concall transcriptshemaroo q2 fy16 concall.pdf (219.8 KB)

1.Target to reduce receivables to 140 days over next two years as new business contribution increases further.

2.Management optimistic about increasing new business content consumption due to launch of jio 4G and it’s impact on price erosion for data prices across all operators.

3.Management is planning to taper investment/acquiring content and looking to prepone monetising the content by few quarters.Management senses that there is opportunity to monetise content on new business due to 4g launch and increased data consumption.Its going to increase the free cash flow and makes balance sheet healthy.

4.confident of maintaining traditional media growth of around 12% and new business growth of around 50%.

@desaidhwanil @dd1474 sir your view particularly related to management plan of tapering the investment mode and looking to monetise the content early.

disclosure: invested and added during recent correction.

Been a lurker on this forum for a couple of years now and finally jump onto the bandwagon for some healthy company dissections and debates. Been value investing for the past 3 years and very keen to learn. Do excuse any “noviceness” on my part.

My 2 cents on Shemaroo:

With a current PE of 13x, consistent growth in the 30-40% range over the past 8-10 quarters and a decent growth visibility in the future I don’t see much of a downside risk here. Besides, it’s in one of the few sectors that will probably have a relatively lesser impact due to the recent demonetisation as compared to other sectors. I think there’s a good possibility of a re-rating of this stock besides the good visible runway (growth story) for the company in the coming years.

I also like the fact that in this business once titles are acquired, they become cash cows after a certain point which is phenomenal!

Question to the boarders: Would like to know how the acquisition of titles work though: Are they sold to multiple companies or does Shemaroo have exclusive rights to the titles?

Disclosure: Added to my portfolio during the recent market correction.

I had earlier tried to explore this stock but stayed away as i felt on both revenue and well as expense side, there is too much of accounting. As I am not an expert on accounting and I had to trust on management for accounting principles, could not make up my mind (this sector is full of account frauds though shemmaroo has investments from people on VP whom i respect a lot and have learnt a lot from their posts, so, I am sure, they would have done their home work). Also, I could not buid confidence that what is new shemaroo brings to the table when it buys content in its second life cycle. What stops the 1st life cycle content holder to renew the content license as they would be better equipped to take ROI decisions on 1st life cycle content. The only advantage i see for shemaroo because already they have huge content base and second life cycle content works better on bundling concept to buyers but will it continue to be a sustainable advantage. Too many questions and hence stayed away.

Note : This is my personal view about building conviction on a stock which by any means does not mean that it is a good or bad stock.

A great discussion thread here. Thanks Dhiraj for pointing me here some ~2months back ![]() Like to acknowledge idea initiator @myprasanna, idea validator @dd1474, @anon34631667 playing a great devil’s advocate role, and most importantly @desaidhwanil for presenting his compact and very insightful Investment Note - it helped me come up to speed in just a couple of hours.

Like to acknowledge idea initiator @myprasanna, idea validator @dd1474, @anon34631667 playing a great devil’s advocate role, and most importantly @desaidhwanil for presenting his compact and very insightful Investment Note - it helped me come up to speed in just a couple of hours.

Using Dhwanil’s Note as a great starting point, and going through the excellent discussion flow on this thread - was enabled to do a top-down job and come to my own conclusions - in just a couple of days. It appeared one had - what we like to call an EASY DECISION!!

However despite Dhwanil’s excellent note, and the engaging discussion in the thread, I am SURPRISED this has not caught enough attention, and consequently perhaps the strengths of this uniquely-positioned business (at compelling valuations) at a very interesting industry/business inflection point?. While I will not be adding anything new, here’s an expose on the thought process and underlying-assumptions for Shemaroo investment decision-making. Hope this helps re-emphasise the key things to notice in this business in a bid to CONNECT the DOTS.

Disc: Invested, close to 10% of Portfolio. This is NOT a Recommendation piece, but a discussion-influencer on detecting a business in transition. I am not an Investment Advisor. Please familiarise yourself with the Risks in the business, and take advise of a registered Investment Advisor for any investment action.

