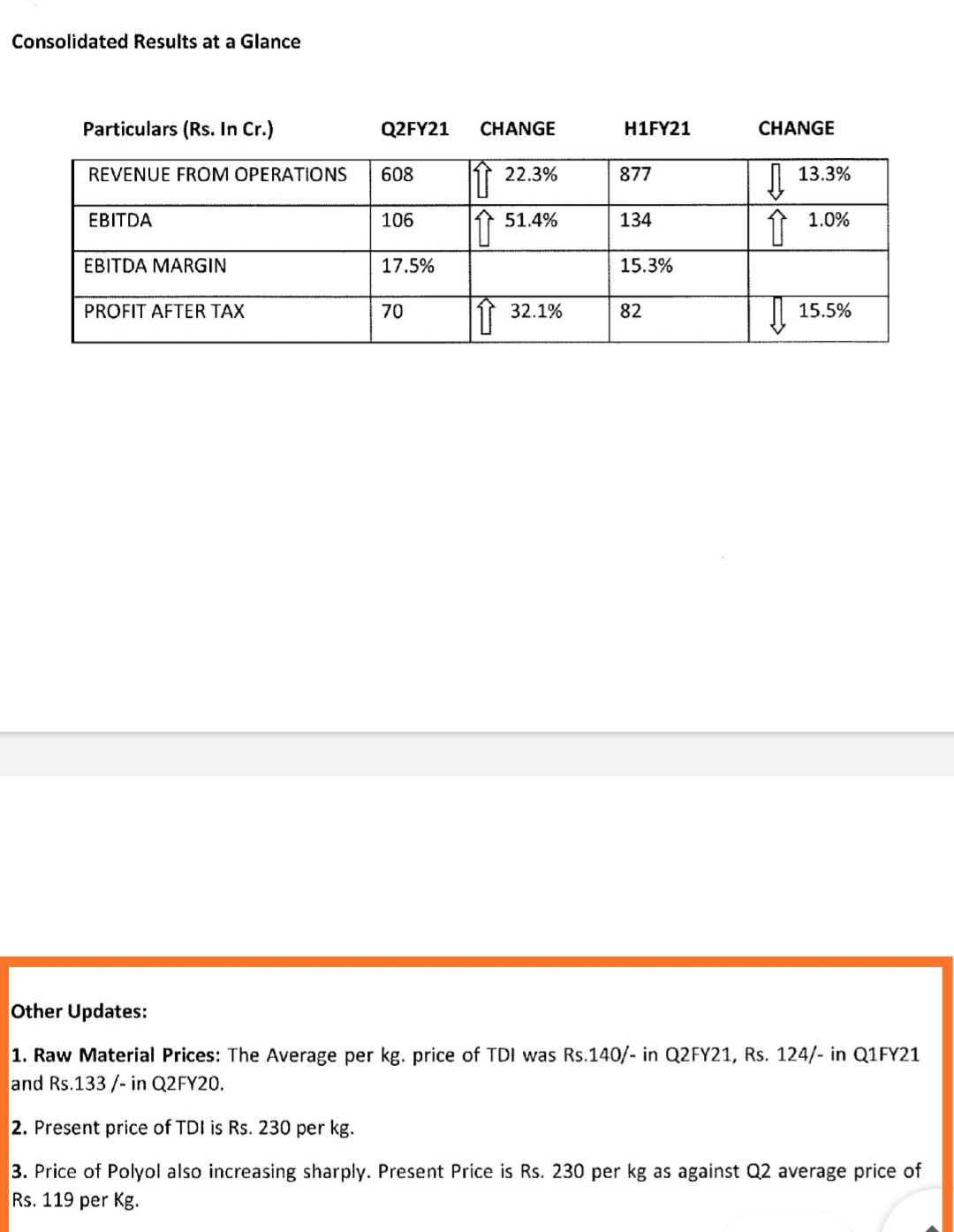

@nikhilbora Sheela foam concall gave details of RM which has increased from last few weeks(more than what I have mentioned in above post).

