Why the distributor is between the Content owner and the broadcaster. Is’nt a possibility that content owner directly sell the rights to broadcasters avoiding the distributor.

The rational behind distributor looks that the content owner does not have to indulge much for finding a broadcaster for every movie over several platforms. Everything will be on distributor . But what if it changes with the coming of new OTT platforms and amazon / netflix buying perpetual broadcasting rights , traditional TV broadcasters buy on their own. It would be a better deal for the content owners to sell to different entities and profit more. How one should see this ?

They mostly go for acquiring rights in second cycle. What if the first cycle owner renew again. Won’t there be a competition then and thus higher acquisition costs.

Cash flows were a little difficult to understand but the thread made that easy. Lower numbers of acquisition and higher monetization resulted in great cash flows in 2018. Though they have a very decent library of movies , why should the acquisition cost will come down. Is that they were in an acquisition mode and most of the old popular movies they have purchased now and will be buying very few in coming years or will the old movies monetization are expected to beat the new acquisition costs ?

Around 120 Movies were released in 2013 (5 years back) . The year was great for bollywood and we witnessed quality movies like Ram Leela , Madras Cafe . Yeh Jawani hai Deewani , Bhag Milkha , Satyagraha , Special 26 , Kai Po Che et cetera. I think they would have to be more aggressive. Also the numbers of movies coming in recent years are increasing every year along with a lot of original contents. Isn’t the higher acquisitions is a non ending part and if monetizations do not resulted in better cash flows from here , company may face some issues.

I understand that it can not be a cash throwing machine due to the nature of the business but isn’t most of the business depends on the promoters acumen ? Also we have to trust the promoters words for any actions ?

History of promoters looks good as they have brought necessary adaptions with the changing times.

Shemaroo Youtube has lots of movies for free but i don’t see any advertisement during any movie. What kind of revenues it generates from Youtube and how ?

They are coming up with own OTT “Shemaroo Me” . Unless they don’t charge for youtube movies , why someone will subscribe for OTT ?

Decent app certainly, but not sure how many will be interested in it. For the end user it is just another OTT app with less latest movies. Their TV offerings are more interesting than the movies btw.

Most of these questions, I too had and was addressed by Dhwanil in this thread. Please check above thread, should help a lot as fellow VPers like @desaidhwanil@dd1474 have put lot of effort in analyzing and addressing some of these queries . However, my stand on point no 1 and 2 was future would be very different from past and it is risk. I dont see why with all minute by minute consumption data in hand, content marketplace companies like Amazon, Netflix can not take a data driven better decision to negotiate 2nd life content monetization decisions which disruption of business model itself. We all have rights to decide, conclude and go right or wrong and this is just a personal view

I personally think they are pricing it aggressively and will have a tough time to find subscribers, especially in the bollywood space. Why would anyone choose ShemarooMe over Zee5 / SonyLiv / HotStar for Bollywood content?

Not sure if we have Gujarati / Kids / Bhakti / Ibaadat specific OTTs in India. Hopefully, they should help find traction as they look very niche without any competition.

Also surprised to see they don’t have any ads in their free videos!

Platform

Plans

Target

ShemarooMe

1000/year for full, 500/year for selected

Age 40+,Kids,Gujarati,Devotional

PrimeVideo

1000/year

Urban

Zee5

1000/year for full, 500/year for selected

All

Hotstar

1000/year

All

SonyLiv

500/year

All

Netflix

9600/year

Urban

AltBalaji

300/year

All (but mostly original shows)

Hooq

450/year

English

ErosNow

950/year, 470/year

All

Sun Nxt

490/year

South

Anyone attended concall and took views from management on pricing / projections / expectations?

On a side note, I am not extremely sure on profitability of Hotstar either. For US subscribers they’ve offered 1 year subscription for $60 with a free $50 Amazon Gift Card. Their usual prices are $9.99/month. The another offer they tend to run is $15 for 3 months. I haven’t researched pricing model for other services in this segment but I agree with @lingalarahul7 , not many subscribers would be willing to pay Rs. 1000/year when majority of content is either very cheap or free and piracy isn’t going away anytime soon.