Hi Donald

Only one basic question since we had covered a lot on EPA/Sales as a reliable stat to be considered before investing. In the case of Shemerao, I see that EPA/Sales is -ve for most of last 10 years. How do you see this?

Br,

Sudheendra

Shemaroo business (at the current juncture) brings to life, several patterns or Mental Models that we have come to value (i.e. SIT UP AND NOTICE) - during our active process of churning a large number of stocks - in the search for a superior business/superior returns

1.Whenever we come across what seems like a superior business - we like to immediately ask - “Isko hilaega kaun” how difficult is it to dislodge this business from its perch?

If we find, We can’t find an easy answer to that, that’s a very good sign

2.If the answer to that is Yes - very very difficult to dislodge, then we like to get a feel for - If the Management can execute well, Where is this business likely to be, in next 2-3 years? Getting a FEEL for the business - Is this a business at an inflexion point? Are there favourable tailwinds for the industry as a whole? Has the Management shown the Foresight, Self-Confidence, and the Execution acumen to consistently grow better than Industry?

Deliberating on above, if we find “Hey, should it continue to execute well, this business will be at a different level in 2-3 years **” - that’s probably pointing to a winner

As I have (and we should all) learnt from Ayush - catching a (superior) business in transition forms a large chunk of getting skilled in the Investing ART part !!

There are a few more steps …before and after, and in-between, like establishing the length of the runway, how predictable is the business (number of variables), etc but since all that has been established before, let’s cut to the chase… the most important part perhaps (to me at least) of the Investing ART form! …

3.What leads to superior stock market returns? Most folks answer that with different nuances, but if we think clearly - there is only one definitive answer ![]()

the GAP between “Perception” and "Performance". Perception is what is built into the current valuation. If actual business performance is superior to the current perception of the business, we might be moving towards a clinching argument

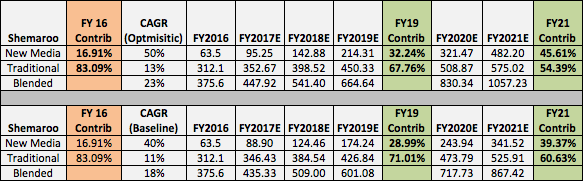

As part of this exercise, its naturally important to get a FEEL (using conservative projections than fed by Management), for where the numbers could be 2-3 years down the line

To be frank, armed with Dhwanil’s Investment Note and all the arguments/counter-arguments already made in this thread, just this simple baseline projection above - was enough to convince me of Shemaroo Investment case.

That there’s probably a GAP between how the business is being perceived today versus where the business is likely to be in 2-3 years time.

It’s been Dhwanil’s case, and it should be ours too

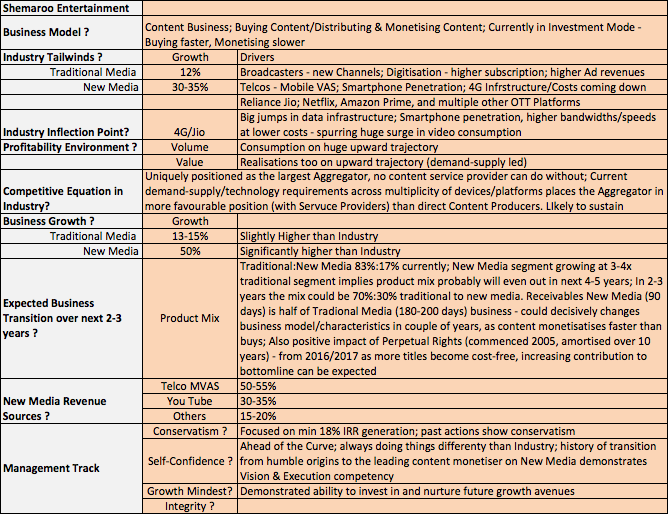

A. The business is not being assessed as it should - it is probably mis-understood. If you take into consideration the business model, and how Shemaroo buys content and monetises it with a lag, the normal objections should fade away

B. The business (and Industry) is at an Inflexion point. In a couple of years if it executes well, it’s an entirely different business, throwing out Cash as product mix changes increasingly in favour of New Media, brings working capital cycle in its favour, and starts funding content acquisition more through internal cash generation. In 3-5 years, could this be a very strong business??