TDI price increased to 154/kg. Polyol price is expected to reach 130 -140 level from low of 110.

Gross margins: impacted due to product mix,low volume of purchase,retention of RM at ports,low yields due to lesser production and loss of GST refund. EBITDA margins may get impacted in the short term with rise in RM but eventually it will be passed on.

India: 80-85% of overall business volume has returned.

Australia and Spain subsidiaries contributed to the topline and profit of Q1 and continue to do well.

Australia business: gaining market share.

Spain: expecting better revenue in future. Spanish acquisition has just 1% of the entire EU market. It has the opportunity of supplying to the USA and Northern Africa. Lot of technologies like foam technology for shoes from India can be transferred to the Spanish unit.

IT business:finding opportunities with medium and small vendors. Does not need any further capital.

Online business: last 2 years growing at 30% and 2 months in E commerce sales growth is around 50%. Overall industry 4% share is online business. No.2 on amazon,

Export: revenue will flow in FY21. Work is progressing in the right direction. Guidance about export revenue will be given in next quarter.

Capex: 50 cr of maintenance capex. New greenfield plant at Jabalpur in another 2 years at capex of 60Cr

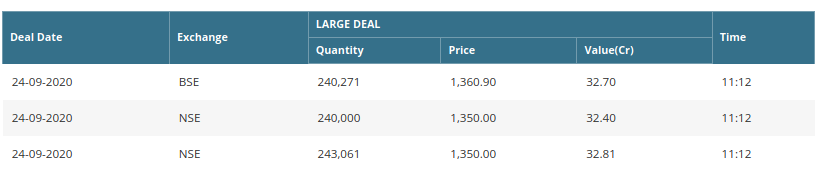

Looking at the delivery percentage it looks like trading happened. Few days back it had humongous volume but with delivery percentage of more than 99%. That was exchange of hands. Today delivery percentage is just 35%. So most of the quantities were traded. Sheela Foam doesn’t have that much buyers to absorb such big dumping(if it is). Few days back DSP mutual fund entered.

while results are good, with elevated raw materials prices , near future margins will be under pressure - broader inferences. They may pass some of it but may need to absorb some. Heartening to see high volume jump though per mattress realization is flattish.

Very good performance from Australia and Spain with higher profitability offsetting somewhat subdued performance from India.

Overall a good performance in tough quarter considering logistics isn’t an easy one for mattresses etc.

Considering current Qtr run rate a branded franchise is available at fair prices( below long term median average PE).

Kotak and DSP MF have built and further positions recently.

Just to be clear I am asking, both TDI(mentioned in point 1&2) and Polyol(point 3) are raw material? Both prices have almost doubled. Don’t you think it will bring down margin in a huge way. Even if they pass some to customers, don’t you think next quarter will have too much pressure if these prices continue or increase. Topline will have to increase in a very good way to compensate this. Views invited.

