Sales growth was 28.13% yoy. Though sales were a bit lower qoq in vale terms, volume growth was good at 3547 MT as compared to 3376 MT in March qtr.

EBITDA Margins were a tad lower at 15.67% as compared to 15.96% in March qtr. Margins were affected due to lower sales realisation and increased employee cost.

Employee cost increased 31.3% qoq from Rs. 7.56 cr. to Rs. 9.93 cr.

Sales realisation were at Rs. 250916 per MT for Q1FY19 as compared to Rs. 269549 per MT in Q4FY19 and Rs. 262604 per MT in Q1FY18. Sales realisation for the whole year FY18 were at Rs. 232750 per MT.

Company setting up a new plant in Halol which will be commercialised by September 2019. Acquired 17 acre land in Halol.

Planned Capex of Rs. 40 cr. Arranged debt funding of Rs. 100 cr.

Received Rs. 100 cr. order from a Home Furnishing Major, start with 6 new products in furniture segment.

Company maintaining it’s target of USD 100 mn sales by FY2020.

Operating proftability has remained healthy over the years as it operates into niche segment of precision molding and caters to demand from global industry leaders in their respective segments.

Home furnishing is the largest segment for SEPL with more than 60% of its total operating income in FY18 being contributed by it wherein it caters to a single industry player which leads to high customer concentration.

SEPL has cost pass-through mechanism with most of its customers, price revision happens only with a time lag.

SEPL has plans to incur sizeable capex for expanding its existing manufacturing facilities for plastic products as well as for establishing a new facility for carbon steel products. SEPL has already achieved financial closure for the same and is expected to commence production in H2FY20.

It was expected the margin to take a hit but I am more concerned about the revenue growth.

Quarter growth is only 9.6% and Half Year 18.3%. I would not term this impressive considering this is small cap.

Has Management said anything related to revenue growth?

I am surprised by the lack of discussion around cash flows in this thread. For all the hype around its PnL (product diversity, hands in many industry pies, marquee customers etc etc), where are the cash flows?

Over the last 10 years, Free cash flow (i.e. Cash flow from Operations minus Cash flow from Investing) has been negative in 5 of the 10. And of the remaining 5 positive years, the FCF was <5 crore in 3 out of those 5 years (source: screener.in)

Ok, they are investing for growth you’d say. Let’s say they cut down on capex, what would you get for Normalized free cash flow. Average Cash flow from Ops has been 17 cr over the last 5 years and 19 cr over the last 3 years. If we take depreciation to be indicative of maintenance levels of capex (15 crore in TTM), then you have 2-4 crore as average FCF.

If you want to be more generous then let’s use 15 year life on their current fixed assets of 127 crore, to get a maintenance capex of 8.5 crore. Using this, we get FCF of 9-10 cr. This compared to EV of 850 crore or an EV/FCF of well above 80x.

It’s just very expensive for the kind of free cash the business generates. All that PnL hype has to translate into cash ultimately, and so far that evidence is paltry.

Agreed. I also have same view. Is it case of cooking of the books? Let’s dig out more to find out red flags. No business is good unless it able to translate revenue/earning into cash flow !

Despite a healthy dividend payout (26.1% in FY18) and ongoing capex cycle, a disciplined working capital cycle and higher machine utilisation will lead to healthy free cash generation.

Not invested here but few points you must understand:

For a rapidly growing company, you will always have negative or close to zero cash flow from operations and most likely a negative FCF simply because cash flow of operations includes the additional negative cash flows in terms of the extra money a company has to put up for increased working capital as the company grows. FCF would be even more negative particularly in Shaily’s case as their revenues are dependent on machines that they are putting and any company growing by almost 2x as Shaily did in FY15-18 would also do a lot of capex related to growth.

So better way to analyse cash flows is normalizing the same for growth and analyzing RoCE and working capital days rather than using cash flow from ops. number as it is. If the company is hardly growing, then ofcourse CFO and FCF are the real numbers to use.

Secondly, again the maintenance capex doesn’t seem right as most of the machine addition seems to have been done recently (100+ cr out of 133 cr Gross block of FY18 was added in last 4-5 yrs) and also a large part of gross block is buildings where rate of depreciation is very low. Lives of the machines are of-course totally dependent on the technology & product and I have not studied it in case of Shaily.

