Looked at this company’s financials because it came up on one of my screens…all numbers below are basis standalone statements of last 5 years (FY21 full year are yet to be released; anyway I would want to analyse the non-pandemic years before thinking about FY21).

I haven’t even started looking at cash flows because what I have seen in P&L and Balance Sheet is enough for me to make my investment decision at current Price levels…

It’s quite a sign of extravagant times we live in that a company whose :

-

Revenue growth is declining YoY (even before the pandemic)

-

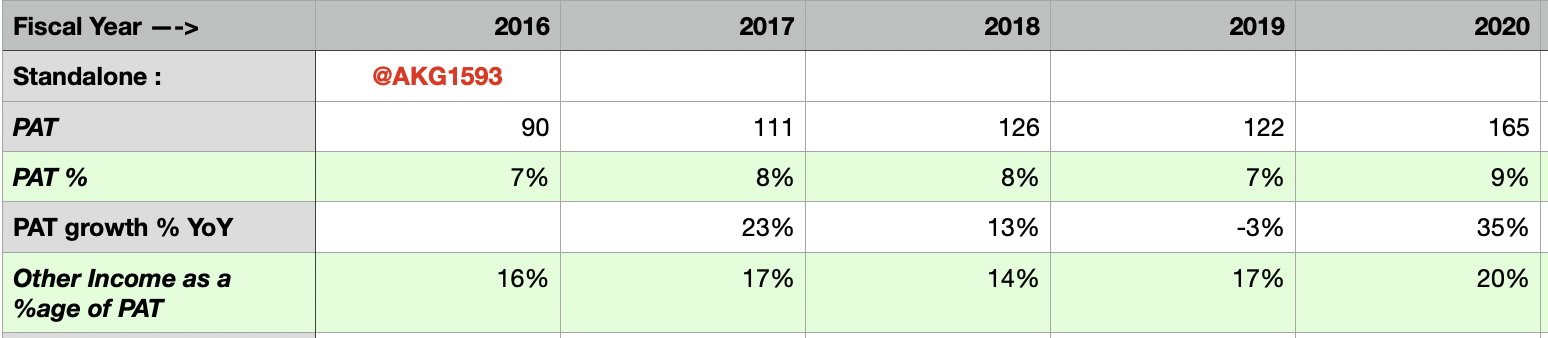

Post tax Other Income (mainly P&L through investments but other non operating stuff) share of PAT is increasing YoY

-

Net Profit margins is in single digits for a branded play

-

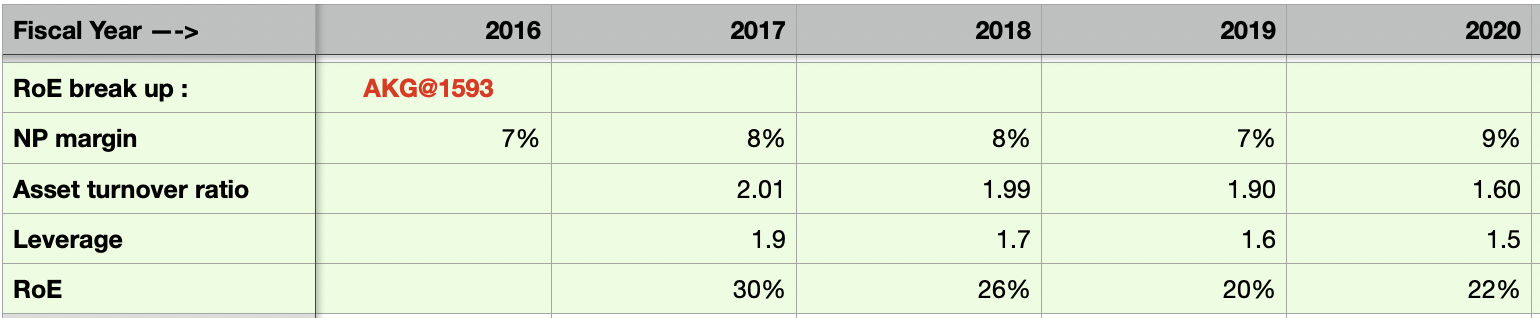

Return on Equity is declining on declining Asset turnover and declining leverage :

-

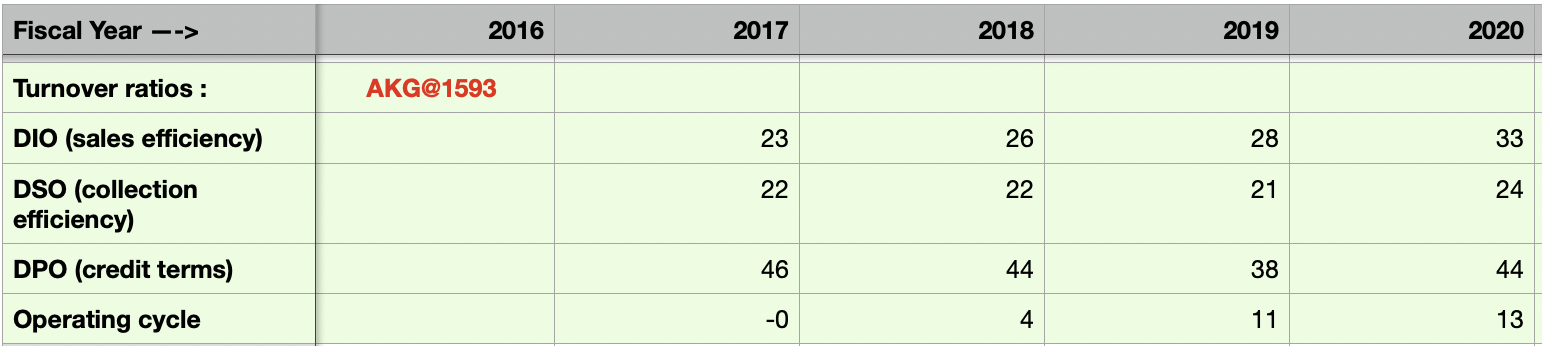

Operating cycle is worsening with a decline in sales efficiency :

-

Pays 0% dividends - For a growing company, it’s fine to retain 100% Earnings to invest in growth; but this isn’t a growing company from what I have seen above (I wouldn’t buy the argument that they are growing through investments/acquisitions abroad - that’s an easy way to divert attention from poor core operating performance which makes up ~80% of the business).

is trading at 45 times P/E, ~10 times P/B, ~38 times EV/EBITDA.

Disclosure : Not invested