Seniors tracking the Selan exploration can give their comments on sharp reduction in promoter holding from ~40%+ as on Sept 2016 to 28.35% as on 31.03.2017. Also if we take into account the shares sold by promoter till date in current Financial year, the promoter holding should be <= 20.85% as on 14 June 2017.

Can some one please throw some light on why promoter is reducing stake at such a fast pace. Also in the absence of any institutional investors backing, what would be the implications of continuous stake sale by promoter in the open market for retail investors?

here promotors are not from same family.

And as I was previously tracking the stock, I found promotor asha Mahajan was slowly selling the stake at regular intervals.

corporate presentation is available in below link;

http://www.selanoil.com/Corporate-Presentation.pdf

I find it interesting to see the company is adopting latest technologies like hydraulic fracturing and horizontal drilling.

disclosure : Invested in the business

1 Like

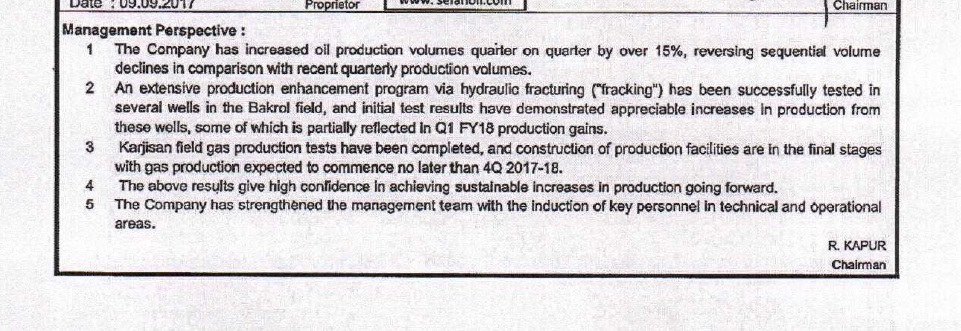

management commentary with June 2017 quarter results:

http://www.bseindia.com/xml-data/corpfiling/AttachLive/2d41b097-6411-4a87-908a-e2ca08ac753d.pdf

3 Likes

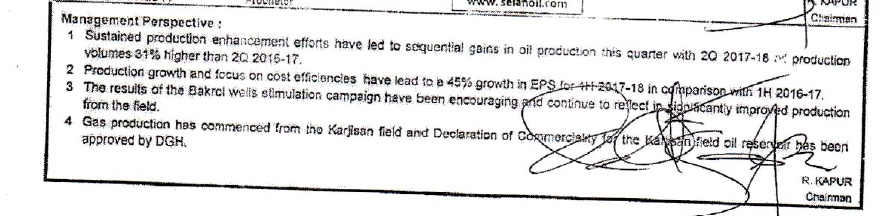

September 2017 quarter result is very encouraging ![]()

http://www.bseindia.com/xml-data/corpfiling/AttachLive/8d678900-1e2d-47a5-b787-8e0490e83499.pdf

management commentary along with the result.

5 Likes

Higher oil prices give a decent quarter.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/bedac90b-9154-47fe-966b-19d4cedfa31c.pdf

Production growth rate from stimulation and crude price determines the sustainability of the growth rate in the coming quarter(s).

1 Like

Oilex got 10 years of PSC contract extension; expecting the case for Selan’s fields as well !

http://www.londonstockexchange.com/exchange/news/market-news/market-news-detail/OEX/13590436.html

Selan has submitted bid for 2 blocks, from Cambay basin in Gujarat, under the first round of on-going OALP auctions. The complete list of bidders are;

http://www.dghindia.gov.in//assets/downloads/5ae9b36bb4177List_of_bidders.pdf

Note that these are undiscovered fields.

1 Like

Happy to see other boarder tracking Selan. Although Selan is marginally more expensive v/s PSU majors like Oil India Limited and ONGC, I still think its a good assymetric bet as 1) run up in share price is much lower than change in profits due to operating leverage on higher oil prices 2) ~$5 EV/BOE proven reserve is still cheaper than most international Oil E&P companies and 3) because of no subsisidy sharing unlike OIL and ONGC which much get roped in again.

I think the key monitor-able for Selan would be production growth looking forward, although even without production growth I beleive a 2x return is possible if Oil spot remains in $70 range.

Disc. Invested in OIL and Selan

1 Like

Selan q4 fy 18 results -

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=1835790e-0c34-4be0-8236-c9dddc211b4e

Good results.

The reason I feel Selan is not getting valuation of EV/BOE per barrel reserve as per its international peers is because it is having the oil field on lease basis and lease for 3 oil fields is till 2020. For the rest two fields it is upto 2030 and 2033.

Though there is good probability that it would get 10 years extension.

I might be wrong as this is my assumption.

Regards

Krishna

Discl - Invested

2 Likes

Was going through the FY2018 annual report. Following are the key points:

- About 21% increase in oil production from 1.65 lac bbls to 2.01 lac bbls.

- Production of gas increased from 60.48 m3 to 76.22 m3

- Indrora field has delivered its highest production since the discovery of the field in 1968. Karjisan oil discovery has been put on regular production. Karjisan gas production has also commenced. Pilot production enhancement activities have also been successful in Lohar which hold promise of improved recovery over the long term.

- Last but not the least, Bakrol, the primary producing field in the Company has undergone

significant production enhancement activities in terms of hydraulic stimulation and production optimization and significantly improved production over last year and continues to deliver higher production. - Co has submitted application for 10 year extension of the block.

- Baring Eq Fund has acquired close to 2% in the company

- Co has about 120 Cr of net cash on balance sheet.