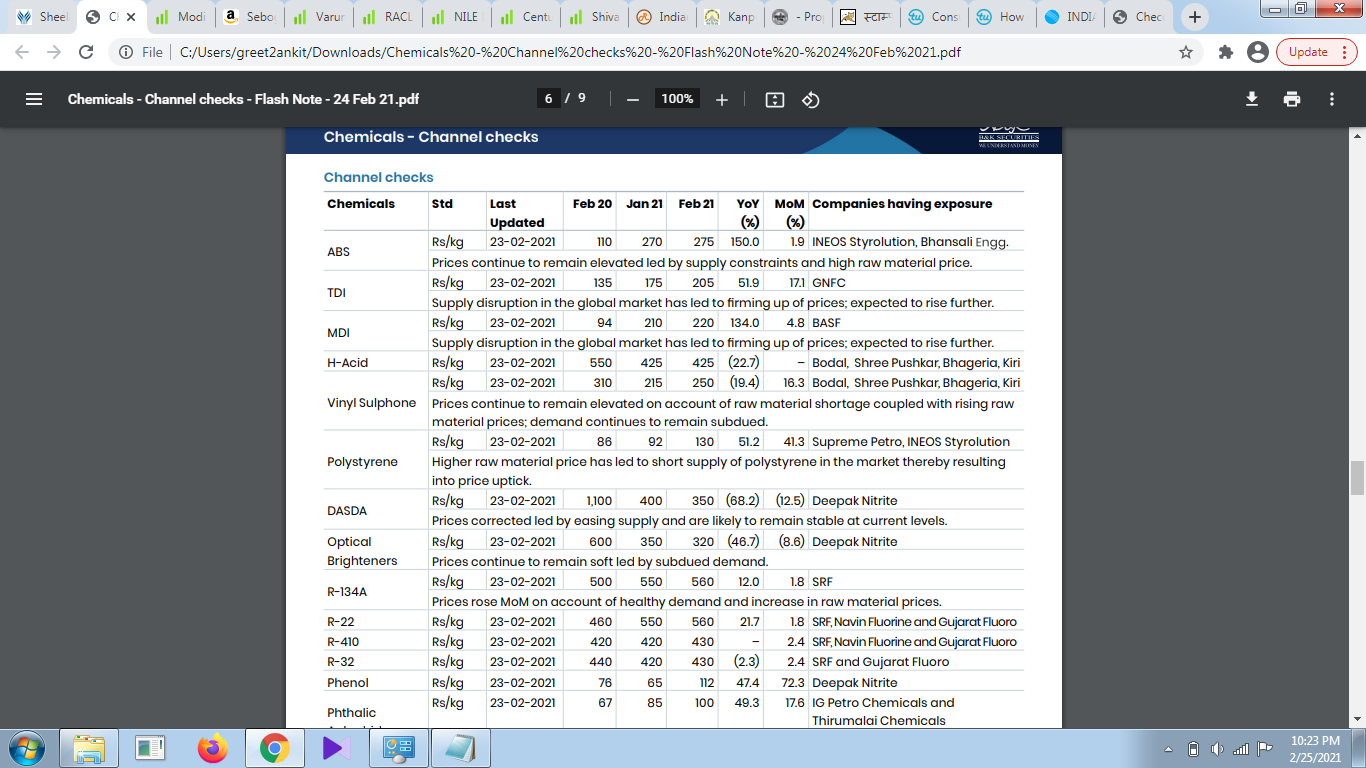

Above article explains the supply chain being an issue. Let’s wait to hear from mgmt - expect a prudent mgmt to have some buffer on raw materials given they would have seen this coming…also updates like this does send out subtle message to market on what to expect

I think rise is raw material prices is already factored in the stock price. (1600 to 1300 after last quarter)… Raw material prices of more than 210-220 was already discussed in last conference call…

Results of this quarter are indeed positive considering the scenario out there…

Thanks a lot . As they are a fine management, I hope they have seen this in advance and collected Raw material at cheap rates. Even in Q2 (after increase in Raw Prices) , they posted such good results. This shows management is strong and plan things. They look conservative as well and keep things clear. With such low float and fine management a top brand can do wonders. That’s my view. I hold heavy so view may sound biased.

