ref=sr_1_1?keywords=Shemaroo&qid=1562493772&s=gateway&sr=8-1

- https://www.amazon.in/Shemaroo-Specially-Curated-Mantra-Bluetooth/dp/B07PS6VNCQ/ref=sr_1_4?keywords=Shemaroo&qid=1562497374&s=gateway&sr=8-4

- https://www.amazon.in/Ibaadat-SQ109-Quran-Majeed-Speaker/dp/B07JXYCW1N/ref=sr_1_6?keywords=Shemaroo&qid=1562497374&s=gateway&sr=8-6

Hopefully it’s just the start of many more such products that can be launched by them.

Any reason for the continuous fall. Just doesn’t seem to be stopping!

I also do not see any reason…Its at an attractive price. Any company which grows at even 15 % CAGR available at 10 PE is lucrative. Also the business is going to grow with more digitization , only thing we need to monitor is how they are monetizing their assets. NO RECOMMENDATION but I see the price attractive.

Company is going from transition phase so it’s wait & watch strategy from investor point of view.

The other major thing could be high debtors.

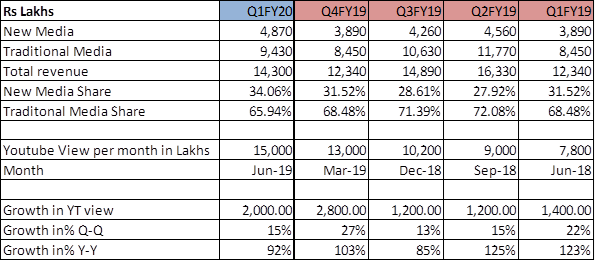

Shemaroo Results for Q1FY20 decliared yesterday. The company reported revenue growth of 15.9% (Consolidated), but EBITDA margin declined 22.3% in Q1FY20 as compared with 31.5% in Q1FY19. The higher material cost and employee cost were the main reason for lower EBITDA. With Depreciation charges compable to Q1FY19, the Finance cost declined by 5%. The increase in other income also assited to reduce impact of EBITDA. Net profit during Q1FY20 was lower by 17.4% as compared with Q1FY19.

| Consolidated (Rs Cr) | Q1FY20 | Q4FY19 | Q3FY19 | Q2FY19 | Q1FY19 |

|---|---|---|---|---|---|

| Sales | 14303 | 13219 | 14,895 | 16,333 | 12,336 |

| Cost of material consumed | 8791 | 6106 | 9,014 | 9,789 | 6,845 |

| Change in inventories | 0 | 0 | 0 | 0 | 0 |

| Employee cost | 1575 | 1664 | 1,509 | 1,226 | 1,110 |

| Other expense | 746 | 1348 | 843 | 1,055 | 492 |

| Gross margin | 5,512 | 7,113 | 5,881 | 6,544 | 5,491 |

| Gross margin % | 38.5% | 53.8% | 39.5% | 40.1% | 44.5% |

| EBITDA | 3,191 | 4,101 | 3,529 | 4,263 | 3,889 |

| EBITDA % | 22.3% | 31.0% | 23.7% | 26.1% | 31.5% |

| Depreciation | 144 | 142 | 144 | 133 | 140 |

| Finance cost | 577 | 730 | 652 | 563 | 613 |

| Other inome | 85 | 82 | 69 | 0 | 23 |

| PBT | 2,555 | 3,311 | 2,802 | 3,567 | 3,159 |

| Tax | 917 | 1,252 | 846 | 1,270 | 1,205 |

| PAT | 1,638 | 2,059 | 1,956 | 2,297 | 1,954 |

| Minority Interest | -20 | 32 | 3 | 8 | 9 |

| Associate share in profit/(loss) | -4 | -2 | -2 | -8 | -9 |

| Consolidated net profit | 1,614 | 2,089 | 1,957 | 2,297 | 1,954 |

| Sales Growth YOY | 15.9% | 11.7% | 12.3% | 21.6% | 19.0% |

| EBITDA Growth YOY | -17.9% | 11.6% | -1.5% | 18.0% | 16.4% |

| PAT Growth YOY | -17.4% | 11.6% | 9.9% | 22.8% | 22.7% |

The company has announed conference call today when we may get more insight. Overall, mixed bag results. Topline growth and finance cost (indicating lower debt) is encouraging, bottom line decline is negative in my opinion.

On business side, the company continue so good traction in Digital media. The growth in digital media is 25% (as compared with Q1FY19) and traditional media sales growth is 11.5%. The share of Digital in total sale first time cross 33%. Youtube view also coninue to show very high growth. Find enclosed key parameters over quarter. Youtube viewership figure are Lakhs per month as read by me from quarterly press release in chart and there scope for misreading.

Discl: Among my Top 10 holding. Views may be biased, Investor shall consult investment advisor before making any investment decision,.

I think in such industry…only big fish wins. Small need to burn too much money to race and finally get exhausted.

Someone please share the conference call notes or link to read the conference call notes

Thanks:pray:

I am posting here cutting from ril agm notes-

SECOND, Edge computing and Virtual and Mixed Reality content.

As you saw in the demo, the next frontier of content is immersive.

This creates exciting new possibilities for entertainment, shopping, gaming and most importantly for education.

Delivering immersive content to hundreds of millions of users requires a well-integrated solution spanning connectivity,

data storage and real-time computing.

And we need to deploy such solutions at the edge of the network or in other words, closer to where our users are.

Today, JIO is setting up a pan-India Edge Computing and Content Distribution network again starting with tens

of thousands of nodes.

This means that your favourite content and applications will be even nearer to you.

So even faster downloads and faster response times

Will it impact shemaroo,or i am misunderstanding something

The part where he says about watching movies at your home the day they are released should impact shemaroos business. He is planning to disrupt the value chain of entertainment industry , eliminating middle men like shemaroo from what i understand . Eventually Sheamroos movie inventory can lose its value if that happens

Disc -invested

He is trying to say that if jio will show every movie on tv on release date, then it is obvious that jio will buy its rights also, to create a digital library, when ever customer wants he can watch from jio library, and so the business of shemaroo will get impacted