Disc: Invested close to ~10% of Portfolio. This is NOT a Recommendation piece, but a discussion-influencer on detecting a business in transition. I am not an Investment Advisor. Please familiarise yourself with the Risks in the business, and take advise of a registered Investment Advisor for any investment action.

@sudhe09

EPA is a powerful construct - and no doubt it’s center-piece to Future Value Creation in a business. Don’t think anyone made the case about EPA being the starting point in building an investment case. At the start of detectable business transition, it is more useful to project and get a feel for the Numbers (Growth, Margins & Returns) and hence EPA - 2-3 years down the line.

Ayush & Hitesh taught us how to relax the thresholds a bit - when we detect a business in transition - as long as there are sure-shot signs of improving trends. If we can’t do that and remain rigid, we would always miss out on an Avanti Feeds, and an Atul Auto, even an Ajanta Pharma - while in transition to those wonderful EPA numbers they soon start spewing out - remember how the numbers transformed!! If they somehow continue to execute well, these are usually the fastest wealth creators too!!

@Donald One of my relative works in the finance team of Karan Johar’s movie production company. I can easily get answers to any doubts or general queries we might have. We may also get some additonal insights.

Looks like stock reacting to this thread. Up 7.5% in a flat market. Near its life time high.

Thanks Donald for the clarification on EPA !

Goldmine Telefilms , an unlisted company, is operating in first and second cycle of hindi dubbed tamil and telugu films. Recently hindi movie channels have allotted much more time slots to such hindi dubbed movies. Even youtube views of such movies, when released there, cross a remarkable number within very short time (The numbers are higher than shemaroo’s many popular movies). Most of subscribers are from age group 20-35. http://www.indiantelevision.com/television/tv-channels/gecs/goldmines-telefilms-manish-shah-denies-hanky-panky-deals-with-sony-india-150123

Shemaroo and goldmine present in different life cycle of business, so not comparable. But, can such products put pressure on pricing of second cycle movies on DTH, channels, MVAP, youtube etc? Can it be disruptive in that sense?

Let’s take this Shemaroo investment puzzle forward

If we can agree to put the Op Cash Flow/Working Capital objections to the back-burner, then we will have to agree that the only VALID objection is -

-

What if the New Media business segment cannot sustain the 50% kind of growth rates in the near to medium term?? @anon34631667’s main argument

-

What if New Media segment only grows at 20-30% - say at par with the Industry?

A. Does that NULLIFY the Investment case?

B. Can we find out more from non-management sources - of the Growth drivers and Shemaroo/Competition positioning strengths/weaknesses for getting a larger share of the growing pie

@ashwinidamani

Thanks for putting your hand up. You can always use/collaborate with @anon34631667 provided data - to understand this issue slightly deeper - and get further insights on this issue - with scuttlebutt from industry folks you may get access to

a) Shemaroo Management must be acutely aware that bulk of their existing Content is not targeted at the “MIllenials” profile - who are actually the biggest drivers of the surge in video consumption - now and in future too

b) does that hinder Shemaroo from growing significantly higher than industry rates in the near term- why, or why not?

c) do they think the Content acquisition focus of Shemaroo (and everyone else) in the content provider game has already changed - will they be able to remain ahead in that game - why, or why not?

Do think that as we gather more data points, more insights can emerge.

I do have some counters to the above posers (in favour of Shemaroo) but these are educated guesses  , worth that much only… he he

, worth that much only… he he

Meanwhile got this online - A book extract on Shemaroo Strategy

I went through this stock during its IPO. But I had following thoughts at the back of my mind.

RISKS:

- High growth business dependent (youtube channel) on google. Google can ban anything anytime. say Google feed, Orkut. They may adjust revenue share.