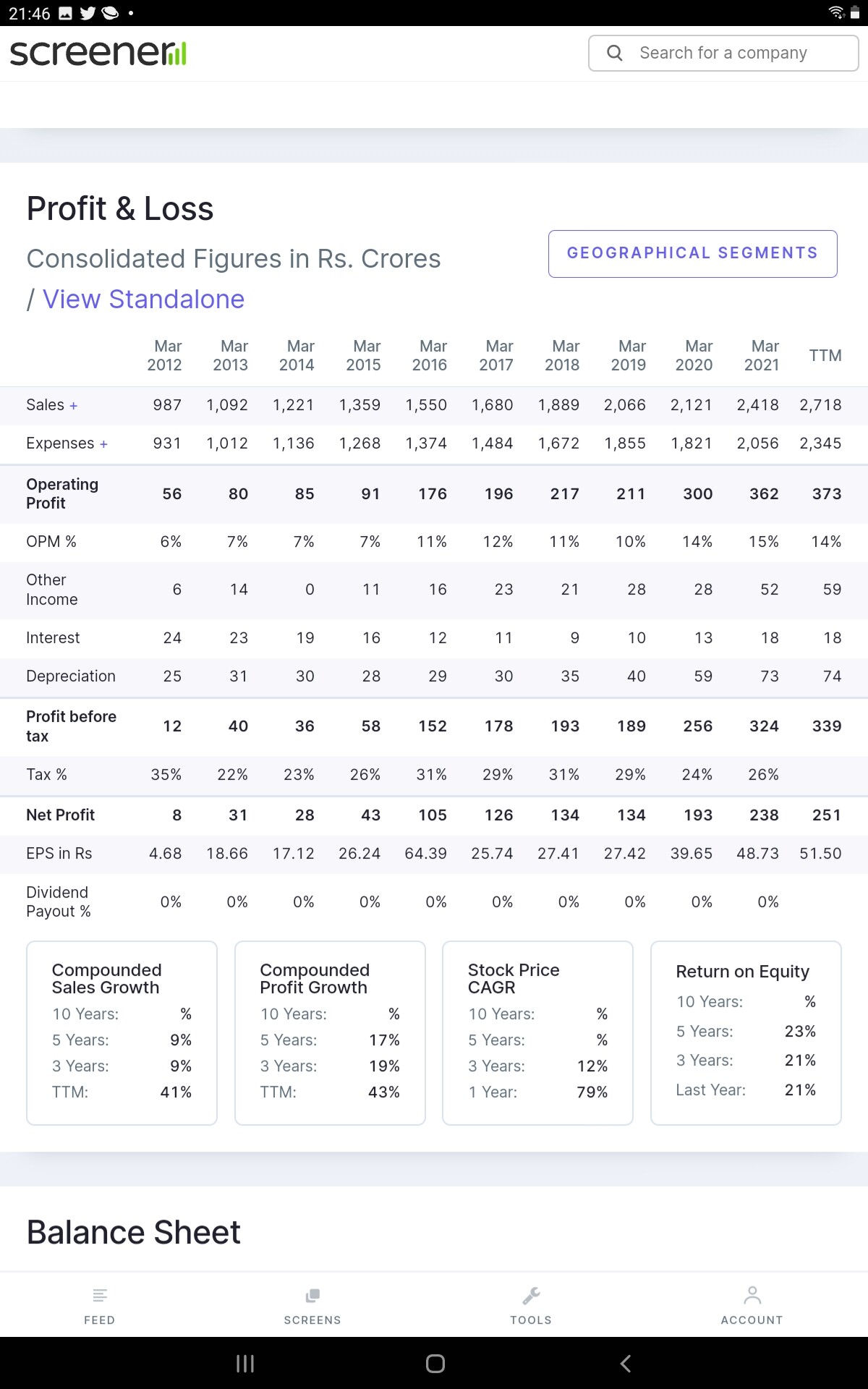

As Per Screener from Balance Sheet it seems companies Gross Block has increased from 512 Cr(March 2019) to 1084 Cr(March 2020)

Can someone who has been tracking company for respectable time explain why did company did so much expansion in its fixed asset( Greenfield/Brownfield/Acquisition of new company from which of the following companies fixed asset are growing?) and currently how much of that gross block has capitalized as Sales growth was not proportional to gross block.

