This thread exists, but there is almost no information about the company in this. I am therefore reviving the thread as if it was a new thread by providing some background information and current developments. Do share your inputs on the company.

Company background

Shanthi Gears was founded in 1969 by a first-generation entrepreneur and was acquired by the Murugappa Group in 2012. Tube Investments now holds more than 70 % stake in the company. The company is now mainly into industrial gears and gearboxes and caters to a reputed clientele from diversified sectors such as general engineering, steel, cement, railways, power and material handling, among others. The company has a manufacturing facility near Coimbatore in Tamil Nadu.

Long Term Story

The business is cyclical and closely linked to the broader capex cycle in the economy. However, there is also replacement business since large gearboxes have a lifespan of five to six years, while the small ones last for two to three years. This leads to steady replacement demand even during lean periods. Sales growth has averaged around 10 to 12 % p.a. since the new promoters took over, while operating profit growth has been higher at above 15 %. Margins have been at more than 16 % p.a. consistently.

SGL is a small company with an efficiently run business model, which has improved consistently over the years. Financials are clean, and an uncomplicated balance sheet leaves gives very little scope for negative surprises. Company has no debt and investment in working capital has also been almost Nil over the years.

Cash flows have been higher than PAT, showing strong conversions of profits. Business is not very capex intensive, leaving decent free cash flows for the benefit of shareholders. Company has been consistent in giving dividends and thanks to a Rs.70 crore buyback in FY20, almost 100 % of the profits earned by the company in the last 9 years have been returned to shareholders. This year, a special dividend of Rs.2 per share has been declared on the occasion of completion of 50 years, taking the total dividend to Rs.5 per share.

The company is strong in the Railway segment, and the current boom in railway capex has been a boon for the business. The management says they get good volumes from the railway capex and Vande Bharat trains etc.

Revenues from the services segment are around 15 to 20 % of company revenues currently.

Forged steel is the main raw material.

Competition

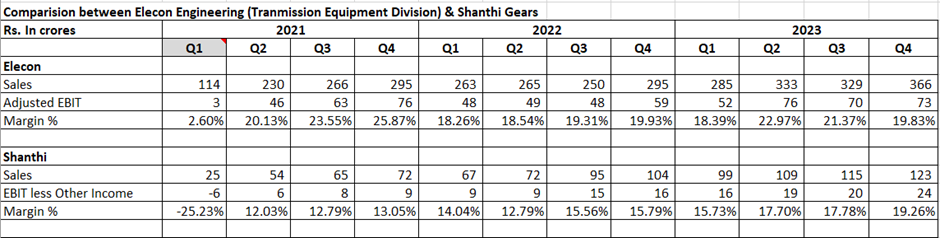

In the listed space, Elecon Engineering is into industrial gearboxes and is much larger than Shanthi. Historically, Elecon has reported higher margins than Shanthi, but the gap is getting bridged in recent times.

I think part of the reason Elecon has higher margins is its higher proportion of exports. SGL’s business is mostly focused on India while Elecon earns around 30 % of its revenues from exports.

Current trends

In recent years, SGL’s operating margins have risen strongly from 15.98 % in Q2 FY21 to 21.60 % in Q4 FY23, bridging the gap with Elecon. Along with this, PAT margins have also increased from around 12 % to more than 15 % in recent quarters. The reason for improvement in margins is better capacity utilization, most likely.

The company’s pending order book stood at Rs 270 Cr as of end-September 2022. In Q3 FY23, the company received orders worth Rs 120 Cr.

The capacity utilization currently is pretty high, according to the management though exact numbers are not available.

Future expansion

According to a brokerage reports, a high proportion of revenues come from customized products (70% of mix in FY 22) which earn higher margins. SGL’s parent company, Tube Investments, is planning to invest Rs 1,000 Cr in its EV endeavour and planning to leverage SGL’s expertise to manufacture gearboxes for electric vehicles.

Company already has surplus land available in Coimbatore for expansion. In addition to that, it has acquired a plant at the Gujarat’s automobile hub, Sanand, to explore growth opportunity from the untapped west and northern markets. The plant will be up and running in the next one or two quarters, according to the company management. Here the company intends to get into renewable energy, though more specific details are unclear.

Concluding Remarks

Clean Balance Sheet, industry tailwinds, strong parentage, improving financials and future expansion plans make Shanthi Gears an interesting stock to consider. The company does not do concalls or release investor presentations, so access to information is sketchy. Hope this post triggers some conversation about the business.

(Disc: Holding)