- I don’t see what Shemaroo brings to table. What is the value added ? Its easy for a big guy (say Jio) to venture into and lease the titles of 2k movies, where Shemaroo finds it tough to maintain the library. It could risk its internet business as well.

- I am not sure on growth of Traditional business. I couldn’t assess it. New TVs are coming with internet cable slots. You can browser for movies on TV.

- I watch a lot of youtube videos (say TVF), its been years since I watch a movie in TV. The growth in subscriptions for a channel is explosive in first 2 years of its launch. It grows little after that. Shemaroo growth could be mainly because of sudden 3G, 4G availability.

- Acc to latest report, Indian internet base will double by 2020. But, what portion of these base watch Shemaroo in youtube. I rarely watch indian movies. I watch TVF, pranks, reality content, shows, cricket. I watch a lot of non-indian stuff too. I believe lot of indian youth does the same.

ADVANTAGES:

6. What I like in Shemaroo is its youtube channel (internet bet). Anyone around the world can watch. Gr8 business. But this is already priced in share value. I also feel management is shrewd.

I understand that at some point we have to concur with data over rationale.

DISC: Not invested.

Hi Donald this is very useful. I agree that new media growth for industry will be very high and should lead to the overall growth in the sector. However, considering the shemaroo business model for buying in second cycle (after 5 years), will this not impact it growth. My view was the new generation and also people getting added to this ever expanding smartphone wave would prefer watching latest (even if not original) content and that may mean Shemaroo will have to cautious in what they buy - else they may buy more but less sales realization. Secondly, this also means that what rights they may procure will go down in terms of volume, so again can impact growth and sales target. Assuming I have not missed any basic point, how do you see this?

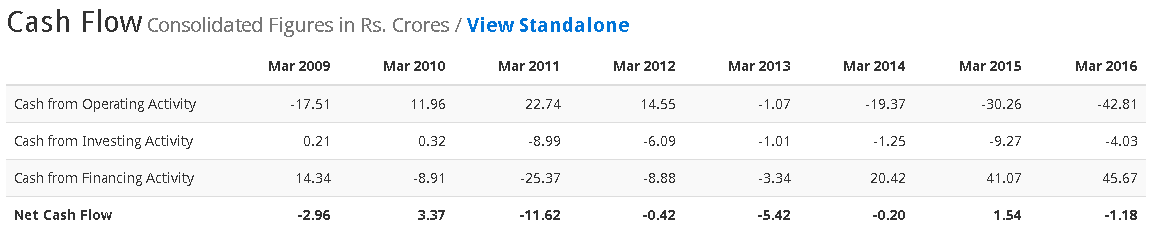

Pardon my elementary question. Why does the company not make any cash flows from operations? I see steady growth in PAT but negative CFO and a constant increase in short term borrowings. And does that not bother anyone?

That may be due to the glowing discussion happening here…and the presence of stalwarts like @Donald @desaidhwanil @dd1474… Even Blogs like RJ have started featuring this thread… More visibility means more copycats, and hence, higher prices… ![]()

Nearly 10% up today… I would wait to enter… let things cool off a bit… After all, the REAL story won’t be seen for at least a year down the road… When the Cash Flow starts showing up… ![]()

Re: Operating Cashflow picture

You may refer back in the same thread - in Dhwanil’s note, and also other places, where this has been discussed at length.

super discussion and much to learn from the insightful posts and notes provided by everyone

If i have to state the business model in a simple way this is how i would do it -

Shemaroo basically buys or creates filmy content , alters it and tries to monetize it as quickly as possible before it loses its value. Whatever money left over is used to buy more content and the cycle repeats.

Some of the content it owns forever ( 26.5% or 912/3432) and some of it is for a temporary period (73.4% or 2520/3432) . A vast majority of the content is Films (92.77% or (1817+1367)/3432).