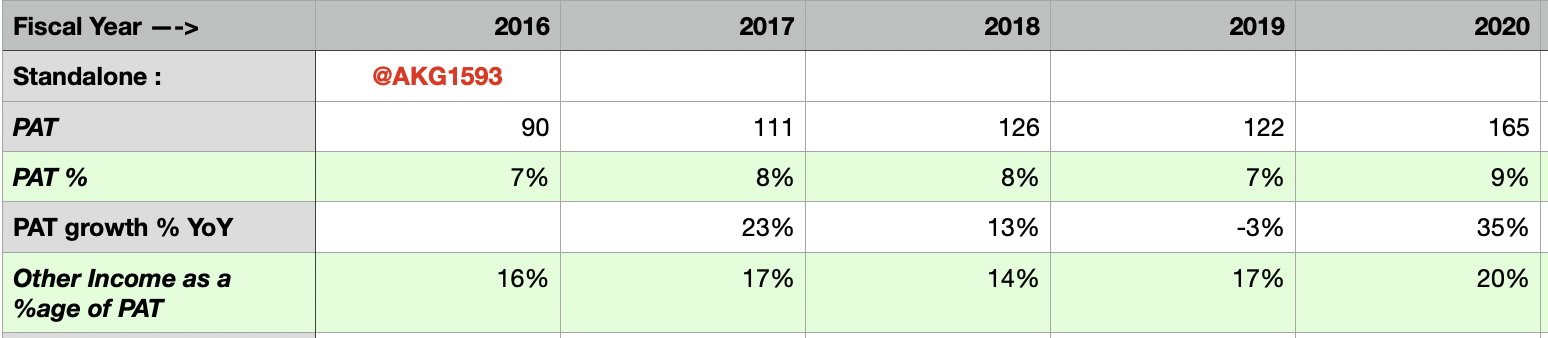

Looked at this company’s financials because it came up on one of my screens…all numbers below are basis standalone statements of last 5 years (FY21 full year are yet to be released; anyway I would want to analyse the non-pandemic years before thinking about FY21).

I haven’t even started looking at cash flows because what I have seen in P&L and Balance Sheet is enough for me to make my investment decision at current Price levels…

It’s quite a sign of extravagant times we live in that a company whose :

Revenue growth is declining YoY (even before the pandemic)

Pays 0% dividends - For a growing company, it’s fine to retain 100% Earnings to invest in growth; but this isn’t a growing company from what I have seen above (I wouldn’t buy the argument that they are growing through investments/acquisitions abroad - that’s an easy way to divert attention from poor core operating performance which makes up ~80% of the business).

is trading at 45 times P/E, ~10 times P/B, ~38 times EV/EBITDA.

Capex announcement - channeled via a new subsidiary - focus seems value priced product for semi urban, E-Commerce.

Initially, ICTPL will establish two manufacturing

facilities one is at Village: Medhi, Tehsil: Niwas,

District: Mandla near Jabalpur and other is at

Nandigram, Gujarat with the object to manufacture the

valued products to tap rural or semi urban market

targeting consumer segment and scaleup the export

and e-commerce business.

The cost of project would be around Rs. 200 crores.

Half of the project cost would be funded by Sheela

Foam Limited through equity/preference shares/loan

and remaining would be funded by Bank(s).