12 Likes

Current market cap is about 337 Crs. Cash flow from operations is about 75 Crs. Is company expected to spend the cash on expansion in medium term?? Is there a (given in AR or derived) outlook for volumes expected in FY19 vs FY18?..Thanks!

Co has submitted application for 10 year extension of the block. …

is this the reason for overhung for stock performance ?

while other companies like HOEC rallied a lot this is not moving.

Thank you, Ayush, for sharing the notes ! A/c to FY2018 AR, Selan’s CEO was buying shares during the last year. Good to see his confidence in the business !

1 Like

A technical case study report, published by HLS Asia Limited (An oilfield service company) in November 2017, on their collaborative work with Selan in Indrora oilfield for characterizing the reservoir for identifying the producible and non-producible zones. Leaving aside the technical details, the report claims that the prospective pay zones are well identified for oil production.

http://hlsasia.com/wp-content/uploads/2017/11/MRIL_shale_SPWLA-2017-SELAN.pdf

I guess the company still have to go a long way before monetizing the finding.

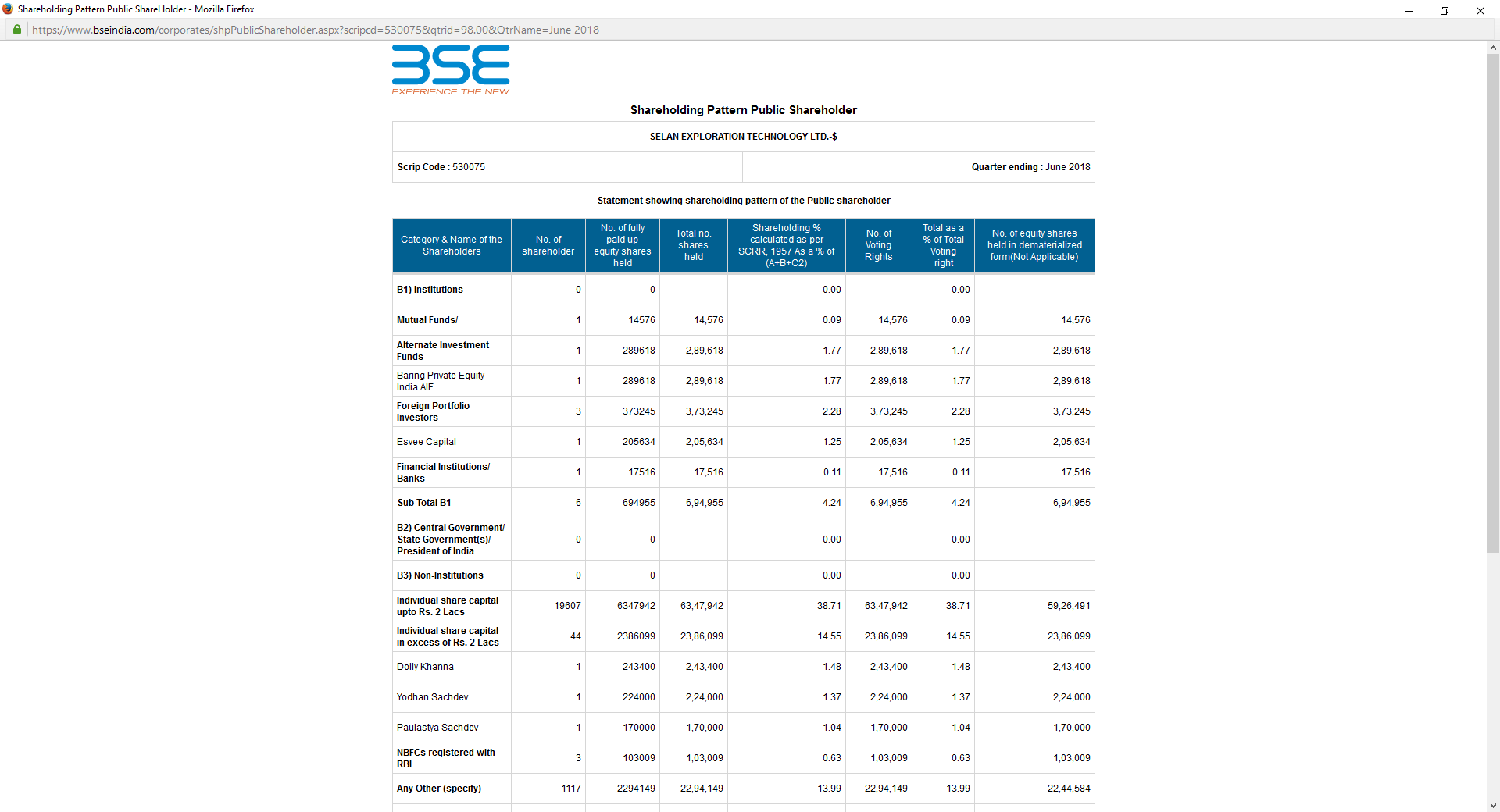

Dolly Khanna has has acquired 1.48% of the company.

The higher crude price, rupee depreciation against dollar, 25% corporate tax and the improved output from production enhancements would give better earning for Selan.

Yet another decent quarter for Selan;

It looks like the production rate (B/D) is same as that of the last quarter and the 15% increase in top-line is due to the higher oil price and the rupee depreciation against dollar.

List of awardees of the first OALP bid round;

http://dghindia.gov.in/assets/downloads/5b84f4d00b6c0List_of_Awardees_under_OALP_Bid_Round.pdf

Vedanta - 41

OIL - 9

ONGC - 2

GAIL - 1

HOEC - 1

This video analyses the value to Oil reserves Selan has to Rs 33000 Cr.(market cap 407 cr) at 60 rs/Barrel crude price and Rupee at $65.

Disc - Not invested.