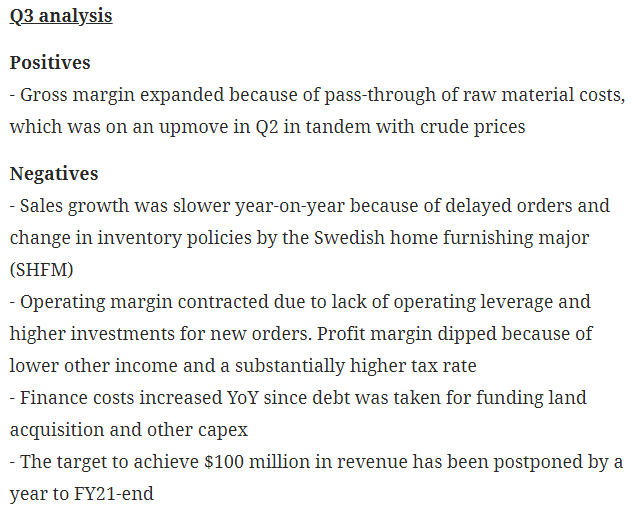

weak numbers from Shaily. PAT down by almost 50%

The presentation mentions change in major customer’s inventory policy as a reason. More worrisome is that they are saying that customer policy changes are likely to be stabilized by H2FY20 !!

Shaily Engineering AR 2019 Notes

Company’s market cap has seen severe correction in past 1 year. Company was largely able to pass on the R.M. prices as the operating margin declined by 140 basis points as compared to severe increase in crude prices. If the company’s turnover is less than 400 cr in FY20 it’s tax burden will also reduce from 30% to 25%. With the growth plans, free cash flows and the clientele company has, it looks really attractive at these valuations. Adverse movement in Crude prices is a risk for the company but they seems to be managing it well.

Key Points

We have five facilities with over 120 injection molding machines ranging from 35 tons to 1000 tons with sophisticated high speed automated and robotic production lines including a dedicated ISO Class 8 clean room manufacturing facility.

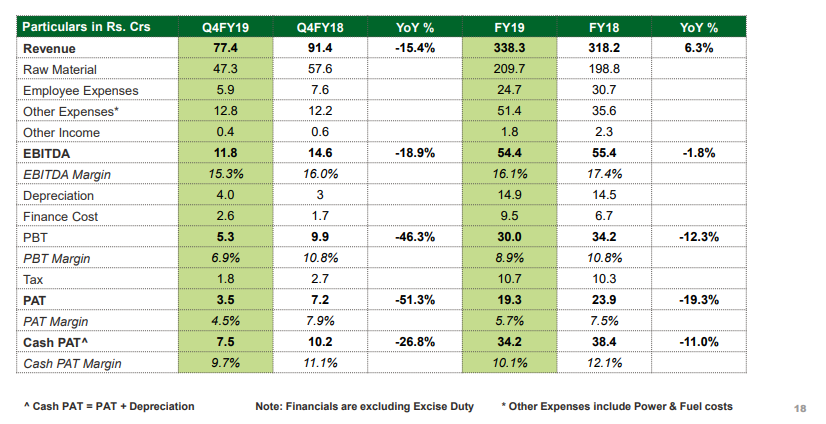

The company reported revenue of ₹ 340.12 cr in FY19, up from ₹ 321.95 cr in the last year, i.e. a growth of 5.64 % YoY.

The company reported EBITDA of ₹ 54.40 cr in FY19, as compared to ₹ 55.45 cr in the last year, i.e. a decline of 1.89% YoY.

Profit before tax (PBT) came in at ₹ 29.95 cr during the year, as compared to ₹ 34.23 cr in the last year, i.e. a decline of12.50% YoY.

The company reported Profit after Tax (PAT) of ₹ 19.28 cr in FY19, as compared to ₹ 23.89 cr in the last year, i.e. a decline of19.30% YoY.

The revenue mix for exports to domestic stands at 73.33%. The revenue mix continue to skew towards exports. Forex earnings are Rs. 233.30 cr. and Forex expenditure Rs. 115cr.