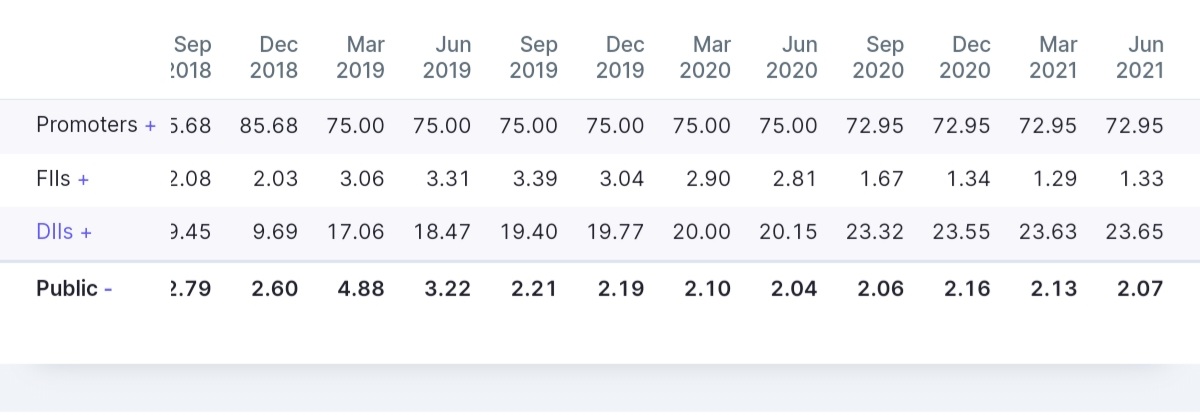

One interesting info on Shareholding- very low retail holding around 2%, low float

This is a consumption linked story and acquisition in EU and Australia have shown efficient capital allocation. Management has indicated using Spain as base for EU and US expansion.

