What explains almost unchanged production profile over the last decade. These sort of bombastic and often childish valuation is of no use since it was valid some 10 yrs a ago too. Every oil field is different and recoveries depend on many things. Selan mostly deals in smaller blocks or where there is no bidding interest. One reason is that there is significant risk of sharp tapering off of oil flow. There are complex techniques available to increase the recoveries as the block ages but often it is about scale and applicability. ONGC/RIL and other oil PSUs are not fools to let go off some of these blocks.

7 Likes

You might be right. I have just posted the video and doesn’t endorse or reject the theory in the video.

Any insight or information on the extension of their licence period?

if i remember correctly, their license renewal was due but have not heard anything thereafter.

Anyone following this company, came out with excellent nos. Half yealy PAT (Rs 28 cr > Last FY PAT of Rs 22 cr) .So even if the P/E ratio remains same the stock should see good upside. Have tracking position. Biggest threat is if oil prices come down significantly.

Steep fall in crude price. Results were just in line with expectation.

No clue on the decline. However, I think the stock is in a sweet position as the P/E ratio is one of the lowest in last 5 years and EPS of 17.2 (HY) > Last year EPS of 13.45. A classic example of heads I win tails I don’t loose much

1 Like

Fabulous numbers from Selan. Margins though are inching towards its peak levels but not there yet. Maybe that’s the reason for its low multiples along with cooling of crude levels as pointed out.

Disc - invested

My biggest worry on this stock is not about crude oil prices as margins are quite decent; it is rather about ability of the company to get renewal on 3 blocks on which lease is expiring in 2020 & production increase from the blocks its operating/exploring.

Disc-invested, thinking of shifting to HOEC

This stock looks safe as always, Doesn’t move much even after high mkt / crude volatility. They don’t seem to have growth plan.

HOEC seems very aggressive but difficult to analyse looking at complex cost claim/ revenue sharing … agreements with govt.

I think their main project is B-80 joint development with 50 % stake expected to come online 1st qtr 20-21. total oil equivalent by then expected to be 8000 BOEPD. Tall order. High risks. Even if they make it , what would the P & L look like assuming current crude price.? Any one.

1 Like

(post withdrawn by author, will be automatically deleted in 24 hours unless flagged)

Hi All,

I have one observation

Revenue dropped by ~10% during Jul-Sep quarter while dollar and oil price high(6%) compared with Apr-Jun quarter. is it due to less production volume ?

The proposed EOR for oil exploration companies offers significant incentives. Although not every company is eligible. Companies using ER techniques will be eligible. Does anyone know how it relates to Selan? Would it benefit from the proposed EOR?

Hi All, Where can we find the Selan Exploration book value trend? Is there any book value improvement?

Was just going through the corporate presentation on Selan’s website. Its pretty detailed and offers information on the company’s plans.

Quick question on the information on pg 29 of the presentation.

It says: “Profit Petroleum 100% to Selan Up to IM of 3.5, 50% thereafter” .

Apologies for the naive question but what is the full form of IM?

Furthermore, any information on the PSC extension? Will the PSC be extended on the same terms? or are the terms likely to change

Disclaimer

Invested

Anyone tracking the buyback declaration from Selan? And resignation from its CEO Neeraj Sethi? The company plans to buy more than 8% of its shares back from the open market. This will reduce its free float. Buyback declaration at 300 while CMP of around 180 at the time of announcement, I was expecting it to go into continuous UCs, but that did not happen. Not sure as to why.

Also, the CEO of the company resigned effective 15th January, 2019. The CEO sold his holdings in August end (30th and 31st per disclosures on BSE website). Selan has announced about the ex-Cairn official Mr. Arunabh Parasher joining as COO. He has joined the company since October, 2018. So it seems like well planned CEO exit that was in discussion since last 4 to 6 months. (All inferences deduced from Google information). And they timed the buyback to minimize the shock of CEO’s exit and arrest the fall in stock price from 270 to 160.

Am I thinking in the right direction? Where will the buyback take this stock? Why did it not react to volatile crude movement?

Good that Selan has gone the open market route for buyback, unlike many other companies that are rewarding exiting shareholders at the cost of the existing shareholders. Seems like a significant number of companies are taking the tender route for buyback after the new dividend tax on dividends above 10 lakhs.

Also, why are they using fracking? If they are using fracking, does that mean that the output yield will decrease faster compared to conventional drilling? Any industry experts here that can shed light on the use of fracking by Selan? Is that something to be concerned about?

Its actually a pretty interesting case, where the numbers have improved materially over last 2-3 years + the company has done a buy-back which utilizes the surplus cash they have had and perhaps shows the management intent.