I feel that at this stage, its best to monetize on free platforms with ads. The demographic would much rather watch ads than pay for ad-free experience.

This is already happening for movies under large production houses (see link below), but however small time producers will have tough time to bag such deals. I think the market is too big for these players to kick Shemaroo entirely out. I believe both can co-exist here. Moreover, I doubt if the Prime Video / Netflix will do this for regional movies too. https://www.hollywoodreporter.com/news/amazon-strikes-licensing-deal-bollywood-932390

This one, I’m not very confident but can say what I think. First cycle rights are mostly acquired by Broadcasters / OTT players directly from producers as they are acquired for spiked TV views / OTT customer acquisition. This reason doesn’t stand when they acquire rights for second cycle. TV channels / OTT platforms show good amount of movies which are 5-10 years old and going through each of them can be a burden when they don’t have a special value of spiked TV views / OTT customer acquisiton. However, I still think this scenario is possible when businesses decide to invest resources to backward integrate. But the important question is when will this materialise and what actions would Shemaroo take when this would happen?

Good thing is Shemaroo’s management acknowledges they see more value in acquiring perpetual rights and in fact are increasing their share of perpetual rights, albeit slowly.

Content library (#)

2018

2017

2016

2015

Hindi perpetual

471

443

423

366

Hindi limited

1454

1423

1394

1336

Regional perpetual

511

456

440

373

Regional limited

1017

984

927

750

Special interest perpetual

55

49

49

42

Special interest limited

243

230

199

144

Total

3751

3585

3432

3011

Perpetual %

0.2764596108

0.2644351464

0.2657342657

0.259382265

Limited %

0.7235403892

0.7355648536

0.7342657343

0.740617735

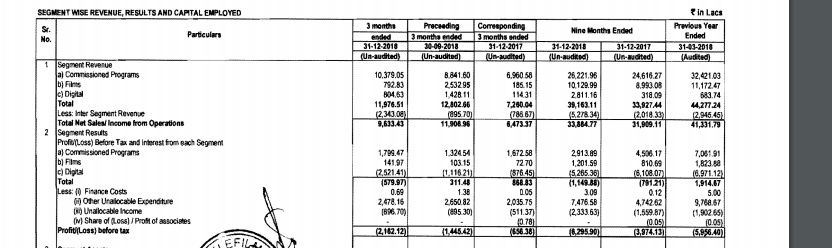

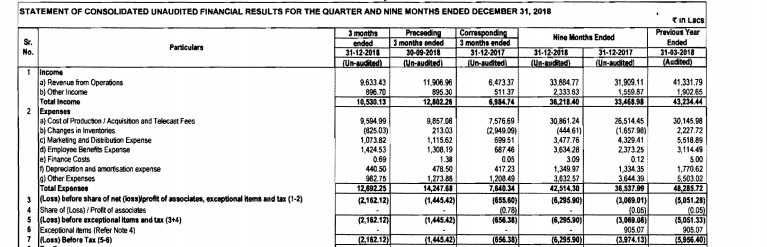

Agree that poor monetisation can shake the whole investment scenario, however I would assign this event a very low probability. Number of Bollywood movies releasing per year is growing slowly while Shemaroo’s revenues are increasing at a higher rate (~15%). Also, the accounting method would help improve cashflows in the future - read Dhwanil’s posts above.

You can notice that in FY18, they have improved their cashflows without compromising on the number of movies they have acquired. I believe this will only improve in the coming fiscal years.

Agree depends a lot on promoter’s acumen and our trust on them, but isn’t that the case for many businesses? Can you be more specific?

OTT story is just beginning and yet to unfold. Need to do more research on this regard. However, good thing is they are not over-aggressively promoting it compared to Balaji Telefilms. Recent increase in Employee benefits expenses must be due to this venture. I believe that failure in OTT venture wouldn’t hit the business too hard.

