But, kurlon as a brand has a pretty strong recall and customer instantly identify it with mattress.

In mattresses space, 3 most popular brands are -

Sleepwell

Kurlon

Century

Now with both brands (Sleepwell and kurlon) under the belt, sheela foam can make new strategic planning.

They might position kurlon as mid segment and Sleepwell being premium segment brand.

I recently visited HGH 2022 Mumbai Fair and sheela foam has largest presence.

They have 4 different booth, spread all over, each catering to different segment.

I never seen Sheela foam putting so much presence in any other HGH or other events.

Things definitely seems interesting over a long run.

–Last couple of weeks the demand has increased and the direction is upwards and its getting better

–Closely linked to TDI RM prices as of Q3 it stood at INR 243/KG which is lower than Q2 , where is it ? --The prices are down and its oscillating and its currently at INR 220/KG so there is a drop from Q3.

–Margins will improve and our products in B2B where selling prices are linked to RM prices there is +ve. The wedding side of the Biz , the contribution of TDI to cost of goods is much lower & therefore it will be a mixed bag and there is a lag between the impact of these prices on margins.

–Inorganic growth ? --co is looking to complete decision making for @FURLENCO acquisition in next 2 months which is a furniture rental co.

–Balance Sheet status ? --Reasonably healthy & we have some 750/800Cr cash on books and debt is relatively negligible but in some places it is there i.e Australia/Europe subsidiaries. Size for Acquisition is dependent on Acquisition but we dont need to borrow from anywhere. The acquisition will be much lesser than 500Cr. The said co is profitable on operating level but loss is there on the financial side. Revenues are 200Cr/year & it can go to 400Cr/Yr once we get involved

–Feather foam / starlight --these brands are primarily supplying to MBOs and all our sleepwell products are completely with the EBOs and there are large no. of MBOs which we have to address and its growing on a steady basis and its dependent on geos and MBOs we go after & it has higher growth as the base is small and universe is much larger.

–FY23 we will be single digit , what’s the outlook for FY24 ? --As of now growth will be 12/13/14% & Margins will be similar 13/14% EBITDA

the brand sees value in its physical presence: The “store is the best representation of our brand. It’s the best way to show all of our products. It’s the experience we can control in a physical way,” Arel said, pointing to the fact that almost 80% of mattress purchases are bought in a place where you can test them out.

Offline / physical retail can never get out fashion and most of the online only brands have to go offline in long run.

Here are some key takeaways from the Q2 FY24 earnings concall transcript of Sheela Foam mattresses:

Revenue growth: The company reported a 22% year-on-year growth in revenue, driven by strong demand for mattresses and other comfort products. The company also gained market share in both organized and unorganized segments.

Margin expansion: The company improved its EBITDA margin by 240 basis points year-on-year, mainly due to better product mix, operational efficiency, and cost optimization. The company also benefited from lower raw material prices and stable forex rates.

New product launches: The company launched several new products in the quarter, such as Sleepwell Signature, Sleepwell Cocoon, Sleepwell Spinetech Air, and Sleepwell Feather Foam. The company also introduced a new brand, SleepX, to cater to the online and value segments.

Outlook and guidance: The company is optimistic about the future prospects, as it expects the demand for mattresses and other comfort products to remain robust, driven by increasing awareness, urbanization, and disposable income. The company also expects to benefit from its strong distribution network, brand recall, and innovation capabilities. The company has guided for a 15% to 20% revenue growth and a 20% to 25% EBITDA growth for FY24.

Kurl-on acquisition: The company has acquired 94.66% stake in Kurl-on Enterprises Ltd. at an equity valuation of Rs. 2,150 crore. The deal is expected to be completed by December 2023. The management expects significant synergies from the acquisition in terms of product portfolio, distribution network, manufacturing capacity, and cost savings. The combined entity will have a market share of more than 50% in India’s organised mattress space2.

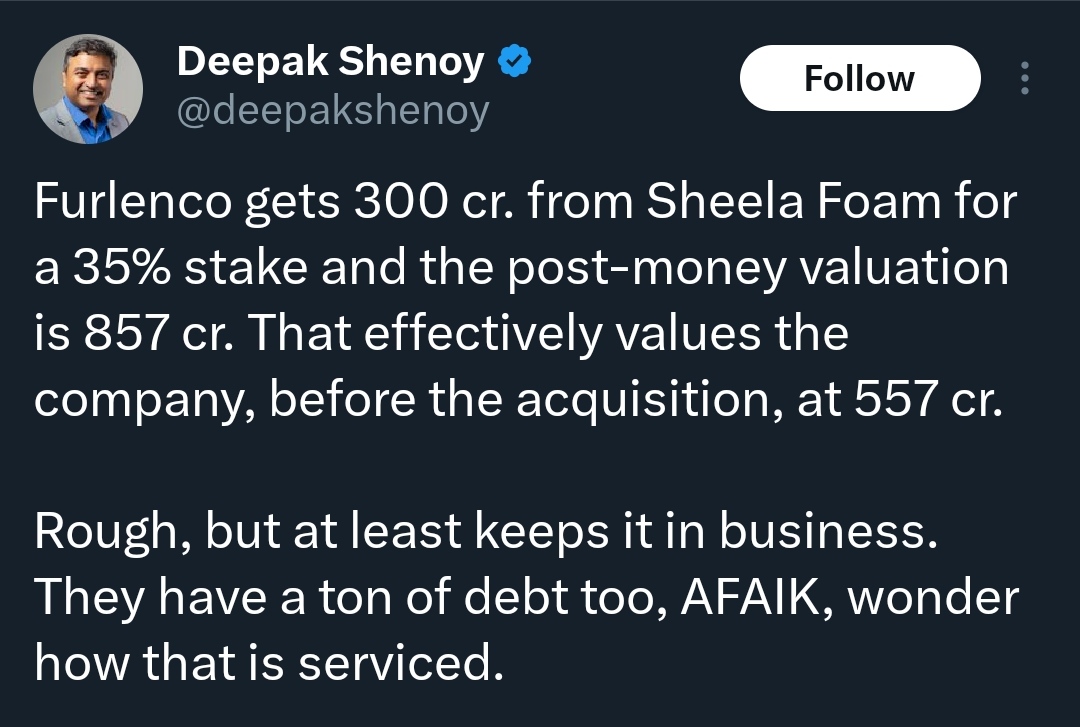

Furlenco acquisition: The company has acquired 35% stake in Furlenco, a furniture rental company, for Rs. 300 crore. The deal is expected to be completed by March 2024. The management believes that Furlenco is a disruptive player in the furniture industry, with a strong brand, loyal customer base, and scalable business model. [The company aims to leverage Furlenco’s online presence, data analytics, and design capabilities to expand its own product offerings and reach new customer segments]

sleepwell strong in north n west, kurl-on on east and south.

kurlon acquisition ramping up.

furlenco not yet PAT level profitable, will be by feb 24.

There are efficiencies or expertise of their respective companies.

Kurlon has a high level of expertise in rubberised coir, making those coir, which we used to buy from outside.

We manufacture foam much more efficiently than Kurlon. Approximately our yield is 10% higher to them.

We are able to service our customers from the nearest distance possible. So our freight cost is going down. So these are the things which definitely yield – would yield tangible benefits to the bottom line.