I am not sure if my understanding is correct. But there are a lot of stories spoken on the pharma opportunity but nothing really is showing up on the numbers.

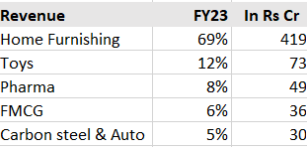

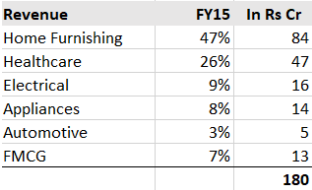

1.Got some scattered segmental numbers - FY23 from crisil report, FY15 - company disclosure. Pharma is flat

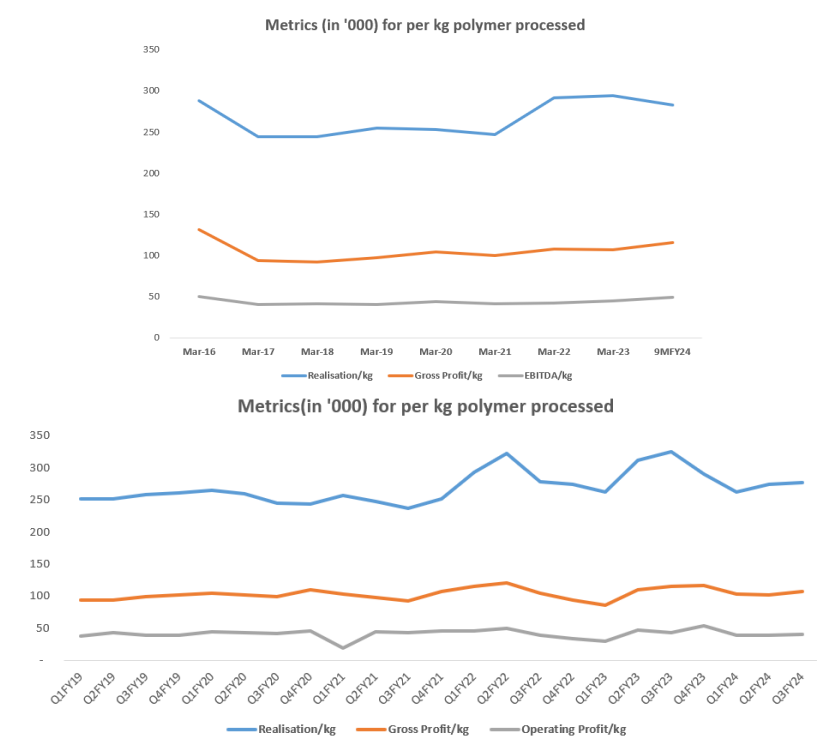

If pharma is really positively influencing, realisation per polymer processed should improve right, how does one view this?

How do you look at the addressable market of the three drugs that they keep speaking about - Semaglutide, Terixxx, Liraglutide? So, $XXXBn of opportunity would be how many pens. Lastly, Their addressable market would be much small right, because they are working only with Sanofi, What about Novo and Lilly?

Looking at other players in the drug delivery market - they are growing pretty well it seems, where is Shaily lacking?

Hi. I am going to study this in detail and get back. Please confirm what is the data source or sources for the figures and charts you shared in your post. Just to make sure that we both are looking at the same thing.

I agree that in terms of revenue the company has not shown any increase in pharma or healthcare.

Once again, I agree. We are not seeing any meaningful difference in realisation per kg polymer processed.

I am going by what the company has referred to in their latest concall. See the below screenshot. Amit is referring to how this market may grow to half a billion pens a year. But you are right. The company is totally dependent on how big a share of that market does Sanofi get or how much market goes to generic manufacturers who also then use Shaily’s products.

I think they took some time in trying to understand how to organise their business. For example they started the toy business a few years back and are now retreating from it. In the interim they also kept looking for a CEO but have now put that project on hold. They have recently done a capex of 100 crores specifically for Pharma and my guess is that they are now feeling confident of that getting converted to revenue real soon. Otherwise why would they sink so much money into capex which will lie underutilised for the next couple of years. But this is my optimism talking. Let’s wait and see what kind of revenue and profit starts getting generated from the pharma business.

@aadhar.aggarwal@Cuckoo_Invests The main hope pharma division is flat over almost a decade, management has repeatedly missed guidance and now saying pharma will actually break -out. Beyond hope, what is the strategy here for investors?