Free content will be monetised through advertisements

Shemaroo’s original content would be documentary series around films and chat shows where modern-day stars interview heroes from yesteryears

When it comes to ‘Bhakti’ and ‘Ibaadat’, the platform will bank on live streaming from various shrines across the country and its library of Bhajans. The content team will create chat shows and darshan videos too

We own 70% of the Gujarati content that exists in the market today. These include movies, Gujarati nataks, short-form series etc

The affluent small-town audience in tier II and tier III markets is what Shemaroo is going after

Hiren Gada: "We will invest whatever is necessary, but at the same time, we will be cautious. We don’t want to get to a situation where it becomes either work out or burn out

In terms of marketing new platform, Shemaroo will use its existing YouTube channels as they are the lower hanging fruits it wants to acquire initially

Disclosures:

Accumulating over the past few months.

Not a SEBI registered advisor. Not a buy / sell recommendation.

Interesting development from Shemaroo. However, as per latest conference call, the revenue from OTT would offset by decline in telecom revenue as many telecom companies are moving from web based media delivery to OTT media delivery. That was also main factor to launch OTT by Shemaroo as it claim to operating in B-B-C segment as against other OTT like Hotstar which are B-C.

While increase in number of subscriber is critical for future growth, the business are going through major refinement. In tradtiional media, change to fee based subscription mandated by TRAI has increased uncertainity in short term, it may be benefit the content owner eventually. Given the content liberary dominated with 70-80s block busters, one need to see how Shemaroo utilise its content with opeating leverage.

In digital world, the new app launch would provide critical missing component from Shemaroo offering, i,e, web based delivery. Further, it try to increase offering in commedy, regional and devotional segments throuhg app.

Disclosure: I continue to hold Shemaroo shares and my view may be biased. Investor shall do his/her own due diligence before making any investment decision. I have sold nearly 20% of peak holding in phases since January 2018.

Subscriber data of different OTTs:

Zee5 - 56.3 million MAU (not sure on paying subcribers number) as of Q3FY19

ErosNow - 15.9 million paying subscribers as of Q3FY19

Hotstar - 150 million MAU (& estimated 5 million paying subscribers) as of Q2FY19

AltBalaji - 10.5 million paying subscribers as of Q3FY19

Netflix India - 0.5 million paying subscribers as of Q2FY19

PrimeVideo India - 13 million paying subscribers as of Q2FY19

Let’s estimate revenues without OTT business first with simple growth rate of ~15%.

Revenues in FY18 ~ 490 crores

Estimated revenues in FY19 ~ 560 crores

Estimated revenues in FY20 ~ 640 crores

Presenting some case-wise analysis below for end of FY20.

Bear case:

Shemaroo acquires only 1 million subscribers across all categories, with average subscription price of 500.

OTT Revenue = 0.1 crores * 500 = 50 crores

=> Revenue growth for FY20 ~ (640+50)/560 - 1 ~ 23%

Base case:

Shemaroo acquires only 2.5 million subscribers across all categories, with average subscription price of 600.

OTT Revenue = 0.25 crores * 600 = 150 crores

=> Revenue growth for FY20 ~ (640+150)/560 - 1 ~ 41%

Bull case:

Shemaroo acquires 5 million subscribers across all categories, with average subscription price of 700.

OTT Revenue = 0.5 crore * 700 = 350 crores

=> Revenue growth for FY20 ~ (640+350)/560 - 1 ~ 76%

Most of the OTT revenue will fall directly into PBT as we already have the rights to our movies. Tech employee costs are already being incurred since past few quarters, so the current margins will continue and will only increase marginally for some additional tech requirement, content making and marketing. D&A wouldn’t make much sense here.

The growth which Shemaroo can achieve at its current valuations look attractive to me, even in the bear case.

With OTT business, the balance sheet of Shemaroo should improve at lot!

Improved inventory turnover ratio: First of all, inventory days for companies like Shemaroo is not defined as inventories can be re-used. Even if market wants to look at it that way, the inventory turnover ratio is going to improve as revenues will increase disproportionately as compared to inventories from now on.