The negative has been that the company hasn’t been able to materially grow the volumes over long term

1 Like

The awardees of DSF Bid Round-II

http://dghindia.gov.in/assets/downloads/5c790f6729839Press_Release_Award_of_blocks_DSF_Bid_Round_II_ver1.pdf

- Selan bid for a offshore block in Krishna Godavari Basin without success

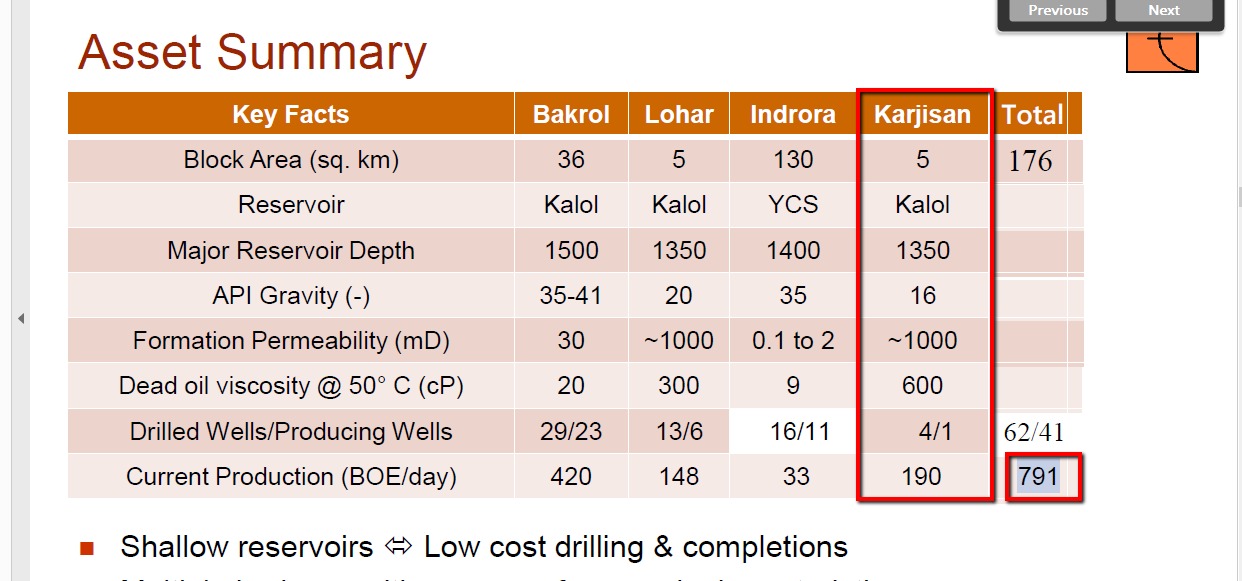

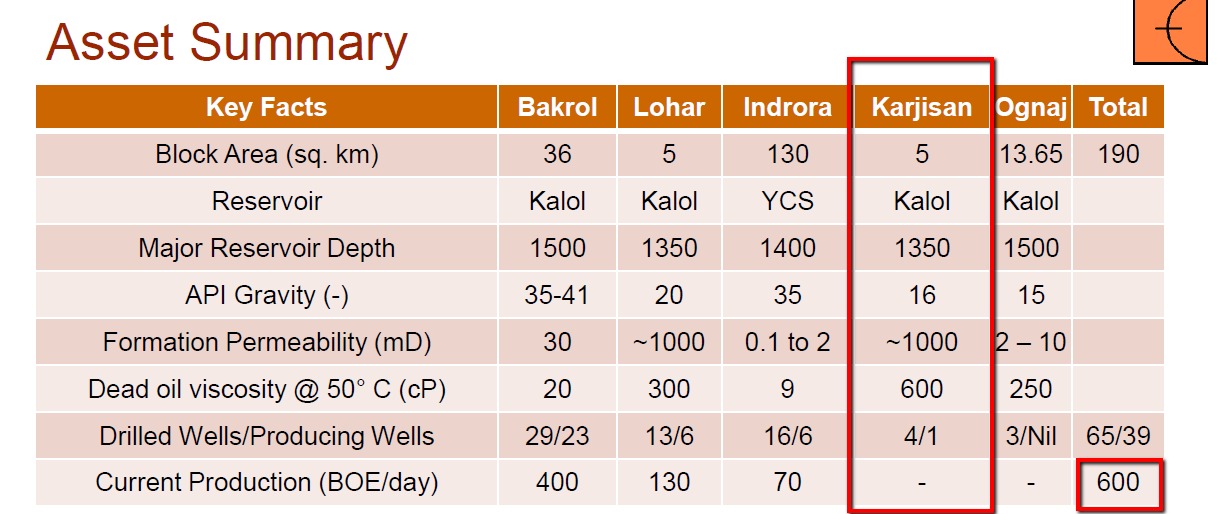

At last some good news on production volumes(reference corporate presentation)

Last year September - 600 BOE

This year April - 791 BOE .

Disclaimer : Invested and major allocation recently at 170.

2 Likes

Can you plz share the link to presentation?