Hi - I want to pen down a small strategy of saving in short term capital gains (I follow this every year):

Assumptions:

a) You have a stock which is below your entry point

b) You have short term capital gains / You believe you will have short term capital gains in near future (Short term capital losses can be carried for 8 years if i m not wrong)

c) You are filing your income tax returns (This is mandatory if you want to carry forward losses to set off against short term capital gains in future)

Methodology:

Lets say I have purchased PI Industries @ 700 (for academic purpose) and i want to hold on to it.

Lets say, I will sell and buy PI simultaneously @ 550 (Hopefully your transaction cost shouldn’t be more than 1% on both sides of trade)

Capital gains and losses are on the FIFO (First in First Out basis)

Now i can book a short term capital loss of Rs. 150 / share and claim it against Short term Capital gains of current year and in case i don’t have any short term capital gains, i will carry forward the losses for next 8 years

Now my holding of PI will be @ 550 (and if i m going to hold it for more than 1 year, any gains from increase in PI value will be tax free since it will be qualified as Long term Capital Gains)

I would still assume at the back of my mind that the entry price of PI for me is 700.

Few cautions:

You should have a liquid stock (where in you shouldn’t lose more than 10bps in spread while buying and selling)

Your transaction costs (like brokerage and associated costs) should be competitive (I wouldn’t spend more than 0.5% on each side of the trade)

You should file your income tax returns to carry this strategy

I m sure, many of the members would be following this strategy. Comments invited

if you do both way trade on same day it will be considered as speculation & during tax calculations FIFO will not be considered. check p&L of your account.

secondly, if you are eyeing for log term gain after trade then you need to wait for 1 more year.

so, one need to take decision based on the strategy.

If stock is shown as “stock in trade” than it is taken as Biz income , 1 must show it as “capital asset” in balance sheet for taking it as STCG or LTCG

This was told to my friend by IT officer as to why his STCG was taken as biz income and charged at normal slab rate and not special rate of 15%.

Please read latest IT circular No 6/2016 dt 29.02.2016 (you can get this on it dept website ) removing this grey area of ITO discretion on distinction bet capital gains and business income - excellent initiative as part of many other similar moves like digital scrutiny ,obligation on ITO who disobeys tribunal ruling over 90 days with 9% interest etc

Do we have CA / tax experts who can bring more clarity on this topic ? Is is possible to do what @varun88 is suggesting ? Are there any other rules that one should keep in mind while doing this ?

Year end short term loss booking is not something unique, its been there for ages.

Clarification 1

Sell the shares in a such way you don’t hit by FIFO method. This means if your earlier purchases are more than one year where you have a loss you won’t benefit as these will be classified as long term capital loss. Long term capital gain or loss have no relevance in India till date as they are outside the ambit of taxes (unless you are not paying STT, unlikely). The transaction cost which can go max up to 1-2% can save 13-14% net tax.

Clarification 2

It doesn’t matter what ever exchange you sell, exchange is just a market place for determining the price. Ultimately you have a electronic folio number with demat account. FIFO is applied on demat account not trading account.

Clarification 3

This is the classic battle between business income and capital gains. Because if you show as business income tax rates arguably higher.

If you are an individual doing business income you may hit 30% depending on income slab, if you are using a company as vehicle then you land up paying 30%. In a most likely scenario the tax rates would be higher than short term capital gain of 15%. But you can claim all incidental expenses against business income which is restricted for capital gain and specific to transaction costs.

The battle is on between classifying investment gain and business income.

The definition lies whether you are using as capital asset (capital gain) or using in normal course of business (business income).

You should be in a position to convince Assessing Officer that you are taking a sell call as opportunity not to save tax. One way of proving is earning dividend on stocks by holding for long time.

The portion of sale should be moderate in comparison to portfolio of shares hold.

You must be consistent in classifying stock in trade and investment if you are doing. If you flip flop over the years then you may get questioned.

There was a recent case in 2012, unfortunately it went to high court. The court put it to capital gains saying tax payer had a salary, few transactions, previous acceptance, no repurchase and so on.

This has been a issue of litigation always. The intent shouldn’t be tax avoidance. These are my views, I may be outdated. Though I am a CA not a tax practitioner.

This circular 6/2016 is bit dicey in nature like all other tax circulars I guess. This gives a minor head room for tax payer although continue to be jurisprudence heavy!