Similarly, trade receivables as % of revenues would decrease as OTT revenues would be received immediately by the company, unlike TV syndication revenues, which are a drag on the balance sheet.

Disclosures:

Accumulating over the past few months.

No private data used in this post.

Not a SEBI registered advisor. Not a buy / sell recommendation.

10.5 mn subscribers for alt Balaji includes telecom subscribers

Direct consumers is difficult to decipher.

Balaji mgmt a couple of concalls ago mentioned the ratio being approx 1:3 so assuming that holds we get a direct subscriber base of 2.6 mn subscribers

The arpu of Direct subs is 25 RS and telecom is 12-15 rs

So Shemaroo getting a subscription 1 million subs at 500rs is not constitute a bear case it might an optimistic scenario

The management Is still concentrating on telecom consumer ( they reqd the ott platform to get on the telecom platforms) hence arpu will not be so high but users will be much higher

Management intends to replace the declining mvas revenue(50% of digital revenue current) with the ott platform

So you might have to re run the nos my cautiously optimistic guesstimate is over time revenue will reach

10 RS arpu per month *12 months * 5 million users =60 cr per annum

And mvas will go from 25 odd crores to 0 over the same time

Revenue increase will be 35 crores

Alt Balaji had 10.5 mn subscribers at the end of Feb - and revenues of INR 8 cr. Thats INR 8 per subscriber for the quarter so clearly all these subscribers are not paying anywhere in the ballpark of INR 300-500.

If we expect INR 300 per user per annum (INR 75 per user per quarter), Alt Balaji has only 1 million paid subscribers. Moreover, to achieve this number, it has between 10 and 50 million downloads of its app. It also had a loss of 26 cr for the quarter. Also, see the huge jump in employee benefits expense for Balaji -from INR 6 cr last quarter to INR 13 cr this quarter- which I’m assuming is for the technology team of Alt Balaji

To summarize, for a revenue run rate of INR 8 cr in Q3, Alt Balaji had to make huge expenditures on content and people and incur a loss of INR 26 crore after achieving an install base of 10-50 million installs on google playstore.

By comparison, currently Shemaroo has between 50-100k installs since launching on Feb 13. To do an incremental revenue of INR 50 cr or above in the next 18 months,

Shemaroo has to increase their monthly acquisition run rate by 10x

Users should remain engaged and pay without big spends on content

Current team should be sufficient for scale up of OTT - maybe 15% increase in payroll.

Thank you @dwarak and @vivek423.

Very helpful and eye-opening on the ARPU side. After reading your posts, assuming 500 rs per subscriber looks very naive to me too

Also wouldn’t directly compare subscribers vs. downloads across applications. There is a sharp line of quality between them. Agree it is a good starting point at the same time.

AltBalaji reviews are very poor while ShemarooMe has great reviews. Lots of people are appreciating their old movies niche. Can see couple of comments on Kids, Bhakti niches too. However, was expecting more reviews on Gujarati front.

Check the density of reviews on 20th and 27th Feb (80 percent of reviews on those two particular days). Fairly certain the reviews are not all organic. It is typical for most startups to do this until their reviews are in the tens of thousands.

As per the draft policy,“An E-Commerce platform in which foreign investment has been made cannot exercise ownership or control over the inventory sold on its platform.”

It looks like with so many players coming into the space, shemaroo is losing the plot. Shemaroo may work on being a conent providers to these players rather than acquirer.

Maybe the player that owns the customer will have high bargaining power, but it looks like Shemaroo is no where near, nor on the way of being a name into reckon in the industry

@Advait_6270 I think there should be a clarification on whether these regulations would also apply to OTT media platforms. If the intent is to segregate ownership and distribution then it would be a real blow for Netflix, Amazon et all in the Originals segment.

I think right now the market is being ‘made’ and it would be in everyone’s best long term interest that the market becomes larger. More people willing to spend money on entertainment and media augurs well for all players including Shemaroo.