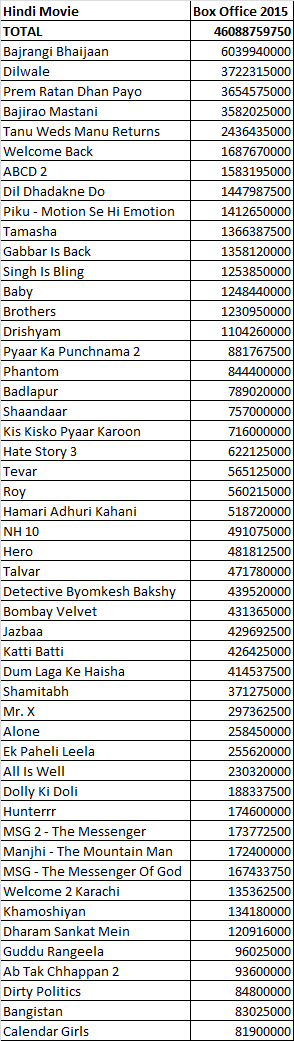

The Total worldwide Box office for the top 50 hindi movies released in 2015 was 4608 crs ( Top Grossers Worldwide 2015 - - Box Office India )

From their investor presentation about ~95% of the revenues are in the first cycle. That means for 2015 about 242 crs revenue ( 5/95*4608) would be up for grabs in the second cycle where Shemaroo participates. From this 242 crs revenue lets say 30% goes to Shemaroo ( it being one of the dominant distributors). This means 72 cr. Shemaroo will try to grab this revenue but it would generally happen over 10 years (after which the no additional amount can be extracted). Thats about 7.2 cr per year. Assuming that our box office grows at 10% and Shemaroo maintains its competitive position and their ROI is 18% ( which they themselves have stated ). This would mean that they would grow their revenues at roughly 10% every year over a 20 yr period ( regardless of the growth in new media you cant earn more in the second cycle than 5% of the overall box office right? ).

Doing a simple DCF (7.2 cr growing at 10% for 20 years @ 18% Discount rate) this comes to about 426 cr. The company already is at a market cap of 1000 cr.

Comments are invited and i am sure that there would be many flaws in this reasoning. But at this juncture i am not too sure about the exuberance around Shemaroo. This is just a big picture kind of analysis and the more detailed analysis has already been presented. But i think this kind of inversion is necessary.

So I spoke to my connect , and these are view points from him -

-

Amazon is also in the business now. They have started buying Streaming Rights (http://www.thehindubusinessline.com/economy/amazon-to-stream-flicks-of-karan-johars-dharma-productions/article9150735.ece)

-

Dharma Production sold a lot of their old inventory to Viacom 2-3 years back for 32 crores (but Viacom is no more in a good shape and has vitually stopped producing new movies and buying new rights)

-

Typically Eros, FoxStar, Viacom, Eros etc buy the satellite rights for 7-8 years. The second cycle starts after 7 years nowadays. Moreover, someone like a Viacom (Colors TV) knows that their channel is not as popular as Star Plus/Sony, so they sublease (syndciate) their rights to the popular channels.

-

Feedback on Eros was not positive (not the best guy out there…i’ll stop the comments at this only)

-

A trend seen with Big Stars like Salman/Akshay etc is that they have stopped taking remuneration for movies they act in. Instead they charge remuneration in form of Satellite Rights. This right is then sold to Sony/Star Plus etc for 7-8 years, after which the rights come back to Salman again and then he sells this in second cycle again (http://indianexpress.com/article/entertainment/bollywood/sultan-star-salman-khan-signed-whopping-rs-1000-crore-deal-with-popular-channel-2914090/)

-

Yashraj never sells its sattelite rights (cant corroborate)

7.Many studios are going out of market. They may sell their inventory at bargain price (Disney, Balaji, Viacom)

One point - he wasnt sure if Shemaroo is participating in the better contents post 2010. Says, never done deals with Shemaroo. They have a good inventory of old movies or pre 2010 movies. Not sure if they are participating in new rights, which were availabl in 2011, 2012, 2013 etc