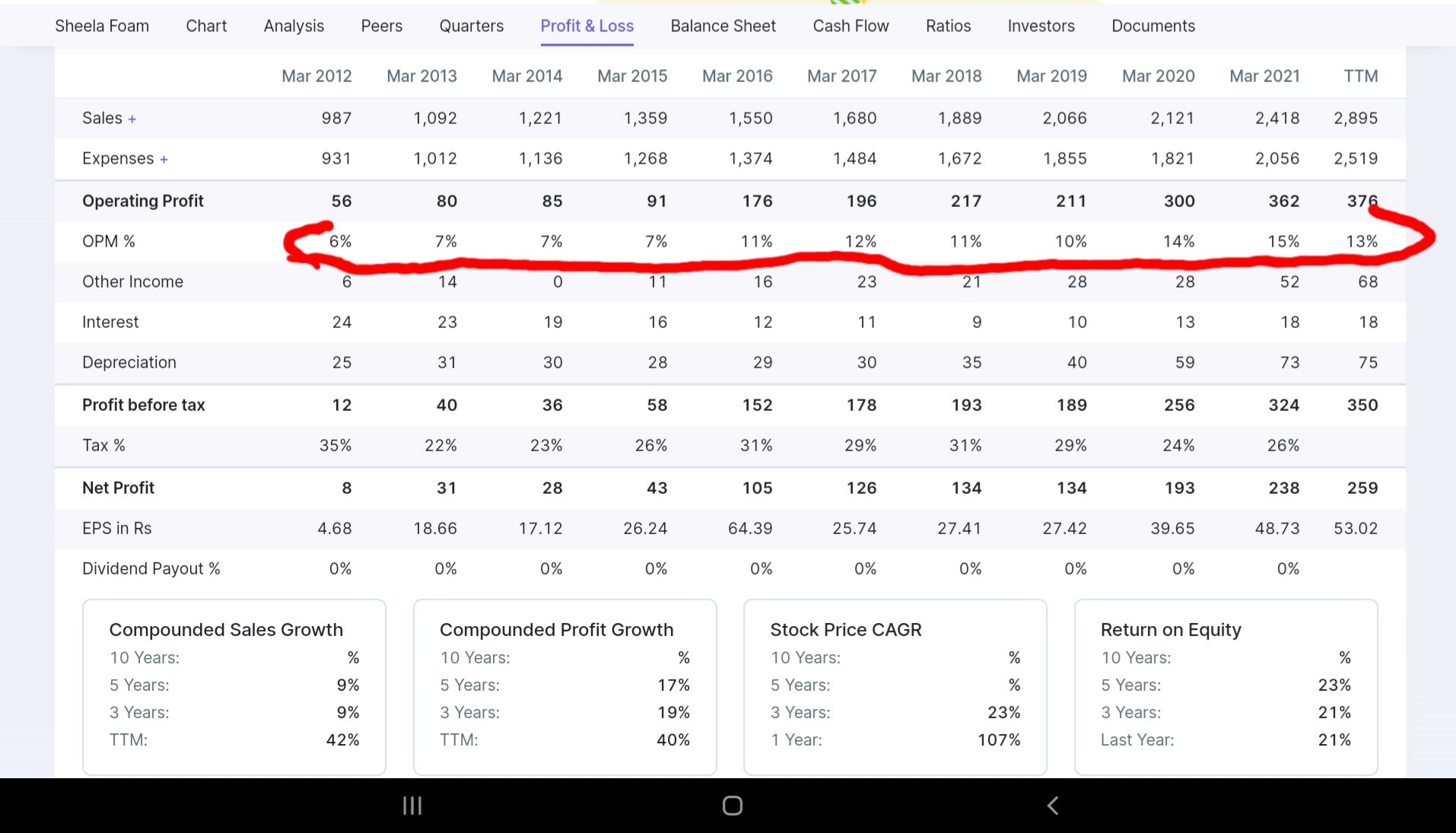

Here is long term performance- 2012 to now - 3X sales - 25X+ PBT, every year margin expansion, CFO to EBDITA has been good, RM prices has been quite high over last many quarters and still managed to keep margins stable.( barring Q1 22 - severe wave 2 impact - been a case with all branded consumption plays)

If anything, find them smart execution folks based on last few Qtrs tracking, leader brand in organized space , small fish in large pond, huge space with tailwind for unorganized to organized consumption theme as well as export possibilities to developed economies as substitute to China. With this new Capex, gearing up for mass economy and E-Commerce push.

Valuations - While stock price hasn’t moved extraordinary in this bull run, performance has been resilient with YoY growth in FY21, expect FY22 to do 3000Cr ( could have been higher without Q1 covid impact)+ sales, 425cr+ EBDITA , available at 3.5X sales and 25X EBDITA - fair valuation for a very long runway branded play. It can also benefit from housing sector revival - look forward to Q2 and future commentary, RM price impact and pricing hike to protect/increase margins.

Our strategies will accelerate sales in Metropolitan and Tier1 cities while capitalise on the growth potential offered by Tier 2-6 cities. The paradigm shift of people’s perception about comfort – be it at home, work or on the go - will be the key driver to our growth. The Indian furniture market is expected to grow at 13% YoY for the next 5 years, providing ample thrust to our new wing. In the B2B segment, growth will be led by long-term economic recovery

We see a new trend as consumers in the unorganised segment are shifting from their cotton mattresses to branded products with an expectation of improved hygiene and comfort. Others are willing to look beyond the pricing and invest in premium comfort products in exchange of long-term benefits. Backed by these, we are witnessing a strong traction in the mattress segment. Business in Australia will remain stable and Spain will offer multiple growth opportunities.

PerformanceE Review

Our net revenue from operations in FY 2020-21 on a

consolidated basis increased to 2,435 crore from 2,174 crore. Consolidated net profit after tax

increased to 240 crore from 194 crore in the

previous year and on a standalone basis net revenue

from operations stood at 1,690 crore as compared to 1,755 crore in FY 2019-20 on account of the disruptions caused by the COVID-19 pandemic. Profit after tax for the year increased to 181 crore from ` 166 crore. Net revenue from operations from Australia increased to AUD 81.08 million from AUD 66.1 million. Net profit after tax increased to AUD 4.84 million in FY 2020-21 from AUD 4.08 million in the previous year. The net revenue from operations from Spain increased from Euro 6.48 million to Euro 39.75 million, while net profit increased from Euro 0.69 million to Euro 4.09 million during the year.

SleepXEGrowthEStory

The online Indian mattress market in FY 2022 is estimated to be about 1,000 crore and is projected to reach 1,500 crore in FY 2023 and 6,000 crore by turn of the decade. User penetration is growing at a similar rate and is expected to hit 65.6% by 2025. The pandemic has resulted in a watershed moment where consumers are more comfortable ordering from the safety of their homes. Conscious buying based on health and hygiene has also increased in the pocket-friendly mid segment. Going by these, our E-commerce business are well poised

to capture the uptrend and have registered a sale of over a lakh mattresses and more than ` 55 crore revenue, demonstrating 74% growth than the previous year. Innovative products such as Personal Protector coupled with regionalisation of communication will further boost growth. Backed by the solid reputation of Sleepwell and offering its own unique advantages, SleepX is bound to ride the e-Commerce storm, break all records and take us towards a new high.