The volumes of polymers processed during the year was 13,258 tonnes (13039 tonnes in FY18).

Total Capex spend during FY19 is Rs. 52.40 Crs (including cost of land acquired for expansion). The capex has been towards the Carbon steel project, land acquisition and ongoing capex in the plastics business. The company also arranged for Rs. 100 crs of Debt finance at attractive terms.

Debt as on 31.03.2019 is Rs. 120 cr.

Company has good cash flow from operations of Rs. 66.45 cr in FY19.

R&D expense in FY19 is Rs. 3.17 cr at 0.93% of sales. (Rs. 1.85 cr in FY18)

Our performance for FY19 remained subdued on account of various factors as enumerated below:

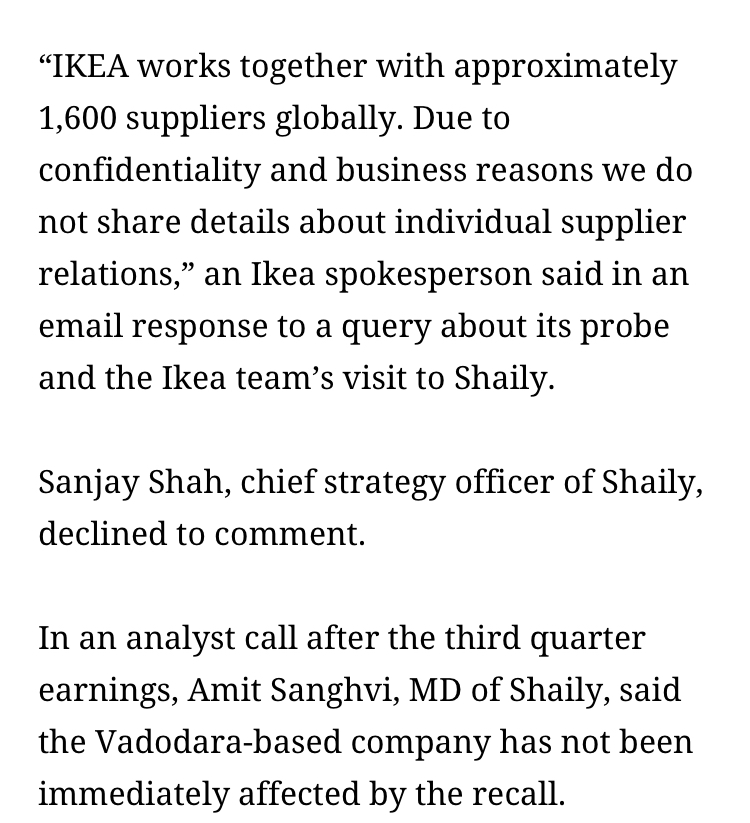

One of our top global clients has faced some challenges with their own growth as compared to their forecast along with the change in the inventory policy which has resulted in lower growth for SEPL. This resulted in lower frequency in ordering, coupled with lower quantity of orders.

We expected to have some more design and development income. Unfortunately, the same has been pushed to next financial year.

During the first half of the year, we had significant labour and power issues which streamlined in third quarter of the year.

During first quarter of the year, Appreciation of Raw material prices impacting performance in some quarters, however the same have been passed onto the customers with some time lag.

Finance cost has increased on account of higher debt taken for land purchase and capex for multiple divisions.

We have done significant investment by increasing management bandwidth to support the growth for coming years. The cost of the same has come this year, but the benefits are expected to follow in future.

Home Furnishings:

Swedish Home Furnishings Major (IKEA): New Product line. SEPL received order for Manufacture & Supply of products under a Carbon Steel Project. This is the first project of SEPL outside of plastics. Estimated Sales value of the order is Rs. 100 crs it will entail an investment of Rs. 40 Crs. Start with 6 new products which will increase in future. We are setting up a new plant at Halol for this project and expect to commercialize the order by September 2019.

Further received business confirmation for Manufacture & Supply of 3 new products in the plastics segment. During the year SEPL was able to garner increased business from the client.

Auto Sector: Received Business confirmation for 3 new products from Honeywell.

Pharma:

Confirmation for 2 new devices received from domestic pharma company. Confirmation from a new client from South Korea for supply of medical device.