Shemaroo business (at the current juncture) brings to life, several patterns or Mental Models that we have come to value (i.e. SIT UP AND NOTICE) - during our active process of churning a large number of stocks - in the search for a superior business/superior returns

1.Whenever we come across what seems like a superior business - we like to immediately ask - “Isko hilaega kaun” how difficult is it to dislodge this business from its perch?

If we find, We can’t find an easy answer to that, that’s a very good sign

2.If the answer to that is Yes - very very difficult to dislodge, then we like to get a feel for - If the Management can execute well, Where is this business likely to be, in next 2-3 years? Getting a FEEL for the business - Is this a business at an inflexion point? Are there favourable tailwinds for the industry as a whole? Has the Management shown the Foresight, Self-Confidence, and the Execution acumen to consistently grow better than Industry?

Deliberating on above, if we find “Hey, should it continue to execute well, this business will be at a different level in 2-3 years **” - that’s probably pointing to a winner

As I have (and we should all) learnt from Ayush - catching a (superior) business in transition forms a large chunk of getting skilled in the Investing ART part !!

There are a few more steps …before and after, and in-between, like establishing the length of the runway, how predictable is the business (number of variables), etc but since all that has been established before, let’s cut to the chase… the most important part perhaps (to me at least) of the Investing ART form! …

3.What leads to superior stock market returns? Most folks answer that with different nuances, but if we think clearly - there is only one definitive answer ![]()

the GAP between “Perception” and "Performance". Perception is what is built into the current valuation. If actual business performance is superior to the current perception of the business, we might be moving towards a clinching argument

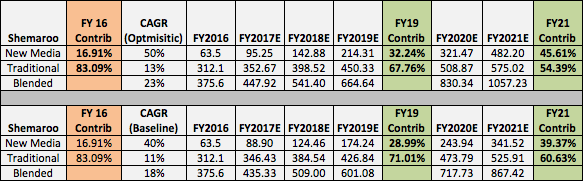

As part of this exercise, its naturally important to get a FEEL (using conservative projections than fed by Management), for where the numbers could be 2-3 years down the line

To be frank, armed with Dhwanil’s Investment Note and all the arguments/counter-arguments already made in this thread, just this simple baseline projection above - was enough to convince me of Shemaroo Investment case.

That there’s probably a GAP between how the business is being perceived today versus where the business is likely to be in 2-3 years time.

It’s been Dhwanil’s case, and it should be ours too

A. The business is not being assessed as it should - it is probably mis-understood. If you take into consideration the business model, and how Shemaroo buys content and monetises it with a lag, the normal objections should fade away

B. The business (and Industry) is at an Inflexion point. In a couple of years if it executes well, it’s an entirely different business, throwing out Cash as product mix changes increasingly in favour of New Media, brings working capital cycle in its favour, and starts funding content acquisition more through internal cash generation. In 3-5 years, could this be a very strong business??

Disc: Invested close to ~10% of Portfolio. This is NOT a Recommendation piece, but a discussion-influencer on detecting a business in transition. I am not an Investment Advisor. Please familiarise yourself with the Risks in the business, and take advise of a registered Investment Advisor for any investment action.

@sudhe09

EPA is a powerful construct - and no doubt it’s center-piece to Future Value Creation in a business. Don’t think anyone made the case about EPA being the starting point in building an investment case. At the start of detectable business transition, it is more useful to project and get a feel for the Numbers (Growth, Margins & Returns) and hence EPA - 2-3 years down the line.

Ayush & Hitesh taught us how to relax the thresholds a bit - when we detect a business in transition - as long as there are sure-shot signs of improving trends. If we can’t do that and remain rigid, we would always miss out on an Avanti Feeds, and an Atul Auto, even an Ajanta Pharma - while in transition to those wonderful EPA numbers they soon start spewing out - remember how the numbers transformed!! If they somehow continue to execute well, these are usually the fastest wealth creators too!!