B2B segment

The momentum in automobile sector has also been a positive contributor to our growth and helped us restore high-market share in the sector. Factors that played in our favour in the B2B segment included focus on large customers with changes in B2B sale structure; increase in demand for mattress and other products from Automobile, Furniture and White Goods industry; reasonable progress in pilot projects including supply of foam to Indian Railways; successful introduction of Low Burn Foam for Auto Lamination and Peeling Industry; and catering to Bata’s pan-India vendor requirements.

Its a mid teen type sales grower at India retail biz, Australia at dingle digit and Spain as well as e-Commerce, Export to grow at much higher rates

RM cost is a concern for short term, company has handled last cycle well, as long as sales are robust they will maintain margins

Divya software is a questionable capital allocation ( small impact though)and a drag on bottomline, however Spain and Australia has done well on both top and bottom line

On a longer term Profits have grown at much higher rates than sales demonstrating operating leverage and brand pricing power, a 20% + CAGR is very much possible

Innovation and customer centric organization, continuing to grow market share( competetion is intense though in mass and eCom segment and hence recent Capex announcement of 200 cr)

Export has been called out by mgmt as a growth trigger, taking some time but it is a high possibility

B2B segment is economy linked and should continue to do well - mgmt has success in various pilots ( Infian Railways, prominent supplier to Bata)

Although not explicitly called out - housing sector revival could be a solid tail wind for SFL, with some lag - they benefit ftom both new houses and home improvement/replacement demands

What does a compounder exhibits - Sales and earning growth, good cash flows, Optionalities and/or smart inorganic growth, Good corporate governance, large Opportunity size , sector tailwind and so on.

SFL has consistently grown topline ( has inorganic element as well)

They have a midas touch on improving margins consistently, year after year, managed it well in last one difficult year as well( barring wave 1 and wave 2 qtrs - still manged growth at yearly level) - a decade of consistently improving margins speaks about mgmt execution quality

Capital allocation - one of very few Indian corporate who has executed overseas acquisition well( many good corporate have struggled for e.g. Symphony)

Its a well managed cash flow machine with good EBDITA to CFO conversion, year after year

Corporate governance seems fair, small Qs around IT subsidiary but that’s negligible in overall scheme of things and scale

FY21 delivered growth on both topline and bottomline , Q1 22 was subdued but Q2 22 has been good( even at 2 yr CAGR basis), though Q 2 is seasonally weak qtr

Pricing power as brand exists( barring B2B biz which is relatively smaller part), exercising judiciously

Thurst on Export Opportunity and India eCom biz as focused unit visible

Opportunity size is big - Unorganized to organized theme helping them and with supply chain woes, likely to continue

High promoter and strong hands holding makes it relatively low float ( public holding at just 1.8%)

One of consumer facing biz which has manged crisis well, though near term RM challenges stays

Strong on charts as well

India B2C and Spain are key growth levers and high margins biz

Besides branded play in India growing mattress industry, a huge sizable optionality has come as tailwind to SFL on Export front, mgmt too is bullish on Spain acquisition to deliver high growth on EU and US front- China used to be largest exporter but with heavy duties from US to China and allied countries ( see link above) , Indian players stands a very good chance to benefit, SFL has been well prepared on this front.

Strength in stock reflects these tailwinds, haven’t broken 50 DMA in last few week overall corrections.

Kurl-on’s net profit stood at Rs 6.1 crore in FY21 compared to Rs 9.7 crore in FY20. Also, its net sales declined to Rs 71.9 crore in FY21 from Rs 114.7 crore in FY20. For this Rs 2000 crores is being paid