The circular does not challenged the definition of 14(2) which is definition of capital asset. So court or tribunal will continue to abide by objective interpretation of 14(2), unless the section itself amended through a statute. So the celebration is restricted:slightly_smiling:

First clarification says if tax payer treat them as stock in trade income would be business income, the tax guys won’t say anything. This means you continue to pay at higher taxes.

Second clarification if the transfer happens after 12 months (which is a long term capital gain) tax payer can show as capital gain and tax guys won’t dispute. This is perhaps beneficial for guys who were showing under business income for long term holding, tax rate can come down to zero. However you have to show always as capital gain, no flip flop allowed in future. In reality an individual will always show long term capital gain which is anyway tax free.

Finally they put a bomb saying nature of transaction (whether business income or capital gain) where transaction itself questionable itself such as bogus claim of LTCG,STCG or sham transactions. Ha ha, now who will decide “questionable”? Food for thought!

Now imagine if business guys starts classifying under capital gains, in bad years they won’t be left out anything to claim incidental situation. Catch 22 situation!

There is been heated debate going in CA institute over this. If you have a big amount please give it to a consultant unless you are one of them.

Intraday profit and loss is considered as speculative loss and clubbed under business income. If you have loss you can carry forward for next 4 years. This comes from the premise the asset is not transferred in terms of ownership as demat number didn’t change.

Profit from derivative don’t considered as speculative, he is called as a trader. But ultimately profit and loss goes and sit in business income.

In my opinion derivative is as good as speculation, perhaps more addicted.

Hi Suvi,

Thanks for your detail explanation. Suppose I am holding two demat accounts holding the same stock in both these accounts. Then how will FIFO work.

FIFO method was prescribed under section 45 (2A) of Income tax act. It basically says shares held in depository form (demat) if transferred and such gain would be taxable for section 48 (which is capital gain) and cost of acquisition and period of holding will be determined on FIFO.

It is applicable individually to demat account not collectively to all demat account of investor. FIFO is applied individually to demat account.

But do note, the transaction date calculating period is the day when you bought shares not the date shares credited to demat account.

Though I have a request Income tax is based on premise that you shouldn’t avoid taxes. Year end selling is controversial, open to interpretation multiple times.

If there is a need arise to sell meaning you were suppose to sell otherwise then calculate and pay taxes.

"As an investor, if you have any short term capital gains for the year you will have to pay 15% of this as tax. Assuming you have stocks sitting in your portfolio making a short term capital loss, you can book this loss, set it off against the gains, and hence reduce your tax outgo.

So assume you have made Rs 1 lakh in trading profits from your short term equity delivery trades. This would mean your tax liability is Rs 15,000 on this gain. If you had stocks in your portfolio which are making Rs 50,000 in short term losses, you can sell these and book the loss. So now your net profit for the year is Rs 50,000 and hence your tax outgo is Rs 7500 (15%), a saving of Rs 7500.

To make up for the stocks that you just sold to book losses, you can either immediately buy a similar stock or wait till those stocks are delivered from your demat to buy them back again. So if you sold ICICI Bank to book a loss on Monday, you can either buy say a HDFC Bank immediately for the same value or wait for Wednesday to buy back ICICI Bank again. So you continue to hold the same portfolio, but by doing this transaction you would have saved Rs 7500.

As an investor, long term gain is exempt from taxes, and hence you can’t use long term capital loss to adjust against short term gain. Only short term capital loss can be adjusted against short term capital gain."

September 2015 I left my job and income tax used to be deducted from my salary. I am currently studying with a bank student loan.

I do share trading (delivery based) and last year I got profit, though previous years I was in loss and therefore did not show it in my IT Return. Since I have student loan and no income, can I avoid filing IT Return ?

Why wait for two days to buy back…you can sell in NSE and buy in BSE at almost the same price…both transactions executed around same time…that way roll over without any market risk…

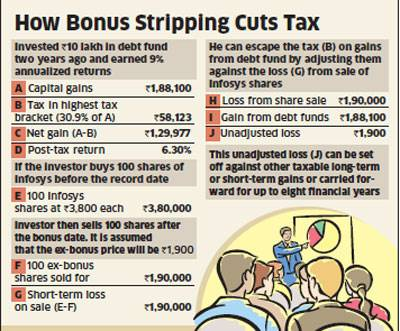

Bonus stripping, a strategy described here. Seems to be a legal way convert STCG to LTCG, can also help push your STCG to the next FYE if done correctly.

I always wondered why some rush to buy after a bonus announcement is made, when actually nothing is offered for free by the company. Could this tax advantage be the reason for such rush?